Macro Update #35

Nothing has changed according to Mr. Market

The Nothing Ever Happens crowd is, once again, looking very smart right now. The playbook around geopolitical shocks held up perfectly: a selloff followed by a V-shaped recovery. And again… The bear case always looked so appealing at the bottom, so of course, most of us did not profit from the situation, and bears did not lock in profits at the bottom. Yep, I fell for it again.

The macro picture: nothing has changed (yet)

Let’s start with some macro fundamentals to better understand where we stand.

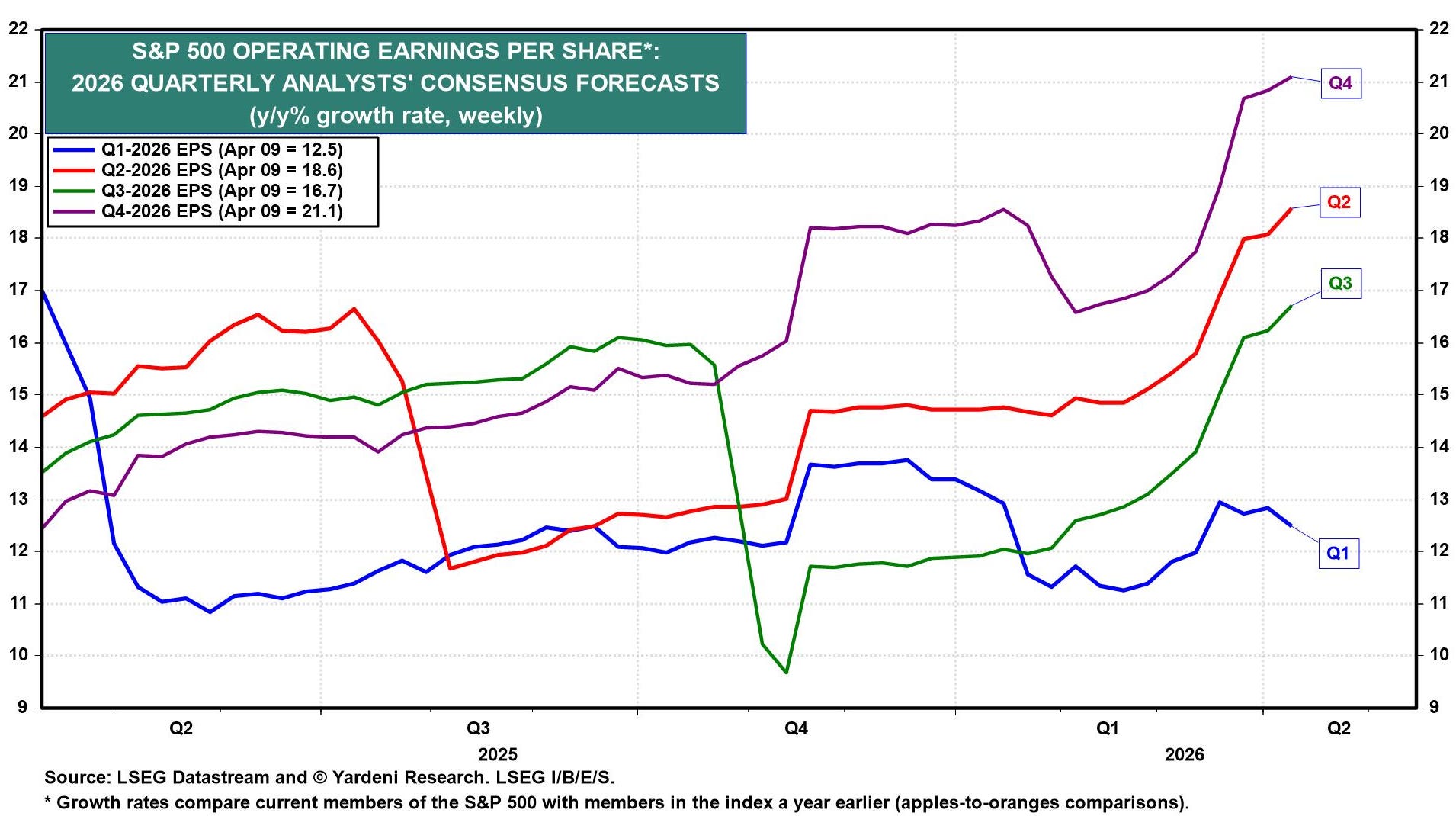

Growth: Resilient

Forward EPS for the S&P 500 did not flinch at all during the conflict. On the contrary, they are still ripping. Every single quarter of 2026 is expected to grow at double digits.

