Crossing the Rubicon

Positioning is back to FOMO, earning breadth is a mirage, and the macro regime is quietly flipping under everyone’s nose.

I was initially going to write a long post recounting what happened, how we got there, and why the market did what it did. I’m going to spare you. Everyone who has a Twitter feed, or a pulse knows the rough contours of the Iran–US war already. What actually matters is what the event revealed about the market.

I called this piece Crossing the Rubicon for a very specific reason. I think we are within a week or two of passing the event horizon on the physical oil situation. Past that point, there is no smooth way back. Very soon, flights will start getting canceled en masse because refiners simply don’t have enough jet fuel in the system. Not long after, you’ll see dry pumps at gas stations, first in the weaker logistical corridors and then everywhere. This is a physical inventory and throughput problem that plays out on a timeline measured in days and weeks, not quarters.

That is the Rubicon. Once those lines are crossed, the market stops pricing an “Iran war premium” and starts pricing a structural supply regime.

The Playbook Worked, On the Surface

The Iran–US war followed the traditional playbook of any past geopolitical event: the S&P 500 corrected for a few weeks, then recovered.

What actually struck me was the positioning.

Real money and long-only funds were incredibly sticky. They didn’t sell anything. They diamond-handed their positions through the thick and thin of it, all the way down and all the way back up. There was no capitulation from the bigger, slower hands.

The fast money did the opposite. CTAs flipped from max long to max short in an almost manic fashion, then had to chase it all the way back up once the ceasefire held. The positioning snapshots for systematic funds told the story loud and clear: a full round-trip in a matter of weeks.

That’s the first clue. When the marginal buyer on the way up is a CTA covering shorts, and the slow money never actually left, you haven’t cleansed positioning properly. Instead you have set the table for a speculative rally.

