Macro Update #34.1

Part I: Growth, Labour Market & Inflation

First, I would like to apologise for not having written any macro update in the past month. It is a time-consuming exercise, and I was uber-focused on delivering the web app, which has a much higher impact on my immediate trading results.

Getting the macro picture correct is a crucial step toward getting the market right, but it is just the first step. Trading is the art of converting information inputs into returns. Macro is just one of many inputs, albeit a very important one.

I have written 33 updates in 2025, this is roughly an update every two weeks. I was initially aiming for weekly updates, but in retrospect this was too ambitious. More than that, weekly is probably an inadequate frequency for this exercise. Macro follows the ebb and flow of economic releases, geopolitical events, market developments, and the unpredictability of Trump tweets.

From now on, I will use a discretionary frequency to post macro updates. If the picture hasn’t changed, there is no need to write thousands of words about it. A simple reminder of my views in the chat or a very short post will be more than enough. However, if I see key changes in the economic trajectory or a shift in the balance of risks for macro assets, then I will write a detailed post.

This should be a better format. To make sure we always have an updated macro dashboard, I will host it on the web app. For new readers, please see the dashboard in the latest post here.

Your time is precious, and so is mine. Let’s dive right into today’s update, and because it is a lot to digest, this update is split in two different parts. Part II will be published tomorrow.

Growth

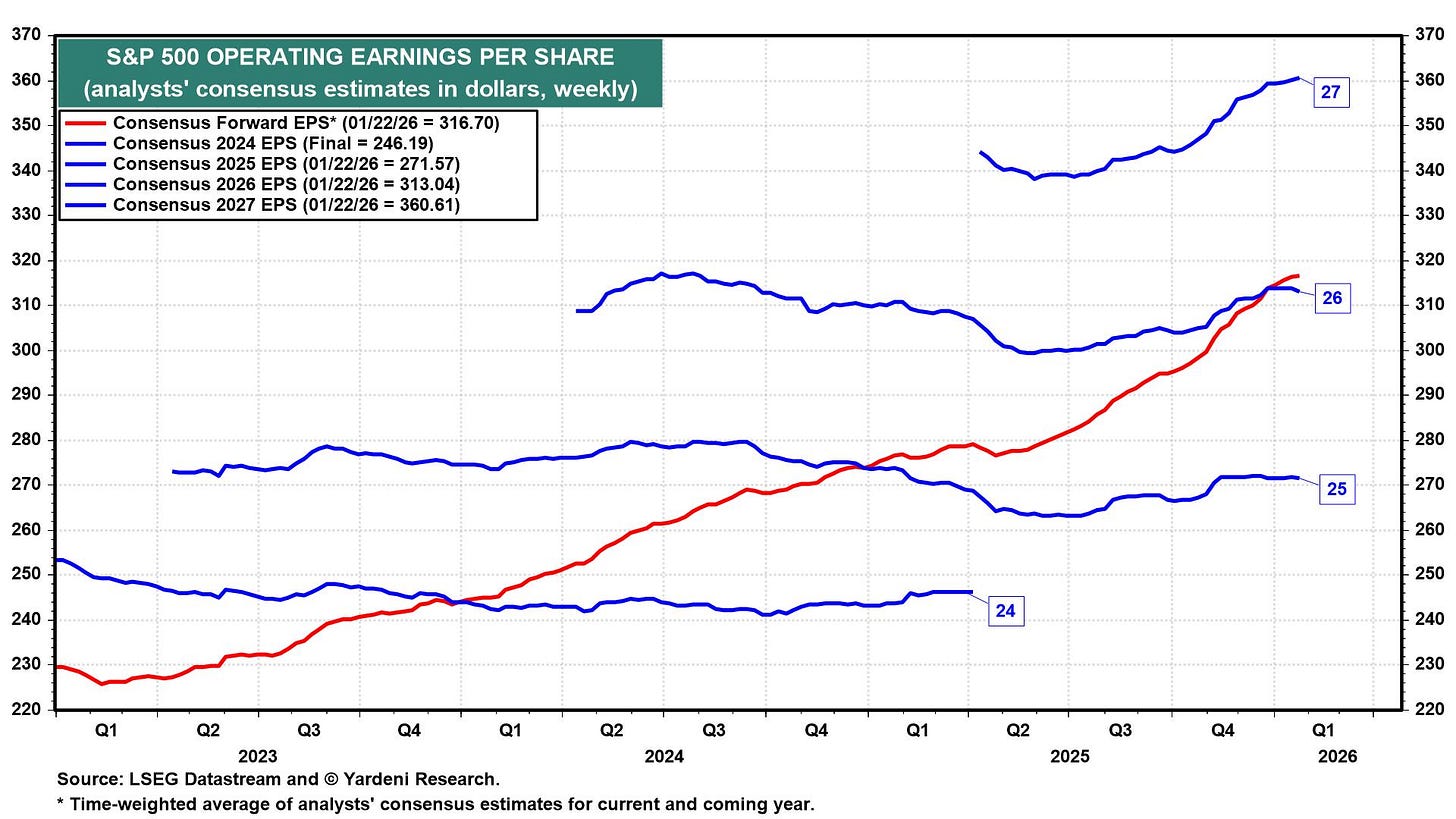

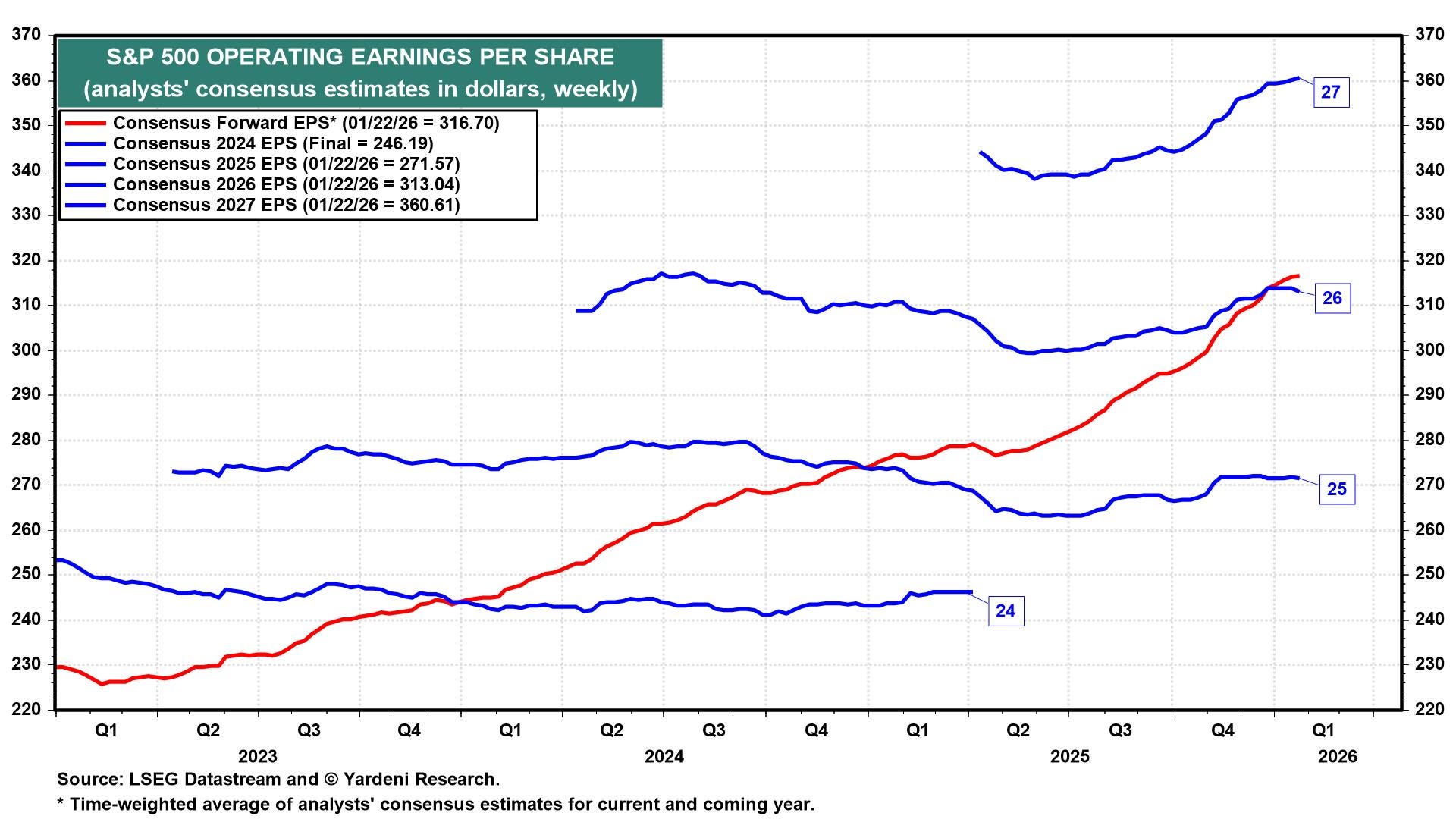

S&P 500 Forward Operating Earnings: What does Gold and Forward EPS have in common? They go up every day. 2027 EPS are tagging 360, at 22x forward earnings that would be a SP500 at 7920 by end of year, a 13.5% return. Not so impressive for Gold who is already up 21% YTD.

While a weakening US dollar reduces returns for foreign investors in the S&P 500, it simultaneously creates strong tailwinds for US big tech companies. Roughly half of their revenue comes from overseas, making them highly diversified global businesses with reliable, high-margin cash flows.

There is a meaningful chance that investors will once again flock to the Magnificent 7 on this basis. In periods of uncertainty, long-only US equity investors have repeatedly gravitated toward these dominant names.