Sector wise, the re-rating higher is mainly coming from:

Tech sector: In 3 months, the revenue growth has been revised from 20.2% to 27.4%. Oof! Profit margin expansion? Productivity gains? Layoffs? Probably a bit of all that. In any case, numbers are going up.

Energy sector: From a depressing -3.1% contraction, analysts have revised up their estimate to +1.6%. This is the second highest jump in forward earnings across all sectors. And all it took was the Strait of Hormuz to be closed!

Are analysts now too optimistic? This is a legit question to ask now. The increase in estimates helped to push the forward P/E lower, and yes, stocks were looking pretty damn fair valued on an NTM basis in the midst of the Iran selloff. But now that we have retraced all the move (and more!), the bar has now been set quite high for the upcoming earnings season. Which means the forward guidance from the C-suites will be absolutely critical. A make-or-break moment with no clear-cut risk-reward.

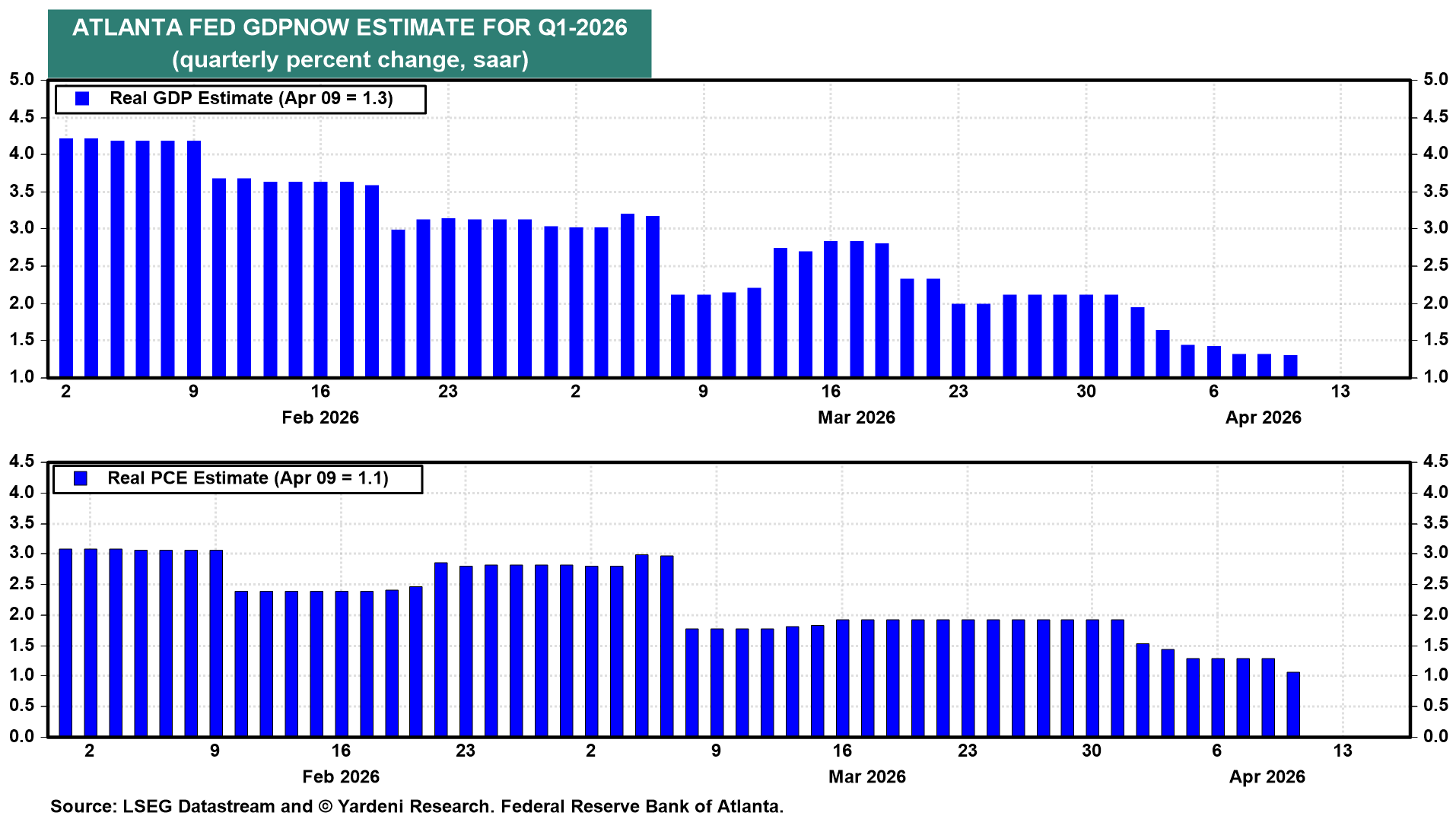

The pessimists will point toward the soft Atlanta GDP nowcast:

Headline GDP is always noisy because of exports and imports and other shenanigans. Real PCE and Final Sales help us cut through the noise, and here again it is not looking so great. According to Yardeni, this is a weather effect from the extreme cold during last winter. I can personally vouch for that. I had the delightful experience to be in New York during the polar vortex. -15 degrees Celsius in the street. Yeah, you don’t really want to shop in that weather!

