Mean Reversion Opportunity

Blow off top? Double top? Who cares! New trade and a risk management trick.

Oof…! What a day for silver! My spidey sense was tingling yesterday, and I shorted the Silver March futures after the usual Asian morning pump.

I woke up this morning and I was actually making money on the trade! I quickly proceeded to put my stop loss back to my entry. And sure enough, the Asia morning pump triggered it…

Lesson: Don’t waste your time trying to short an asset going parabolic with 200% realised volatility. It’s an absolute waste of time and energy.

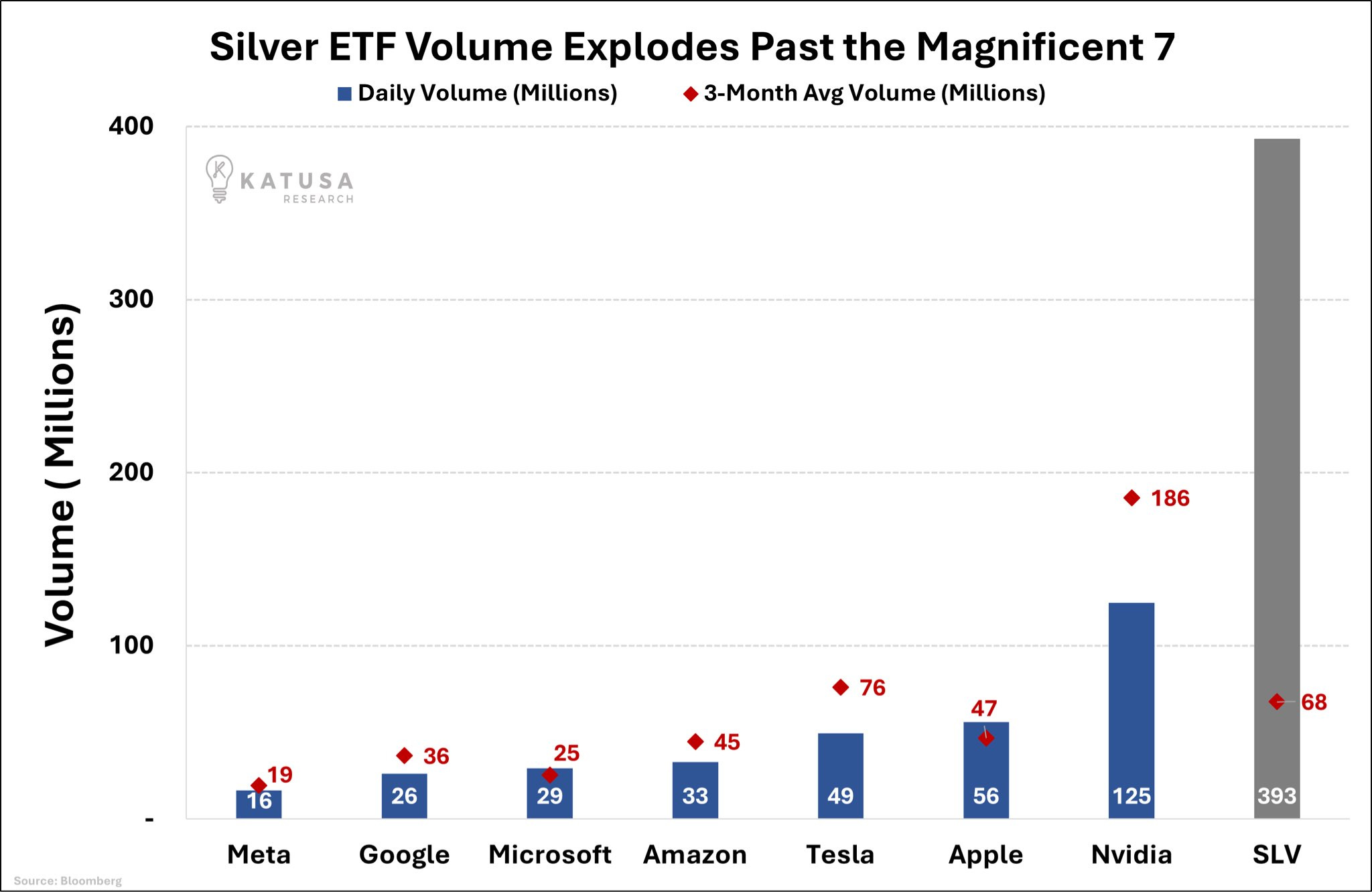

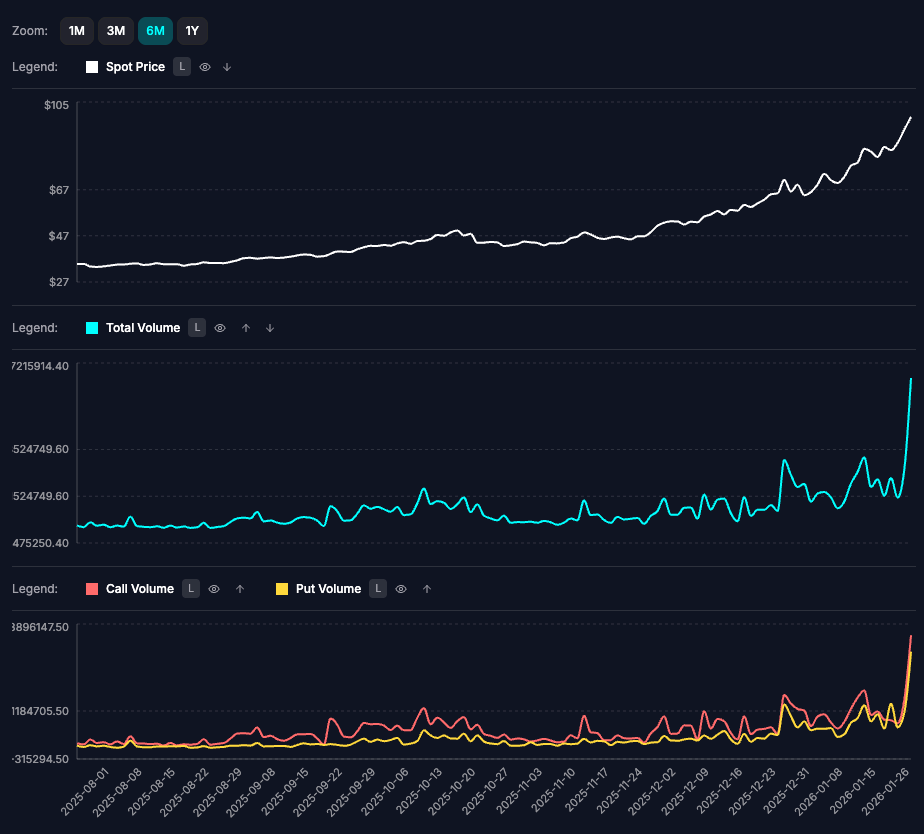

But let’s not give up so easily. Yesterday was truly an epic day for silver. SLV volume EXPLODED:

It seems to be the largest volume ever for SLV. Oof x2!