But is the current broadening of the US stock market a lasting shift, or merely a fad? I believe it is the latter. Consider two possible scenarios:

The market continues to broaden, with capital flowing from the Magnificent 7 and the broader S&P 500 into riskier small- and mid-cap stocks. Unlike the Mag 7, these smaller companies are not high-margin cash generators; they are cyclical businesses with structurally lower returns on equity. As valuations expand for small caps, multiples on large caps would compress. If this valuation rerating fails to attract fresh capital, it would likely be because earnings are deteriorating. After all, if large-cap earnings continue growing at the current pace (more than 20% for tech and over 13% for the S&P 500 overall), investors would quickly step in to buy these high-quality companies at more attractive valuations. Conversely, if large-cap earnings weaken, small- and mid-cap earnings would almost certainly decline even more sharply. In today’s economy—dominated by technological monopolies and economies of scale—any rotation out of large caps is unlikely to be smooth or sustainable. Broadening can only persist for a limited time; it cannot become a new secular trend. At best, it is a short-lived cyclical phenomenon.

The recent small-cap outperformance fades, and mega-cap tech rebounds on the back of strong earnings growth. A weaker dollar would trigger upward revisions to earnings estimates for US multinationals. By year-end, market concentration would likely increase again, with the S&P 500 potentially trading at 23–24× forward earnings—implying an index level between 8,280 and 8,640.

To me, the S&P 500 will either thrive on continued concentration or suffer from its unwind. That is the mechanical reality of today’s US equity market. If global decoupling is genuine and other developed economies are truly cutting ties with US tech giants, then concentration would indeed decline—but only after a significant de-rating in valuations. The only way this would not happen is if the US government and the Federal Reserve respond with aggressive stimulus on a scale comparable to extreme monetary experiments (Project Zimbabwe becoming a reality). Regardless of the path, the SP500 will end up much higher in the long term.