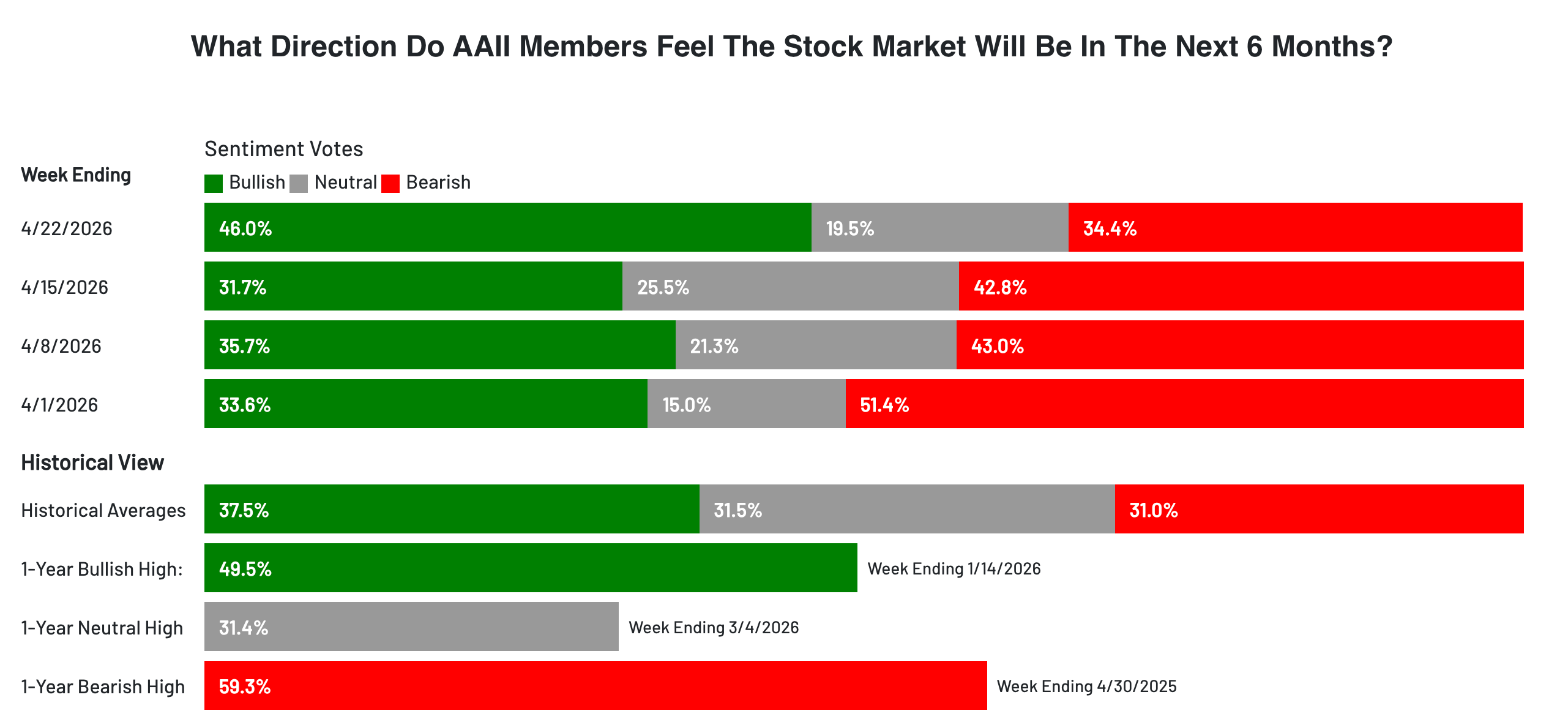

Everyone Is Back Long

Positioning is back to very full long, and FOMO is everywhere around me.

The data backs it up:

AAII sentiment is max bullish over a one-year window. Bears are capitulating.

The SPX call/put ratio is stupidly low.

The SPX skew is highly tilted toward calls. Traders are hoarding calls because they’re afraid of missing the right tail.

The Goldman sentiment indicator is back to firmly positive.

Every one of these is a sentiment-and-positioning alarm bell. Individually, you can dismiss them. Stacked on top of each other, they paint a picture of a market that has already priced the good outcome, and is now paying up for more of it.

The Cheap Market That Isn’t

I get the bull case. Fundamentally, the SPX was genuinely cheap during the war. Forward earnings kept rising while price corrected, and the forward P/E mechanically compressed from both sides: numerator going down, denominator going up. That’s the kind of setup that normally rewards buyers.

But there’s a big misconception here.

Forward earnings have been going higher on the back of extraordinarily narrow breadth. Roughly 50% of the earnings rise is coming from a single name, Micron. The rest is coming from energy. These are rough numbers, but they check out when you decompose the index.

Two things jump out:

The leadership is very, very narrow. A one-stock earnings engine is not a healthy market.

Energy-driven earnings leadership is bad leadership. Historically, when energy carries index earnings, the usual reason is that input costs are squeezing every non-energy sector on the other side of the P&L.

A rising forward earnings number looks bullish in a headline. Under the hood, it’s telling you where the pain is about to show up.

Stagflation Is Here

I strongly believe we are entering a stagflation regime where inflation rises dramatically and growth slows down. Every oil expert worth reading is pointing at the same thing: the supply situation is extreme.

The clearest tell came right after Trump extended the ceasefire. That headline was supposed to be unambiguously bearish for war-linked assets. Yet, oil went up on the day. When a market refuses to rally on “bullish” news and refuses to sell off on “bearish” news, you stop arguing and start listening.

Under the hood, the physical setup is ugly for anyone short oil:

Saudi Arabia, Kuwait, and Iraq all have full storage tanks, forcing wells to be shut in.

Reversing this can’t happen quickly. A realistic minimum is a month, and that’s the optimistic scenario.

These producers have no incentive to rush. They’ve taken major financial hits, they need cash to rebuild, and they are not going to flood the market with cheap barrels to do the importers a favor.

Production comes back slowly, if at all.

The numbers are wild. Saudi net exports are down roughly 50%, yet total profits are up over 100%. Lower volumes, higher prices, fatter margins. Why on earth would they race to “save the day”?

And this is exactly where the event horizon bites. Refiners run on working inventories and flow rates that have already been drawn down, not on theoretical supply. Jet fuel is the canary: it has the thinnest buffer, the most concentrated consumers (airlines), and the least flexible substitution options. Expect mass flight cancellations to start happening in a week or two. Gasoline and diesel pump shortages follow on a slightly longer lag, but the same math applies. Once consumers and corporates see it with their own eyes, the narrative shift is violent and irreversible. By then, the entire oil future curve has already repriced.

The Oil Call

Here is my base case, and I want to be explicit so you can hold me to it: an 18–24 month oil bull market, with a $100 WTI floor (absent price controls).

The drivers go well beyond a one-time war premium. They are structural:

Massive pent-up demand. Empty tanks across Japan, Oceania, and other importers. Cars and trucks still burn gasoline and diesel, and they still need to be refueled once supply normalizes. Consumption doesn’t wait for narratives.

Global SPR releases have created even more future buying. Governments are going to refill strategic reserves, and they are likely to expand them after this crisis.

Arab producers won’t race to save the day. They’ll extract their “just desserts” first. That’s just how cartels behave after being taking a hit.