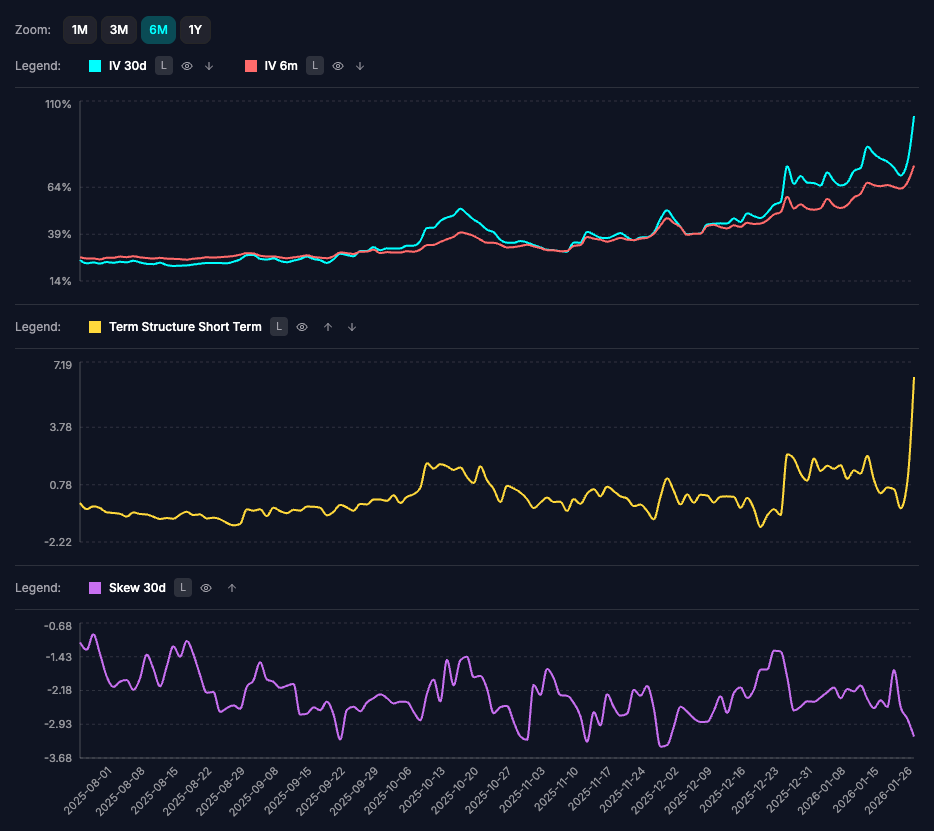

The options market went bananas as well, with call OTM IV going to the moon, especially on the short end of the term structure.

And options volume... Oof x3!

We’ve already reached three “oof”s in just a couple of sentences, so you’re now fully aware that what we’ve seen is some kind of TOP for silver.

Is it THE top?

Or just A top?

Or the first top of a double top?

Who knows? Surely not me. But for now, let’s call it a ZZ TOP!

So, how do you trade a ZZ Top?

Spoiler alert: No, you don’t short silver; you go for the second-order trade.

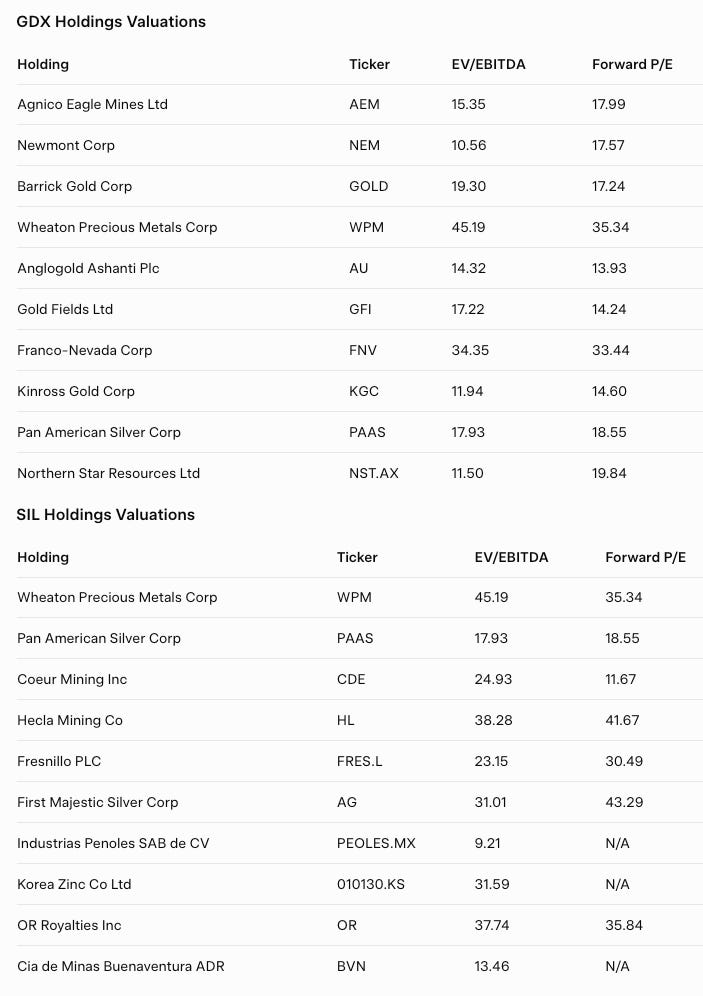

Answer: You trade the relative value between miners, specifically long GDX and short SIL:

I don’t see the signs (yet) of a blow-off top in gold, and gold miners will just keep printing money in the next year. Silver miners, on the other hand, are already priced to perfection. If silver stalls at this price or finds a floor lower—say, at 60 bucks—there risk reward is not there on the long side. In essence, GDX is just a better option if the volatility in silver and gold decreases and we settle around these prices. Silver miners are very prone to underperformance in a flat market.