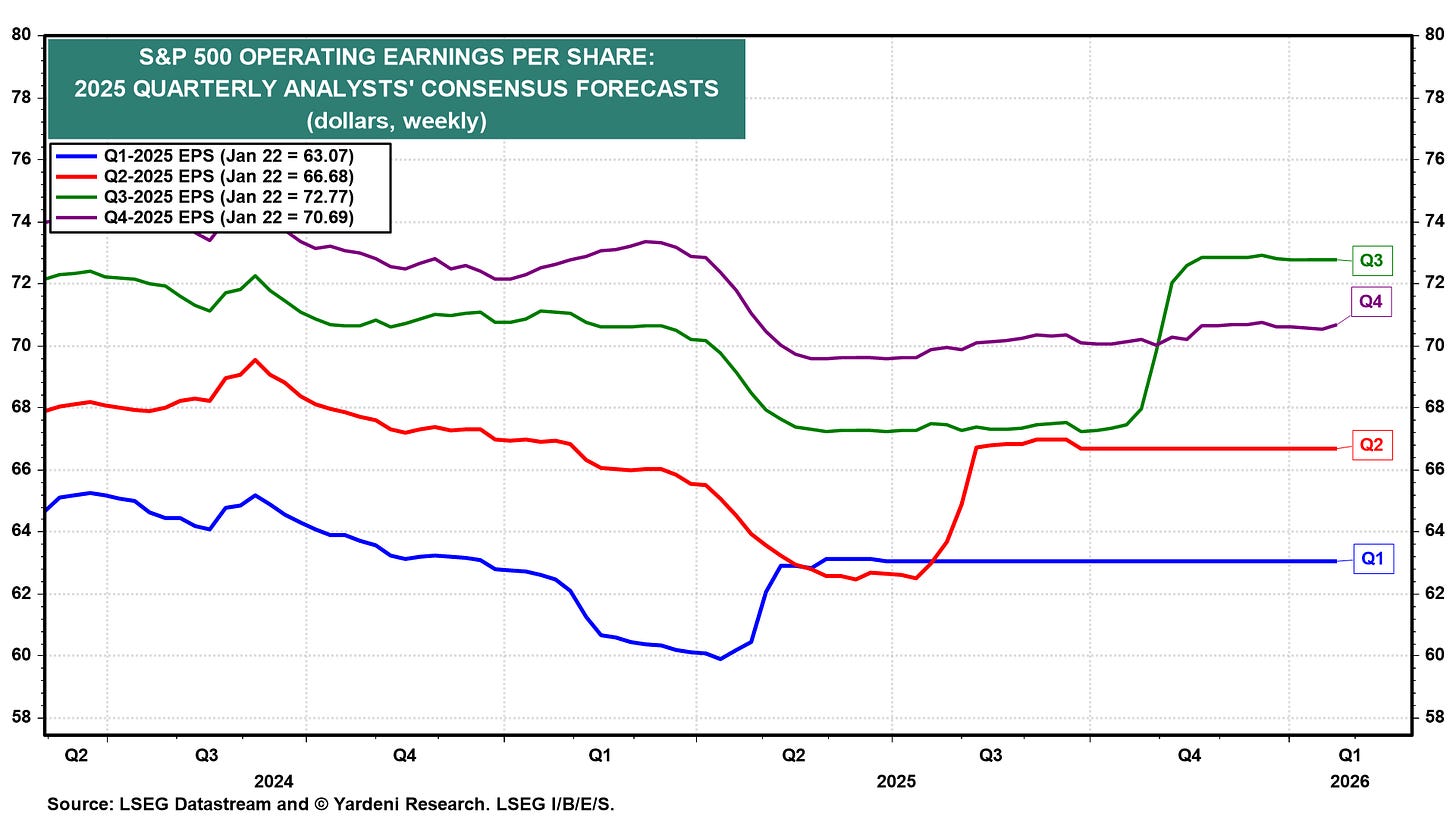

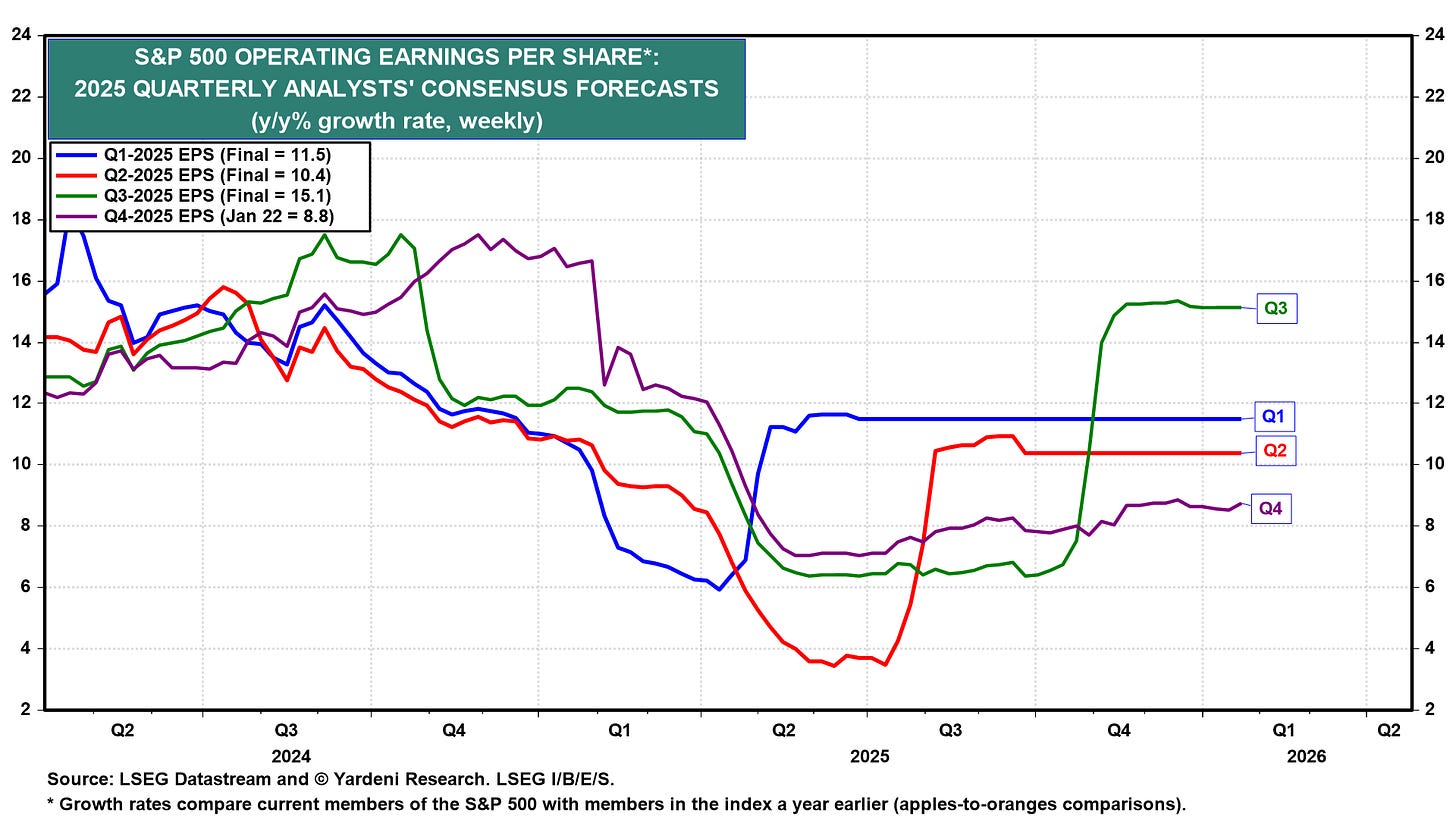

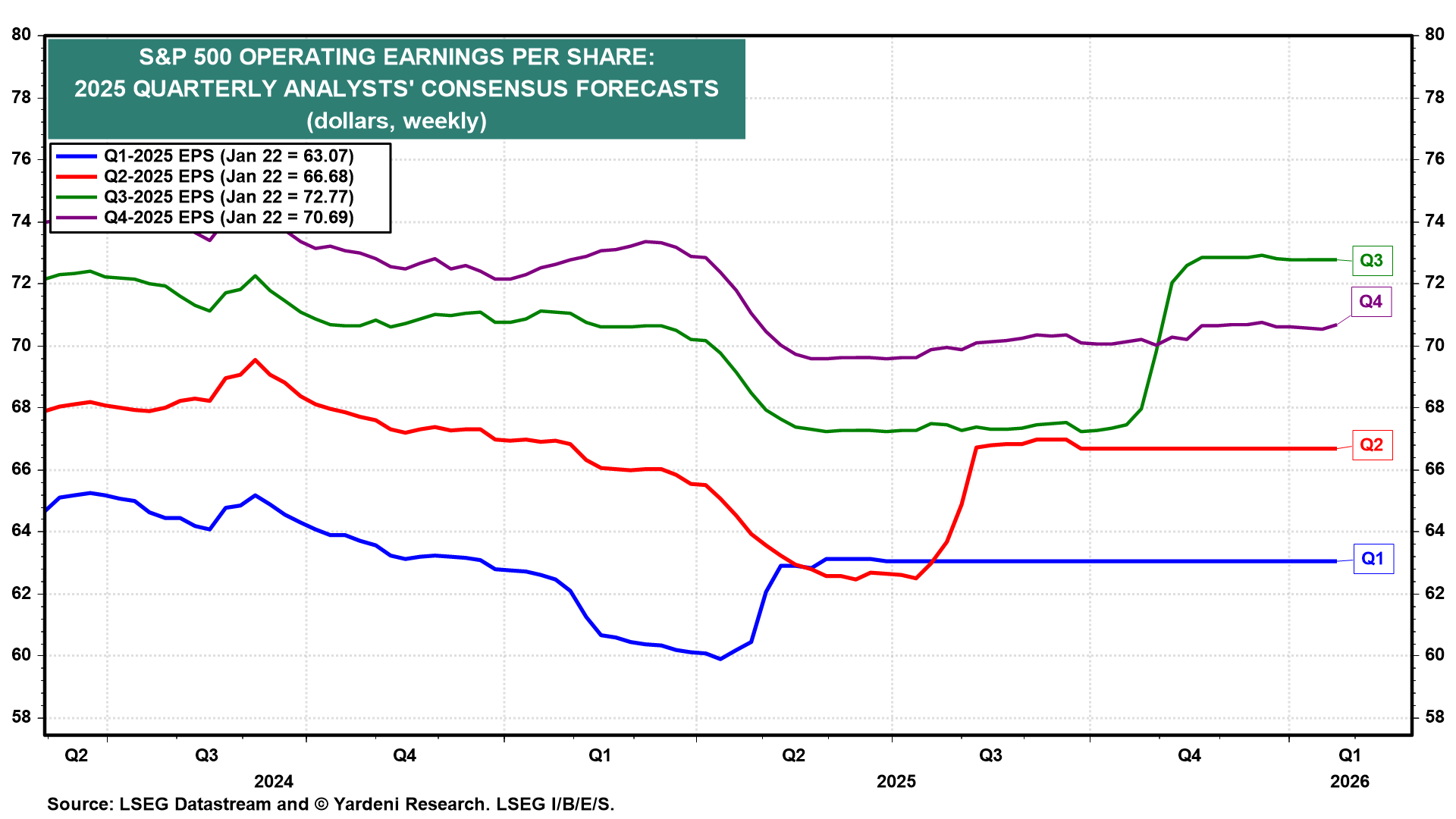

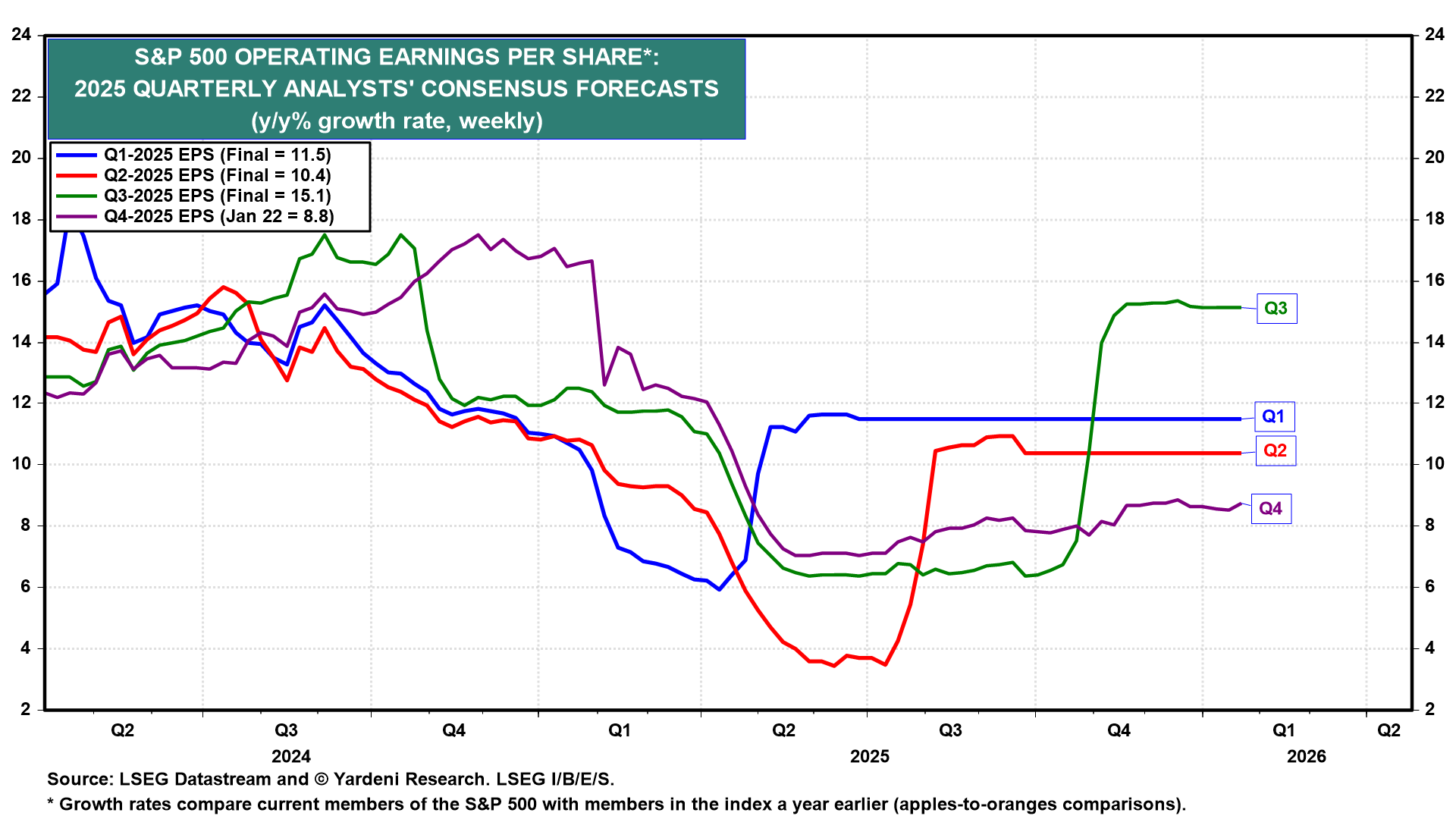

On a more tactical note, the current earnings season is quite interesting in terms of expectations. As pictured below, the Q4 2025 forecasted EPS dipped last year during Liberation Day, but it has been gradually recovering. Usually, analysts tend to revise their estimates downward a few months before the actual earnings season. This time, it didn’t happen, and analysts have actually been increasing their forecasts. Some market watchers may think contrarily and point to optimistic earnings results.

I am more inclined to the opposite interpretation: Liberation Day severely depressed the estimates, and analysts have been slowly revising up their earnings, but clearly not enough. It is reasonable to expect Q4-2025 earnings to be much higher; last year we had 18.3% growth realised, but now, one year later, we expect only 8.8%? And the AI trade is still booming? TSMC and AMSL earnings gave an early sign of the momentum still pushing earnings higher. (I wrote this part yesterday, in the meantime MSFT and META released earnings and are increasing capex on the back of higher revenues).

With the dollar down and low earnings expectations, I would not be surprised to see the SPX nearing 7000, pushed by tech companies. My only concern is the heavy positioning, extreme bullish sentiment. But if you ignore that, we could potentially be looking at a higher SPX in a couple of weeks, unless geopolitics throw us a curved ball. In any case it is going to be volatile either on the upside or downside.