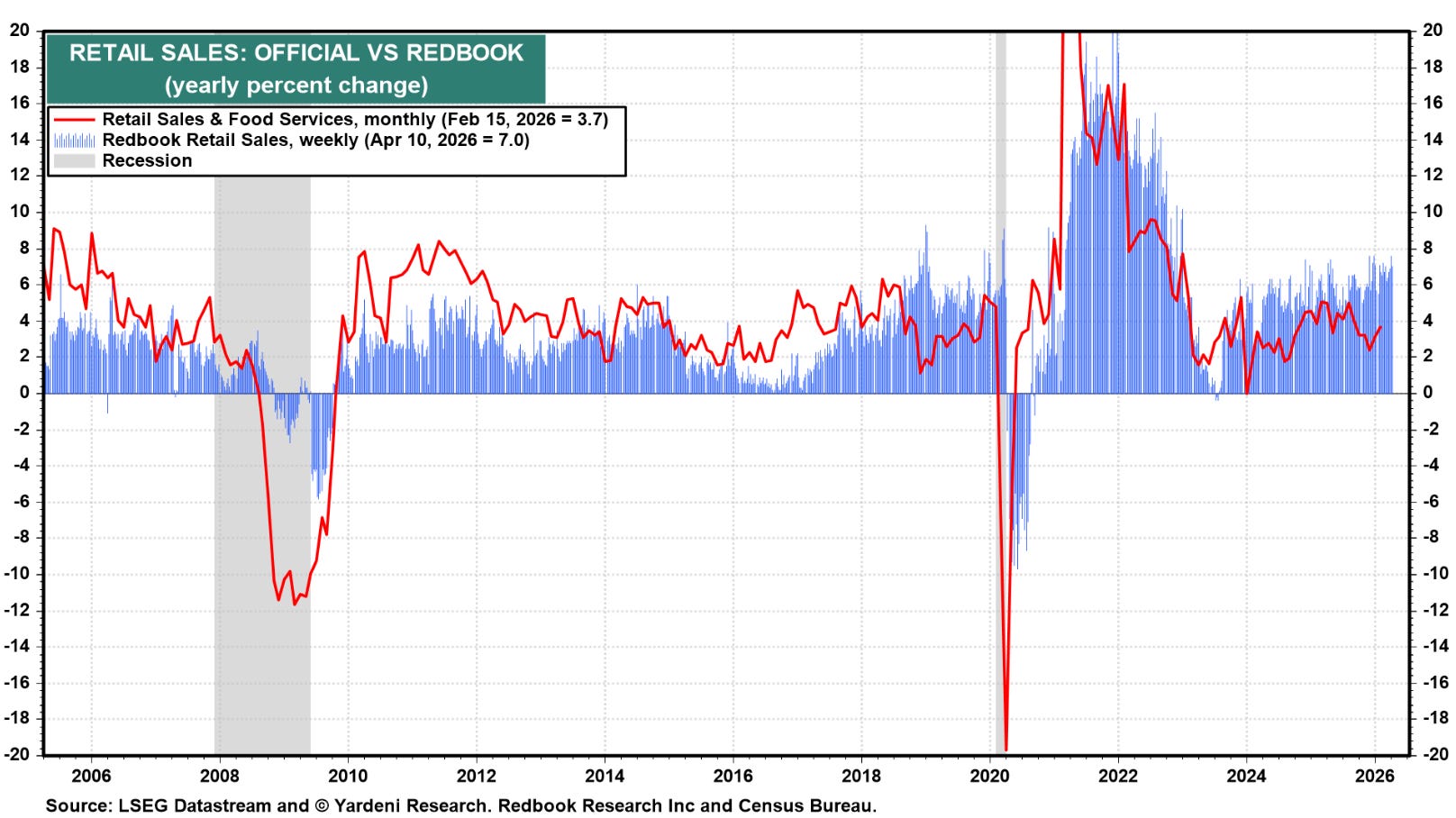

Redbook retail sales doesn’t put as much weight on leisure and other weather-dependent activities, and it is pointing toward a strong consumer.

The story remains the same. Inflation or not, the American consumer remains resilient because most of the consumption is coming from the upper K, and that’s what the stock market cares about, not how the average American consumer feels (sentiment is horrendous).

“I think the higher-end consumer, the premium consumer, is candidly immune or becoming more immune to the headlines and not delaying their investment in the experience economy, waiting to see what the next headline’s going to be on the margin.... I think as difficult as it is to see what’s going on with the conflict in the Middle East, I’m not sure that our premium customers are feeling affected by that.” – Delta CEO

“...net sales for the month [of March] came in at $28.41 billion, an increase of 11.3% from $25.51 billion last year. March had one less shopping day versus last year due to the calendar shift of Easter. This negatively impacted both total and comparable sales by approximately 1% and 1.5%. Reported comparable sales for the month were as follows: U.S., 8.7%; Canada, 10.7%; Other International, 11.9%; total company, 9.4%; digitally enabled 23.3%.” - Costco, Director of Financial Planning