Strong demand plus a slow supply response equals prolonged high oil prices, driven by both real consumption and strategic restocking. Do not trade this as a spike to fade. Trade it as a regime.

How I’m Expressing It: Long Canadian Energy

I am expressing this conviction by being very long oil stocks, and I particularly like XEG, the Canadian energy ETF.

Canadian energy has a stack of tailwinds that very few other energy equities can match:

Higher energy prices directly, obviously.

Higher CADUSD as the terms of trade improve.

No export ban risk This is the one most US investors under-appreciate. Washington has shown it is perfectly willing to weaponize export controls when domestic politics demand it. Ottawa has neither the incentive nor the political setup to do that.

Diversification away from the US. In a world where capital is starting to wonder whether it really wants to be parked in US megacaps, Canadian energy is an escape valve that actually produces cash flow.

The thematic tailwinds line up. You don’t get many setups where the macro regime, the physical market, the FX cross, and the political risk premium all point the same direction.

Why I’m Not Constructive on the SPX

Regarding the S&P 500, I do not have a constructive view. I think it faces severe headwinds.

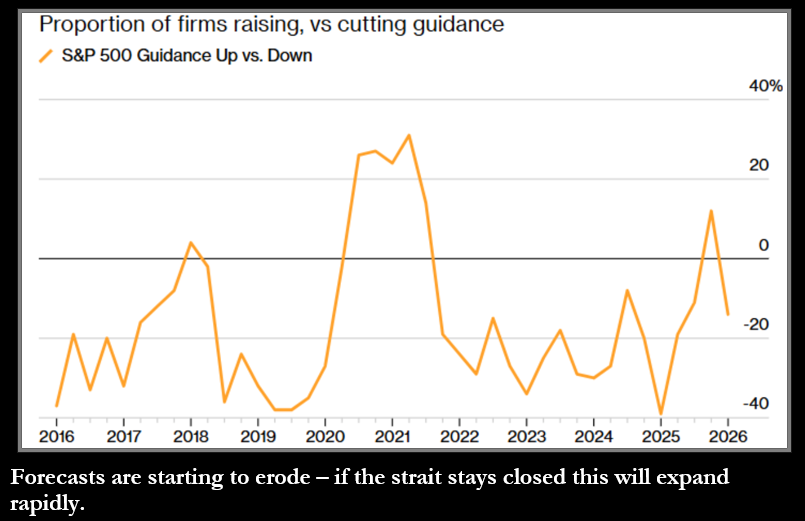

Concentration risk is as high as it has ever been. The Mag 7 dominance is what inherently makes the index riskier today. These companies are now very asset-heavy. Free cash flow has been falling, and it is still not clear when it recovers. Capex growth will start to diminish in 2027, but capex itself will keep rising. To digest that, you effectively need a big rise in revenues or profit margins to overcome the capex drag. It could happen. But at these multiples, it’s a bet with a bad risk/reward.

Consider the below chart for the upcoming Q1 earnings: Ex-Mag7 are expected to grow more than Mag7 (excluding NVDA).

The world is multi-polar, and the Iran–US war only strengthened that view. NATO, as we knew it, is dead. Everybody needs to rearm. Capital controls are coming (not tomorrow, but the direction of travel is obvious) to repatriate savings back home. The SPX is still the piggy bank of the world, and that role simply does not fit the world we are actually transiting into. When the rest of the world reprices its reserves and savings, the marginal buyer of US megacaps gets smaller.

And at the end of the day, it’s all about AI. Fine. But then why do you need to buy the SPX for that? You don’t. If you are bullish AI, focus your energy on the highest-growing EPS companies. Buy NVDA and Micron and forget about the rest.