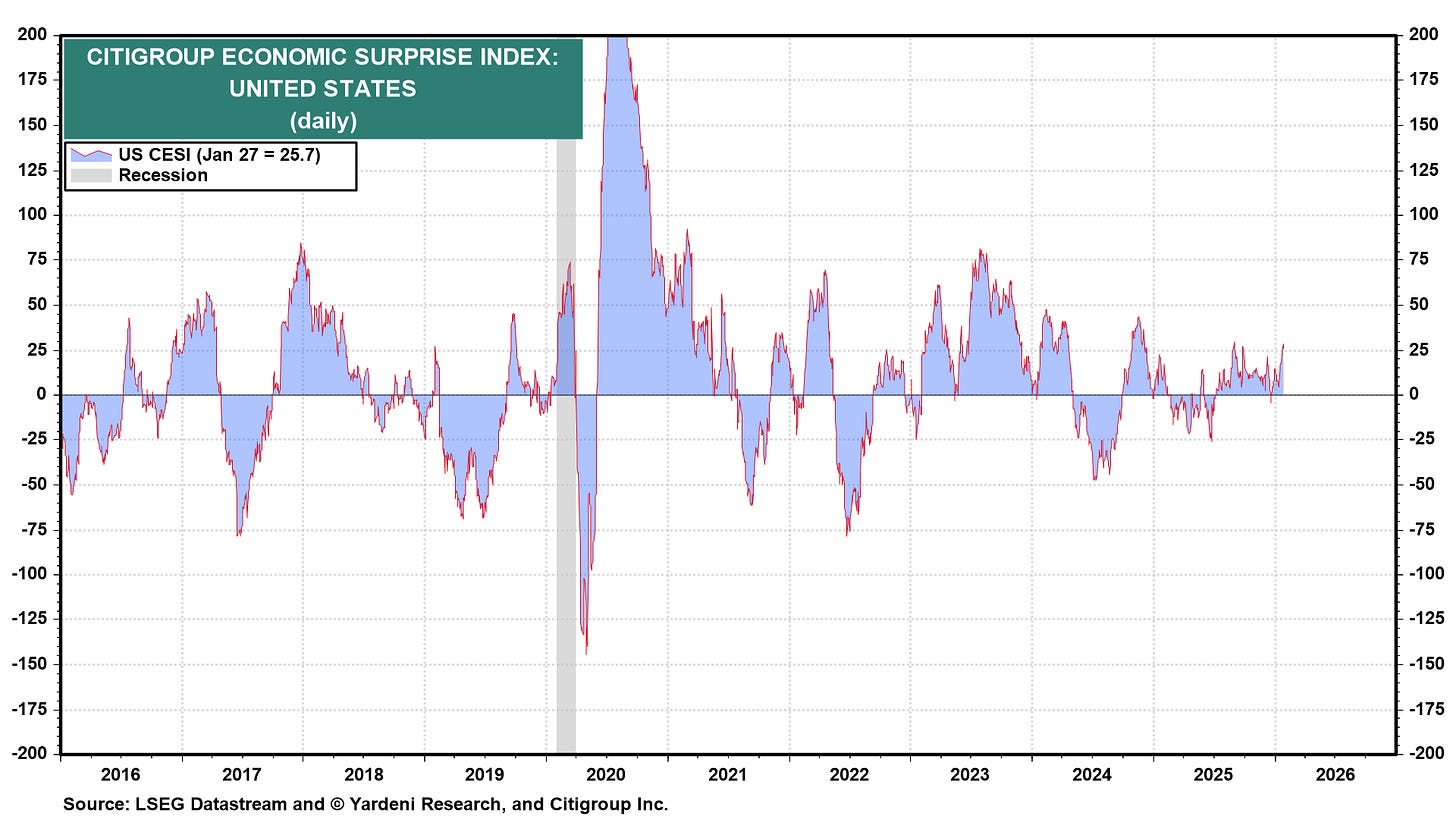

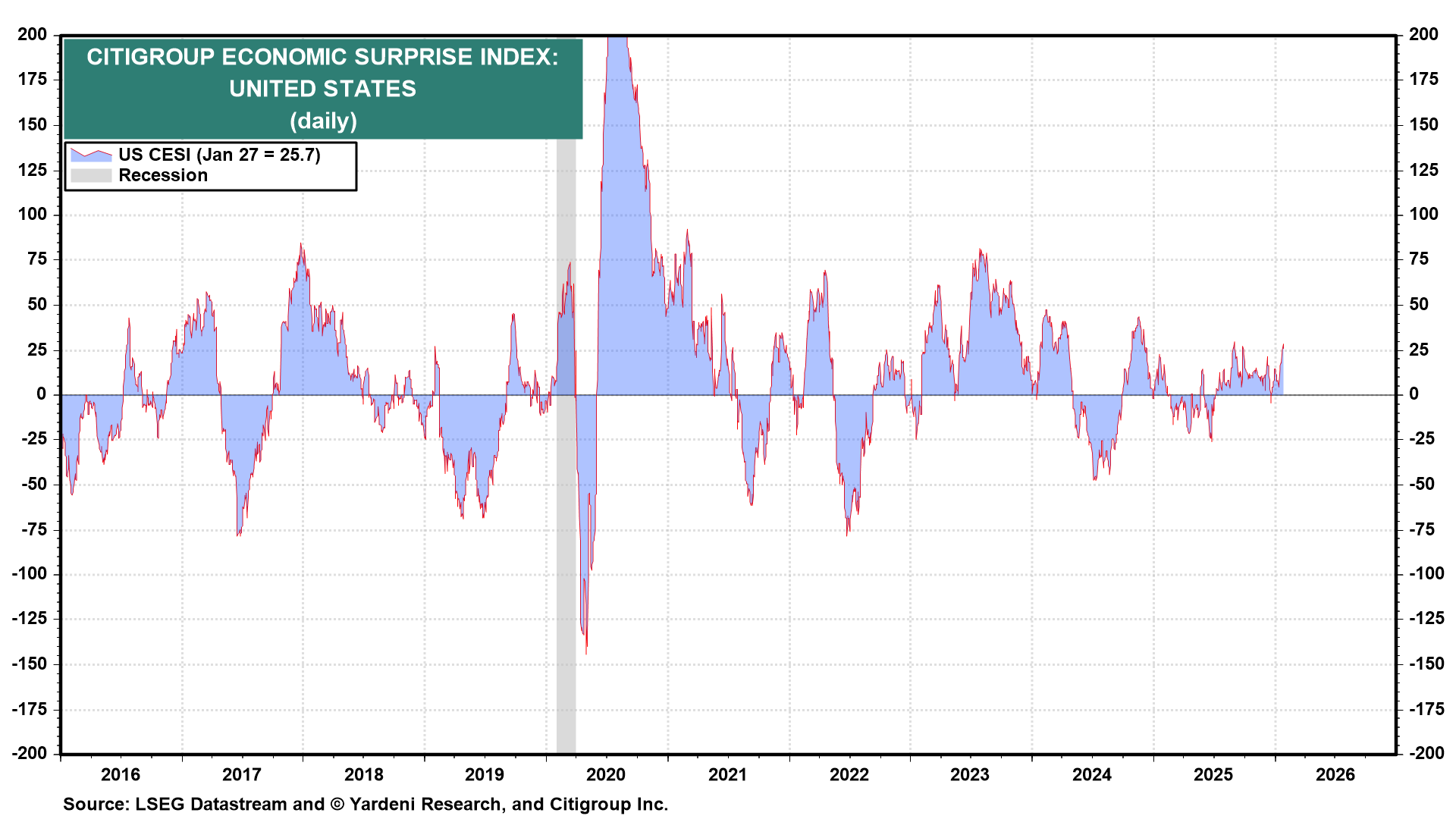

US Economic Surprise: The CESI index is now firmly positive. The economy is indeed “running hot,” but nothing extremely out of line compared to expectations (the CESI index measures economic release surprises, not absolute values).

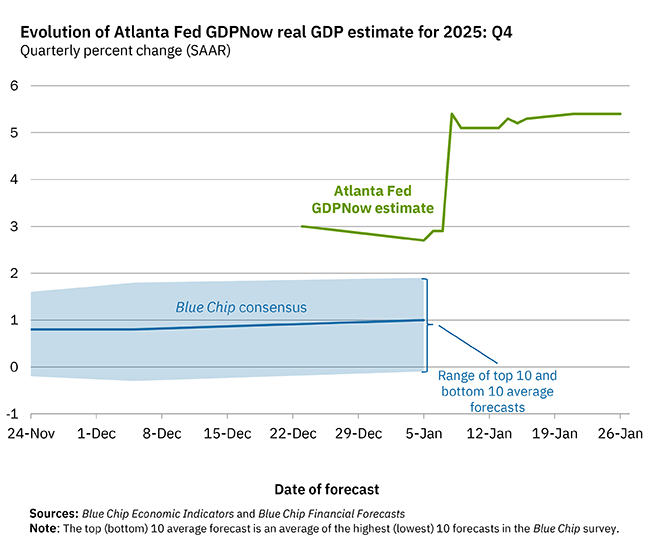

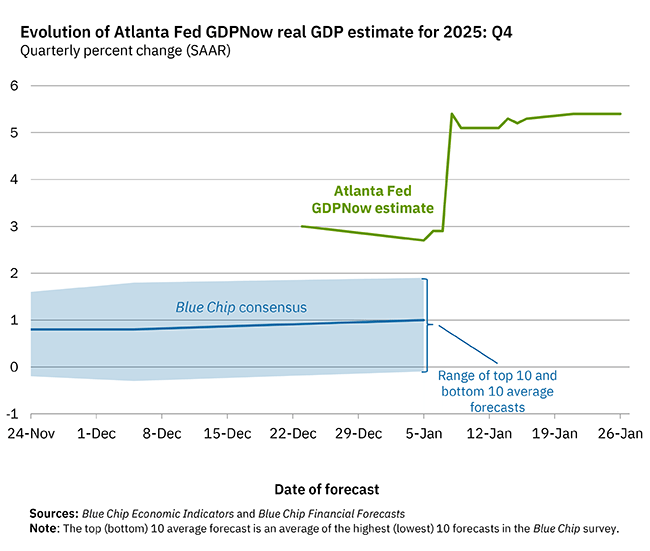

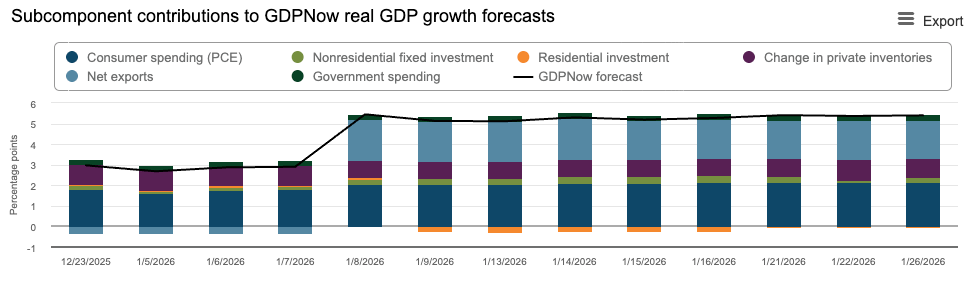

GDP Nowcast: The headline number is running above 5% (that’s real GDP, not nominal!), but that number is overestimated by large net exports, stemming again from gold. The real headline number is around 3%, which is a solid figure. Once again, the Blue Chip consensus looks way too low.