Inflation: Still under control

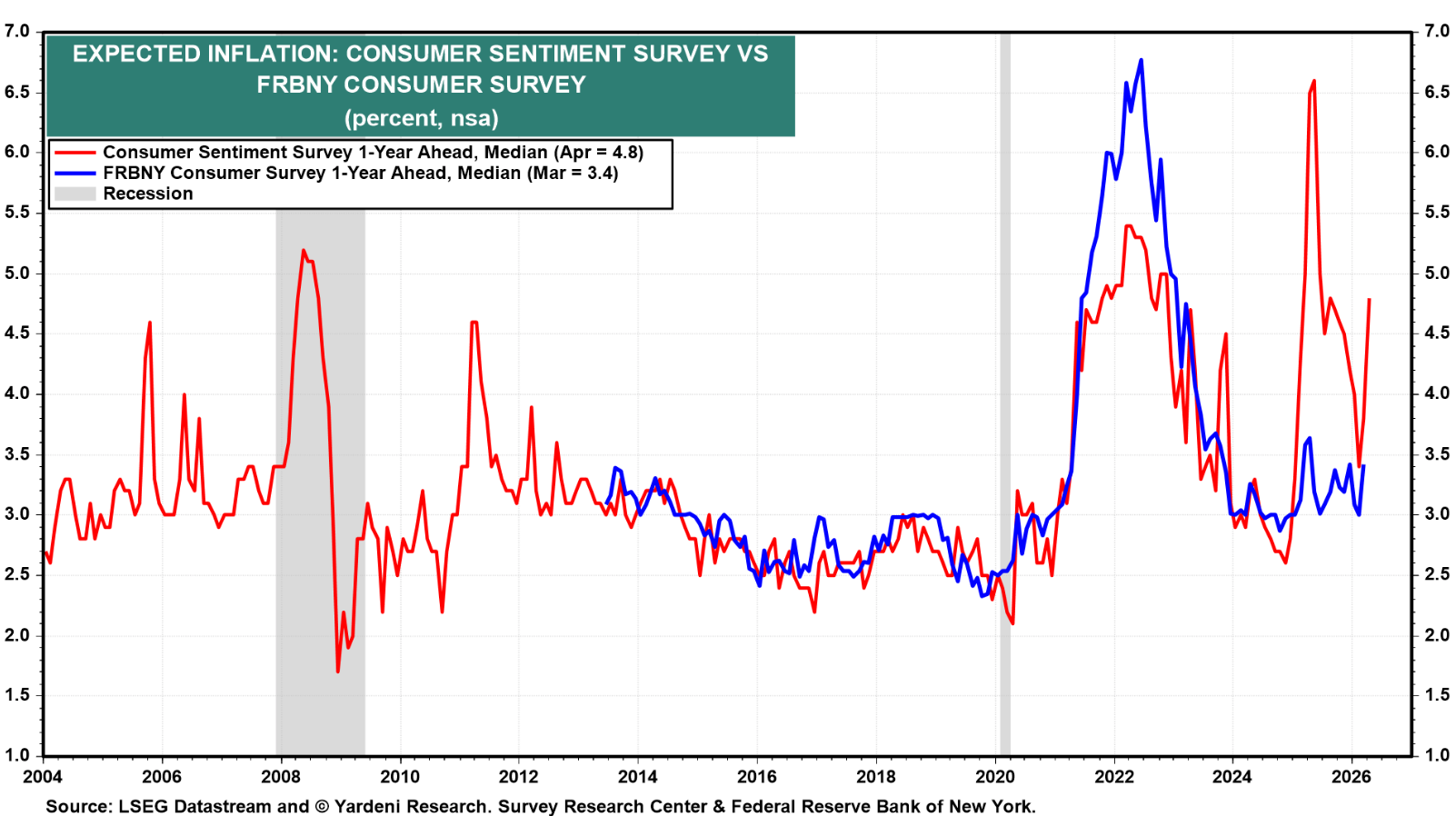

Expectations might start to be unanchored over a one-year-ahead basis. The FRBNY survey is still showing a tame outlook, but the Consumer Sentiment Survey is spiking once again.