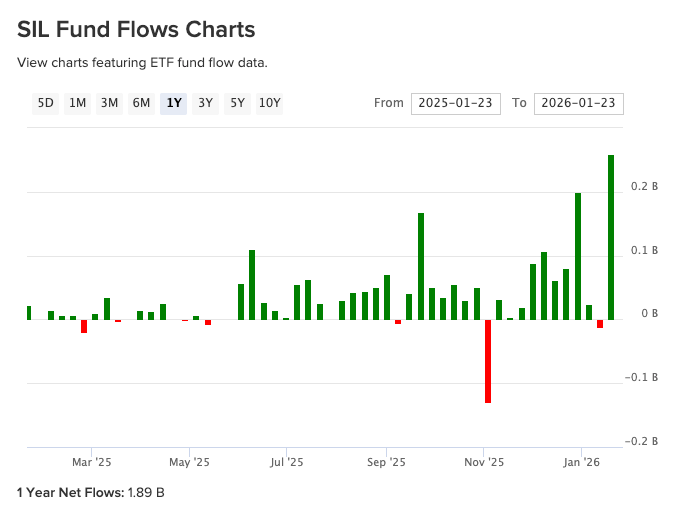

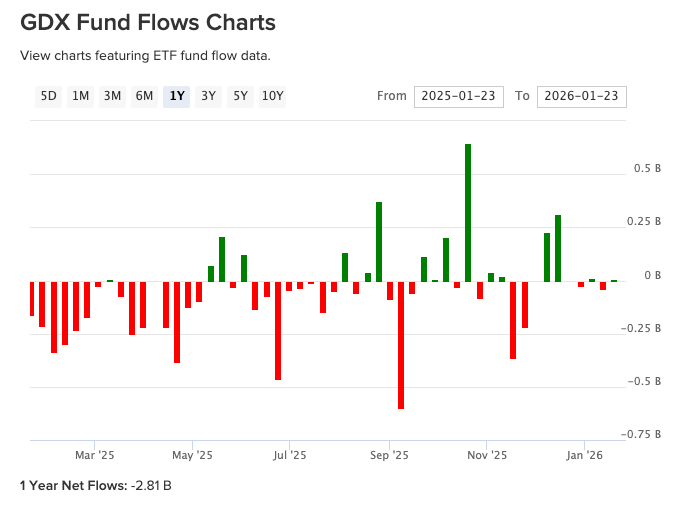

In terms of flows, SIL shows a 1-year net flow of +1.89B, but GDX is actually at -2.81B!

I will enter this long/short trade today. You can use the new feature Long/Short bet for sizing your trade in the web app:

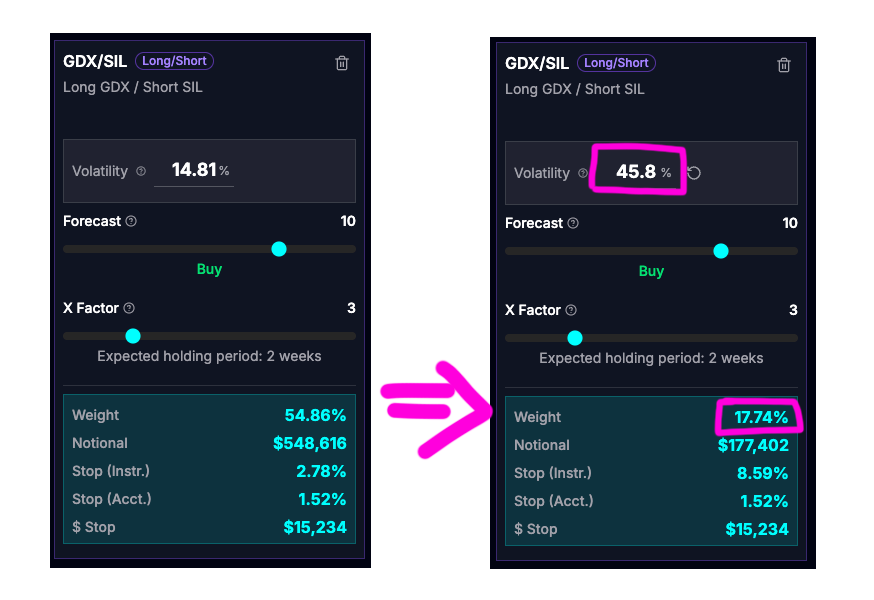

A word of caution, though: the app will use the realised volatility of the historical ratio returns. These two ETFs have been correlated at ~95% in the past month. If the two assets are decorrelating from each other, the volatility of the ratio will be underestimated. The volatility of a long/short portfolio can be computed as below:

GDX and SIL vols are respectively around 40% and 50%.

To be conservative, I would use a coefficient of correlation of 50% (instead of the last measured 95%). This gives us a conservative volatility estimation:

You can override the volatility parameter for this long/short bet inside the web app. It will dramatically reduce the recommended weight. For this theoretical portfolio, it will decrease the weight from 54.86% to 17.74%. This kind of trick is what it takes to avoid blowing up on a long/short trade, or putting your stop loss way too close.

I will open this trade in the web app tonight.

Good luck!

~MH