Labor Market

I’m dedicating a full section to the job market in this post. The situation is nearly unique. As we’ve seen—and as everyone knows—the economy is growing quickly, and so is the stock market. Yet the job market has been stalling. It’s fair to say that these conditions are genuinely puzzling. Warren captured it perfectly in the post below:

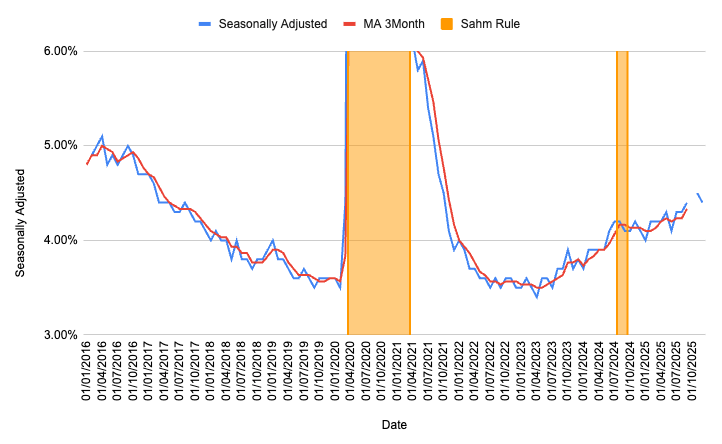

As seen below, the unemployment rate is still rising; we triggered the Sahm Rule six months ago, but no recession is in sight. Actually, it looks more like a boom than anything else.

The unemployment rate can climb through several mechanisms:

Layoffs (bad for the economy)

Quits (not bad for the economy)

Mismatch between requirements of open jobs and available skills in the labor force (awkward but not bad for the economy)

Hiring freeze (can be either good or bad, depending on the cause)

Technological displacement or automation (potentially disruptive but often positive long-term)

New labor force entrants or re-entrants (neutral to positive for the economy)

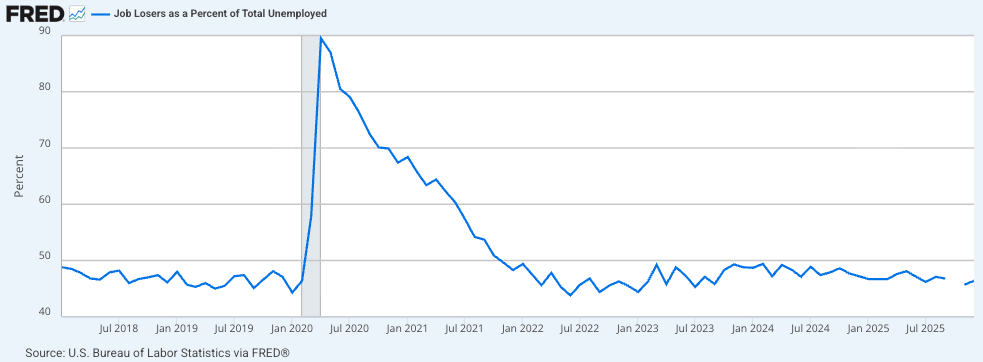

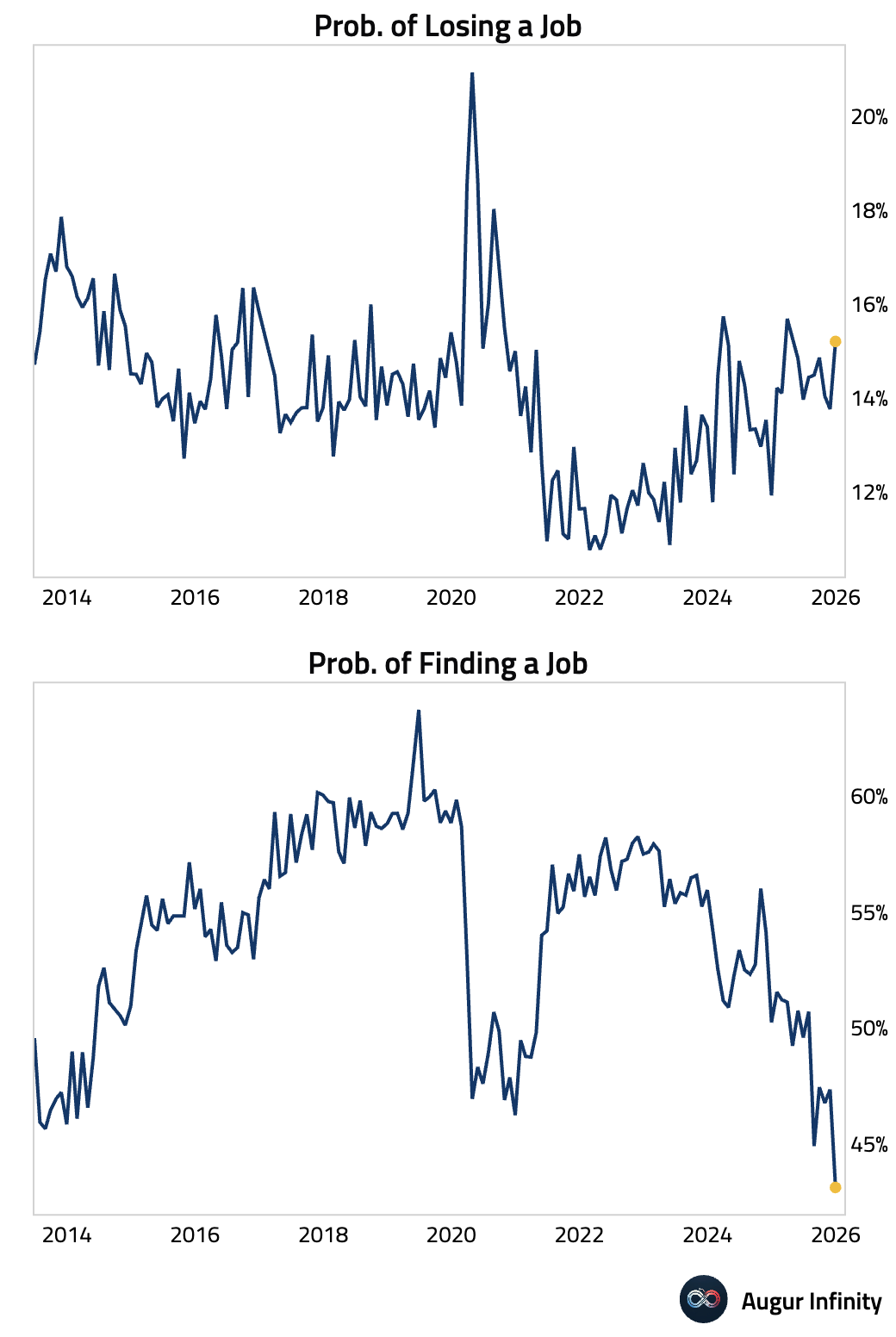

What’s the data telling us? First, and that’s great news, we can rule out layoffs. The ratio of job losers as a percent of total unemployed remains very low:

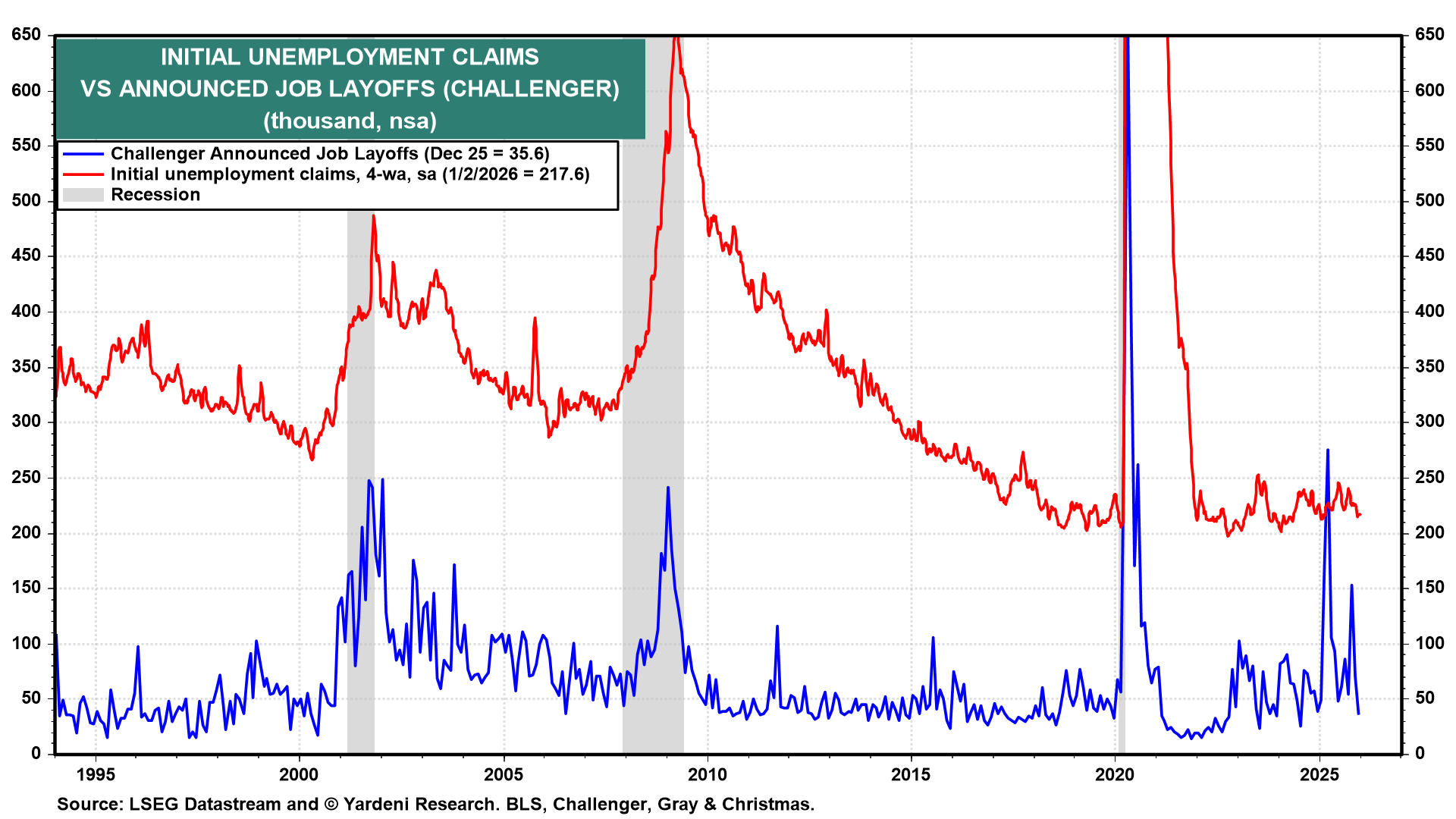

Initial claims and Challenger-announced layoffs, both timely indicators, are at their lows. Challenger had some spikes that spooked everyone, but it doesn’t seem like the layoffs were for economic reasons.

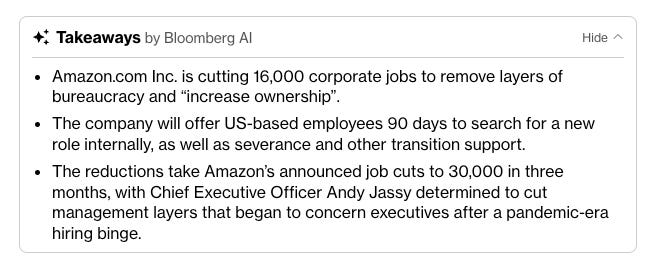

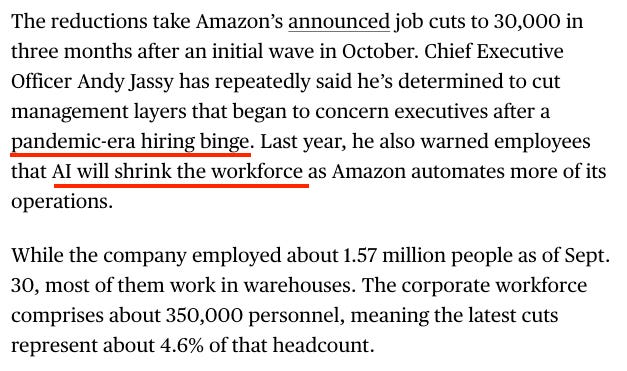

Instead, what seems to be happening is a continued re-normalization from the pandemic-era hiring binge at large companies, along with a strong push toward automation. The following article from Bloomberg is from yesterday:

Bloomberg: Amazon to Cut 16,000 Corporate Positions to Trim Bureaucracy

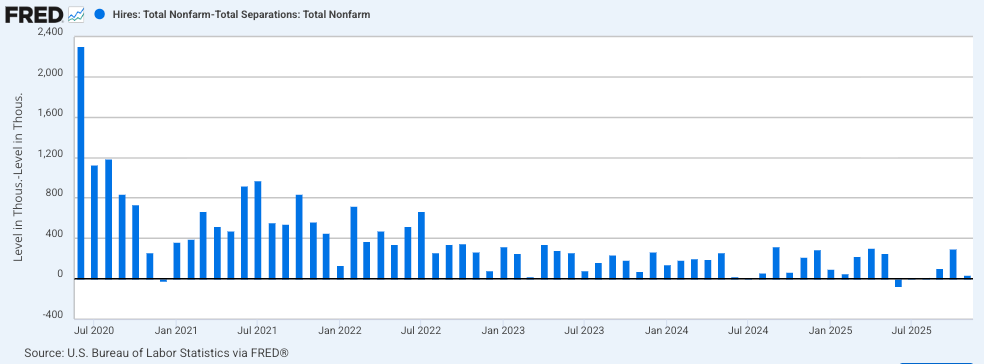

An indicator I also like to follow is JOLTS hires minus separations. What we see here is a job market at equilibrium: despite a slightly rising unemployment rate, hires are outpacing layoffs.

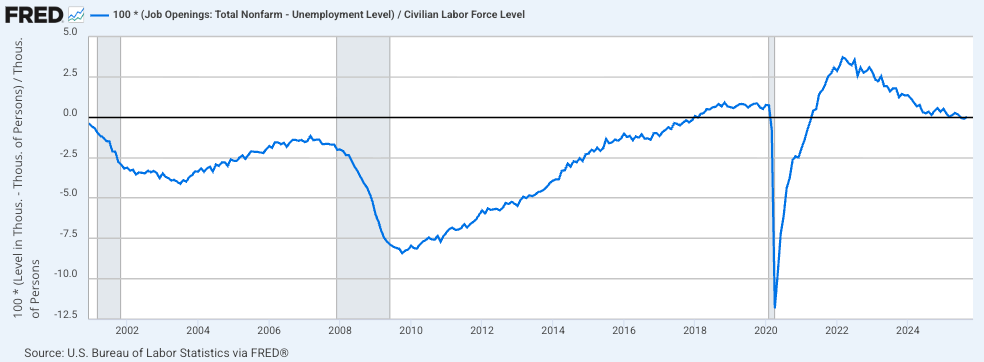

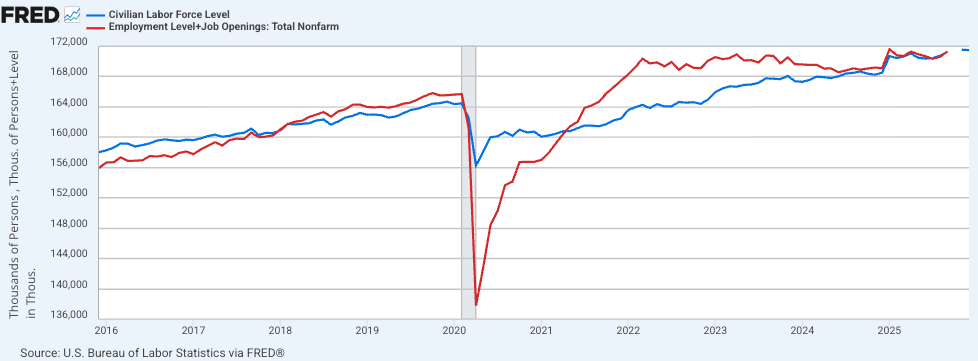

The chart below represents what we call the jobs-workers gap. The big gap in 2022 created the hiring binge, but we are back to an equilibrium where each worker could theoretically find a job.

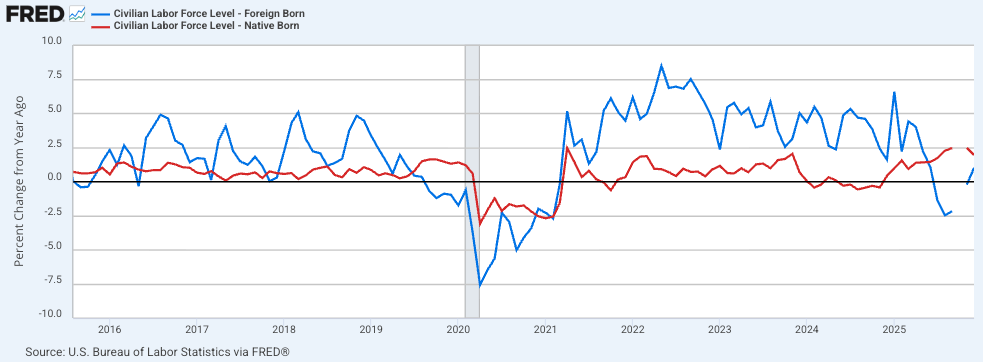

If these workers can’t find jobs, the remaining reason is a skill mismatch, as the US economy is rapidly evolving. Probably because of the sudden drops in the foreign-born labor force, many jobs were not filled while the labor force has been rising steadily. This supports the skills mismatch thesis.

This mismatch between labor skill demand and labor skill supply could be the reason why the “vibe” from US workers is still very depressed. The New York Fed’s consumer survey points to growing anxiety about the labor market. Perceived job security has worsened, and confidence in finding new employment has slumped to the lowest level since the survey began.

Once again, we have a big gap between feelings (soft data) and reality (hard data), or what everyone is now calling the K-shaped economy.

The most likely way to escape this K-shaped economy is through wage increases. Indeed, everyone enjoys a nice pay rise, don’t you? But what would trigger wages to accelerate?