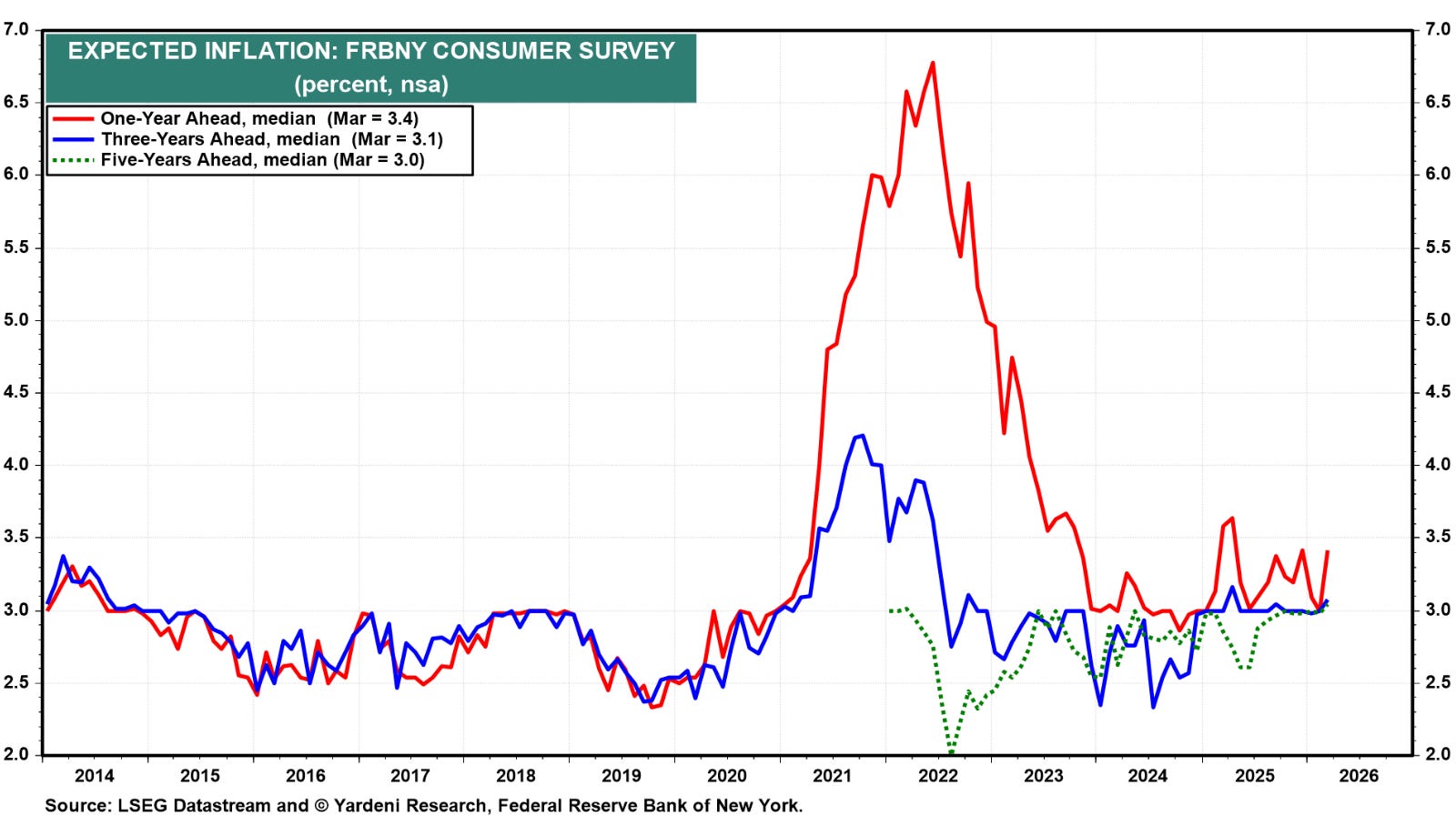

One-year outlook is not the most important horizon. The Fed will look through any short-term bump; however, they will not let the long-term expectations rise (3-years and 5-years). So far, these expectations are still anchored, and the Fed is in no rush to raise rates. Wait and see.

What about the inflation market? 5-Year breakeven inflation rates are notoriously correlated to the price of oil. The recent oil shock is still not feeding through the 5-Year Breakeven.

Kevin Muir, from the Macrotourist, wrote a very good post on the shorter-term inflation rates.

While the point of the post was to debunk a popular post on X regarding collapsing inflation breakevens, the main takeaway from the 1-year and 2-year inflation swaps is that the market has repriced a bit higher the inflation expectations, but we are absolutely nowhere near the horrendous situation of 2021 and 2022.

The inflation market is also looking through the Iran conflict. A short-term bump in inflation is expected, but it will be transitory (yes, yes, yes, you’ve heard that before… But we will just have to trust the market on that one).

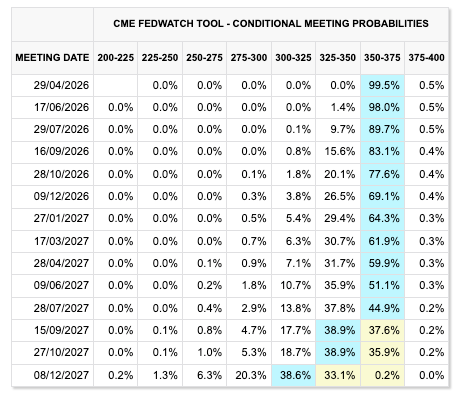

Naturally, the Fed Funds futures market is pricing the Fed to stay on hold for at least a year.

The bottom line for the macro picture is that nothing much has changed. Growth is still positive, forward EPS are climbing, the consumer is consuming, boomers are de-saving and throwing money at the economy, inflation is going higher but not for long, and the Fed is on hold.

And that’s exactly why the stock market is back to where it was before the war.

WELL AT LEAST THAT’S THE CONSENSUS. I AM NOT SAYING IT IS RIGHT OR WRONG, BUT IT IS WHAT IT IS, AND THE MARKET IS DISCOUNTING IT.

→ For the bulls, the closure of the Strait of Hormuz is the most beautiful wall of worry a market can climb.

→ For the bears, the closure of the Strait of Hormuz is the most beautiful slope of hope a market can slide.

In the next post (for paid subs), I will review the selloff from a pure sentiment and positioning perspective. And try to game where things are going with or without a happy ending to the conflict. If the macro picture has not changed, then one can also argue that the predominant themes moving the market before the conflict are still very much alive and worth a review. Finally, I will review the trades opened in the web app.

"Any resemblance with Macro Alf is purely coincidental" 🤣