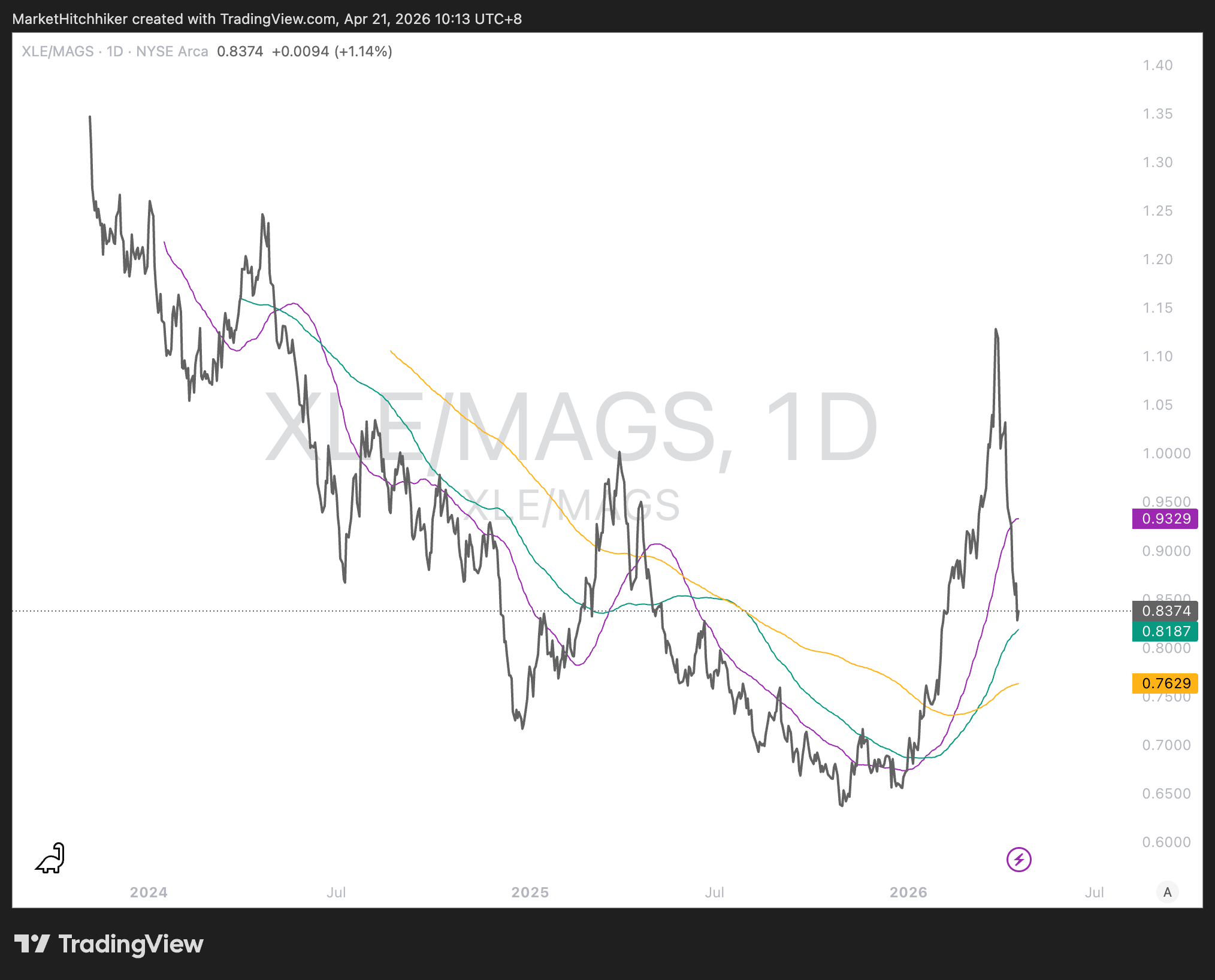

Energy In, Tech Out

Here is the framing I keep coming back to.

An economy, at the most fundamental level, is a machine for transforming energy into outputs (products and services). That is why energy stocks and tech stocks tend to perform in opposite ways depending on the macro regime: one is the input to the machine, the other is the productivity layer on top of it. When energy is cheap and abundant, the productivity layer captures all the rents. When energy is scarce and expensive, the input layer takes its share back.

We’ve just lived through a very long stretch of tech outperformance. That was the correct trade for the regime we were in. We are about to see that reversal in the coming year or two. The macro regime underneath is flipping, and the relative performance between energy and tech is going to flip with it. This is a regime call, not a bubble call on AI.

Takeaways

Positioning and Sentiment did a round trip. Sentiment is now max bullish, skew is leaning on calls, and slow money never sold. Upside surprises from here require new marginal buyers, and I don’t see where they come from.

Don’t confuse narrow breadth with strong earnings. Micron plus energy is not a healthy index story.

Trade oil as a regime. Position for 18–24 months, with $100 WTI as a floor and $150–200 as a realistic simmer range before we hit demand destruction.

The event horizon is days weeks, not quarters. Jet fuel cancellations first, pump shortages soon after. By the time it’s on CNBC, oil equities have already repriced. You want to be there before the headline.

Prefer Canadian energy (XEG). Same thematic, better FX, lower political tail risk, genuine diversification away from US exposure.

If you have to be long AI, concentrate. Buy NVDA and Micron directly. Or DRAM ETF if that’s your thing.

Plan for the tech-to-energy rotation. It won’t happen in a single day. The direction is set.

The Rubicon has been crossed. Position accordingly.