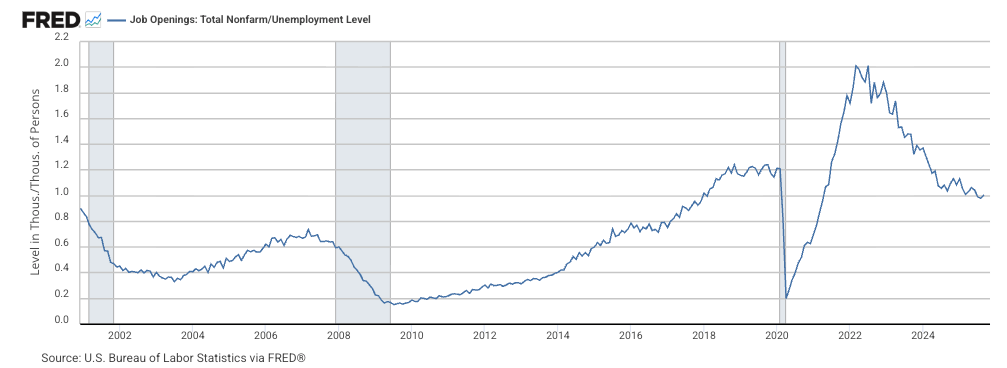

Currently, wages are still decelerating and returning to the pre-pandemic upward trend. To resume a positive trend, the job market will need to tighten. There is a decent chance we will see this happening in the near future. The key indicator to follow is the ratio of vacancies to unemployment (often called the V/U ratio or vacancy-to-unemployment ratio). It measures labor market tightness, with a higher ratio indicating more job openings per jobseeker.

This ratio seems to be bottoming, which suggests wage growth is bottoming out too. And if wages are stabilizing at these lows, then one of the main drivers of inflation is doing the same. The other two big ones are energy and shelter. More details in the inflation section.

Bottom line: The unemployment rate has been rising for technical reasons, such as the hiring binge in 2021, a mismatch between the requirements of open jobs and the available skills in the labor force, and, to some degree, technical disruption from AI. None of these factors is negative for the economy or the stock market; in fact, they are very supportive.

Inflation

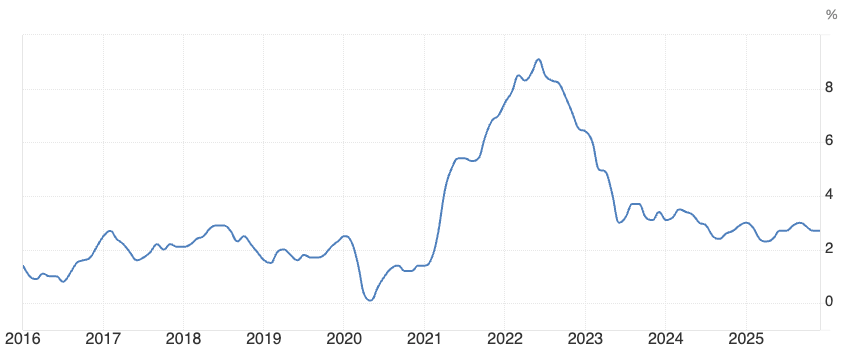

CPI: As of December 2025, the official year-over-year inflation rate stands at 2.7%, still above the Fed’s target. But you should get used to it by now; 3% is the new 2%.

Inflation Expectations: Michigan Consumer inflation expectations are still renormalizing post-Liberation Day. It is interesting that the 5Y expectation has been in an uptrend since COVID. This is another symptom of the debasement trade/mindset.

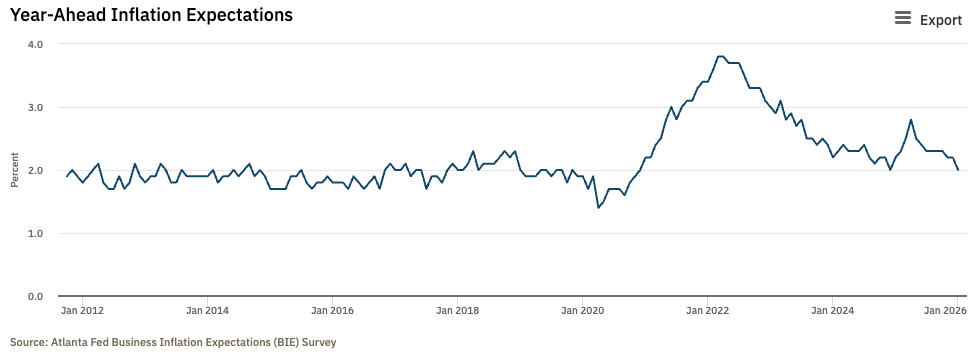

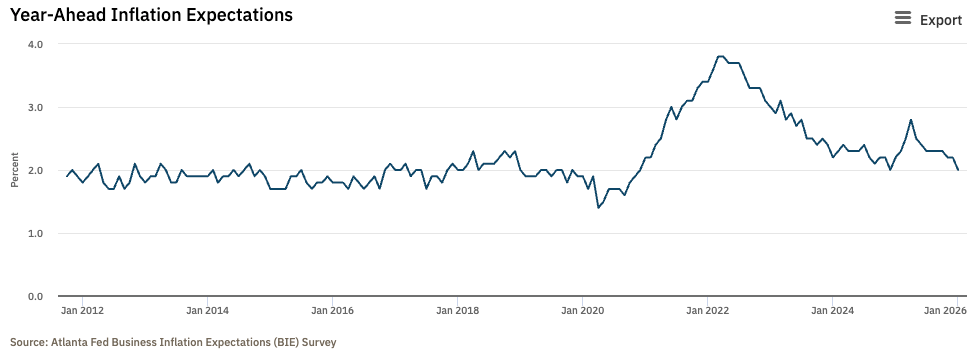

The Atlanta Fed Business Inflation Expectations Survey is now back to its pre-tariff level. Tariffs were not as inflationary as feared; their effect is similar to that of a tax as opposed to a subsidy. One is disinflationary, while the other is inflationary.

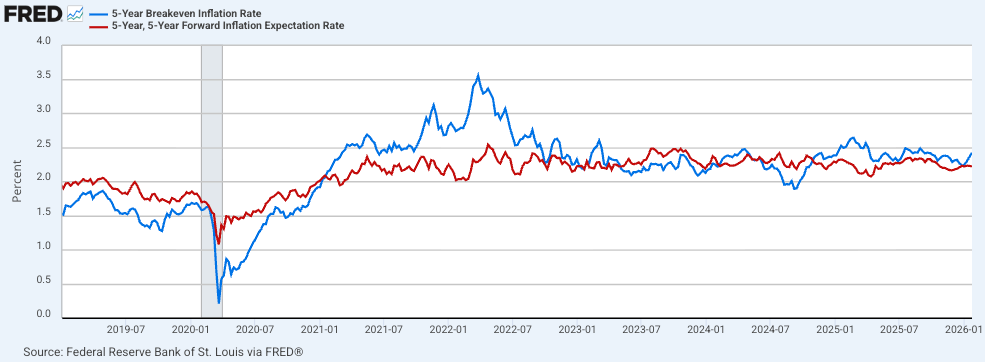

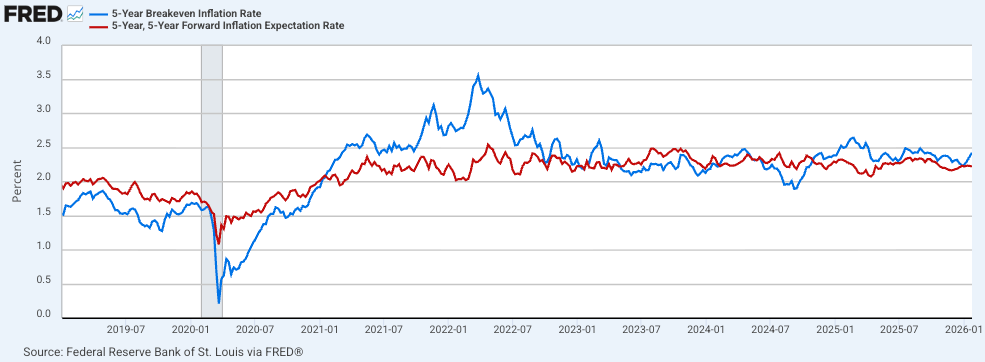

Inflation Swaps: The 5-year and 5-year forward breakeven inflation rates are still in the same range, going basically nowhere.

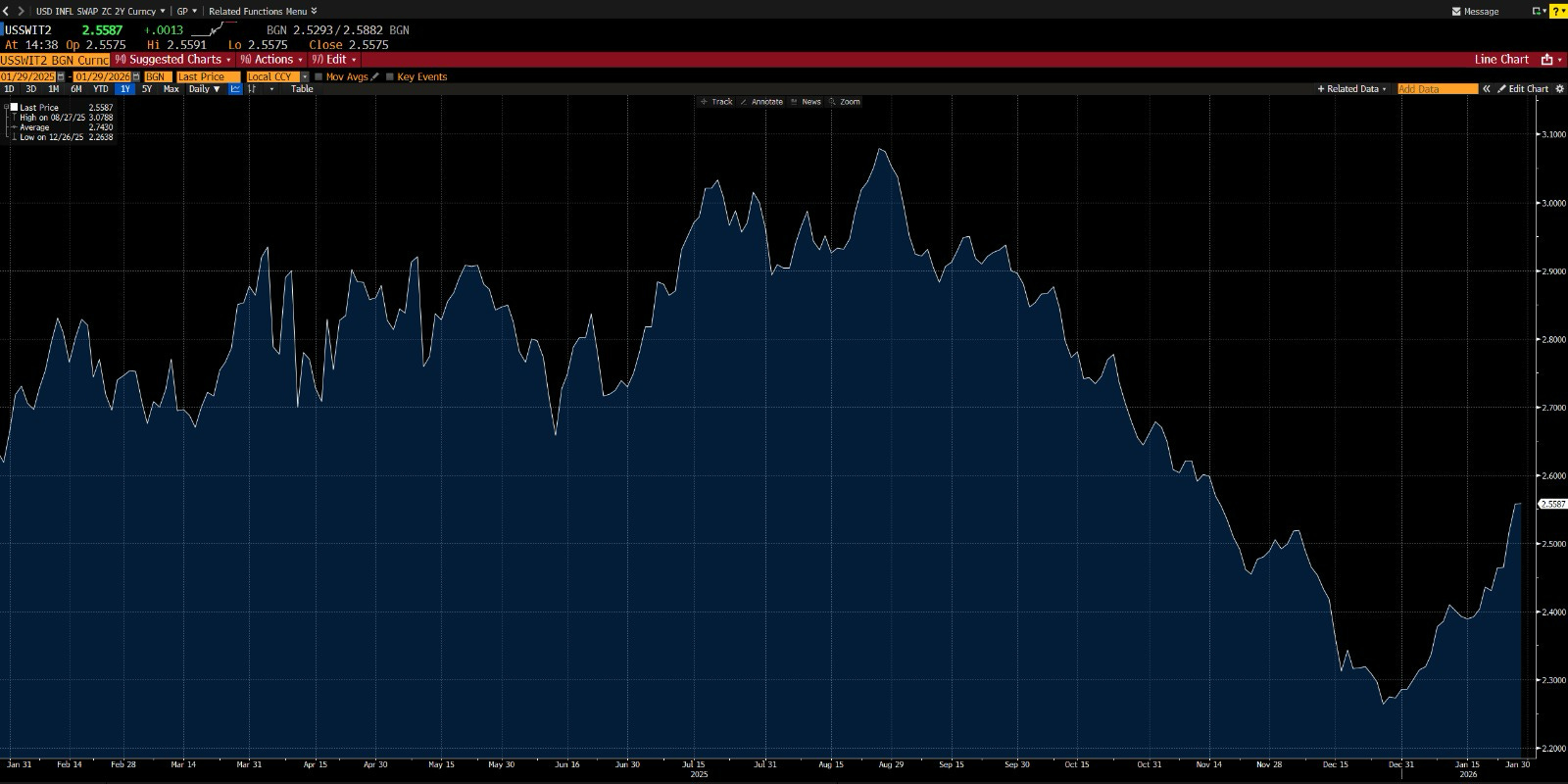

And 2-Year inflation swap is back to 2.55% after a steep decline.

The inflation picture is not concerning in the immediate future; both the backward-looking CPI and the forward-looking inflation expectations remain anchored. Inflation is structurally higher and now runs at a constant rate of around 3%, the new floor post-COVID and the fiscal bonanza.

The three broad vectors of inflation, namely wages, shelter, and energy, have been a tailwind for the cyclical disinflation. This is well identified by now and fully priced in by the market.

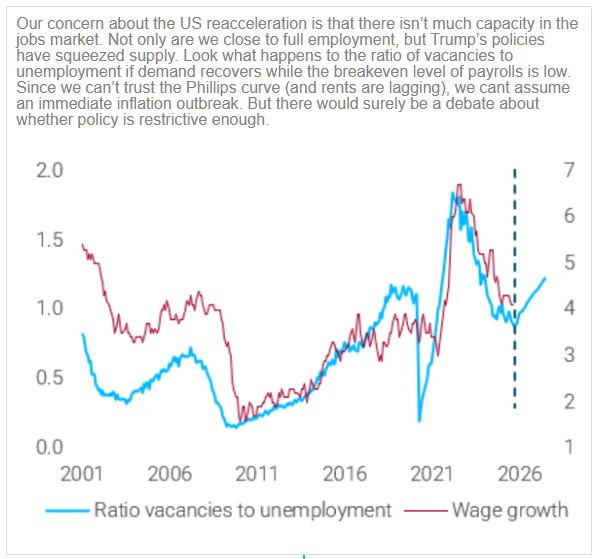

However, I am starting to get on edge. The structural forces are still here with us: fiscal deficit, debasement mindset, elevated asset prices pushing the wealth effect ever higher. The job market is stabilizing and might tighten from now on; the structural force at play is the lopsided demographic pyramid. As seen in the labour market section, the vacancies-to-unemployment ratio could shoot higher, leading to higher wages. And higher wages more often than not mean higher shelter prices.

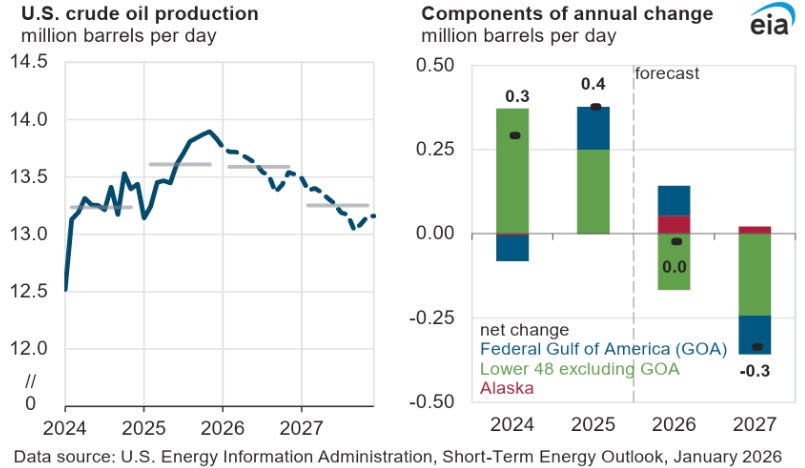

Regarding energy, the current bull market in commodities is somewhat unusual, with very narrow participation from precious metals. It is natural to expect the bull market to broaden into other commodities, and in particular oil. Yes, there is still a lot of oil in storage and at sea, but that is cyclical; again, the structural forces point toward higher oil prices. US crude oil output is bound to decrease, Venezuela is just smoke and mirrors, and Iran poses an immediate geopolitical risk that is yet to be fully priced in.

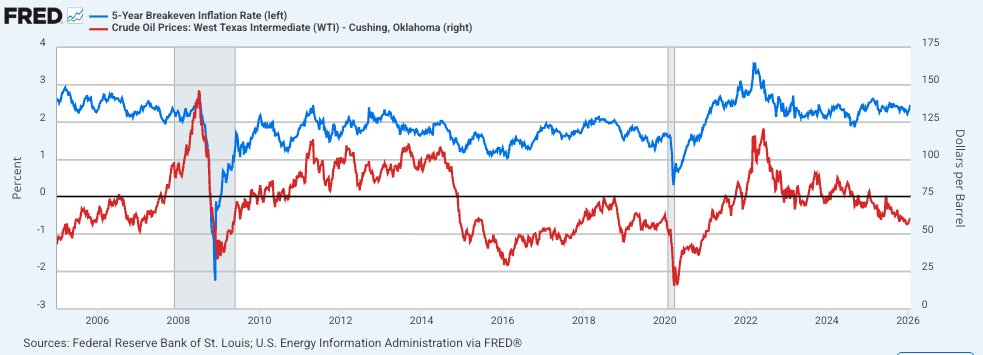

The chart below shows a near-perfect correlation between metals performance and U.S. 5-year breakeven inflation.

Oil is also extremely correlated to the 5-year breakeven inflation rate. It will be the transmission vector to close the jaws of the above chart.

In conclusion, inflation is not an immediate risk, but the risk-reward has shifted tremendously: the cyclical forces behind the disinflation are getting exhausted while the secular inflationary forces are only increasing in strength, and the explosive rally in precious metals could spur the next inflation leg. In that environment, it is very difficult to be long bonds or any duration-sensitive assets. In the next post, we will link this to the Fed’s monetary policy and their reaction function, but there is a decent chance the Fed will be too late again, especially if they lose their independence. No bueno for TLT.

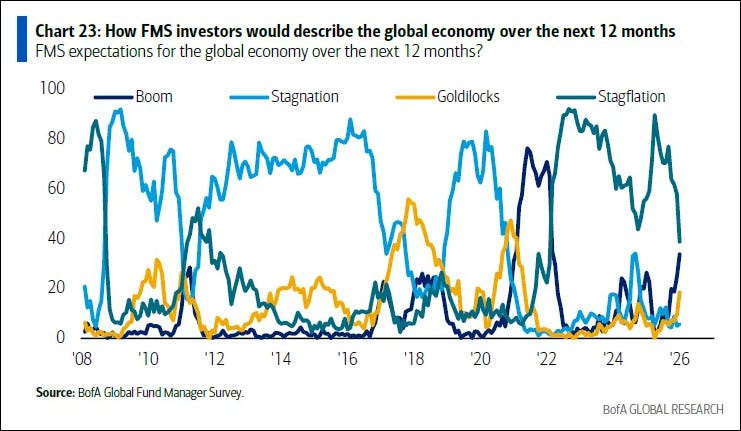

The economy is at risk of becoming too hot. This is not consensus yet, but market participants are seeing it coming: a BOOM.

“The U.S. economy has remained resilient. While labor markets have softened, conditions do not appear to be worsening. Meanwhile, consumers continue to spend, and businesses generally remain healthy. These conditions could persist for some time, particularly with ongoing fiscal stimulus, the benefits of deregulation and the Fed’s recent monetary policy.” – JPMorgan Chase ($JPM ) CEO Jamie Dimon

That’s it for today, see you tomorrow for Part II.