Positioning Reset

Momentum cracked first, high beta made one last push, shorts were forced to cover, and the index finally "collapsed under the weight of its own delta"

The Positioning Reset Has Begun

For the past month I have been warning that the momentum factor was stretched to the point of absurdity. On May 11, I wrote the following in the chat:

Momentum factor is sooo stretched and highly correlated to Semi and all the AI infra theme. I’m expecting some wild move and potential reversal in the coming days. I’m now outright short SOXX and EWY (Korea). It’s all one big momo trade!

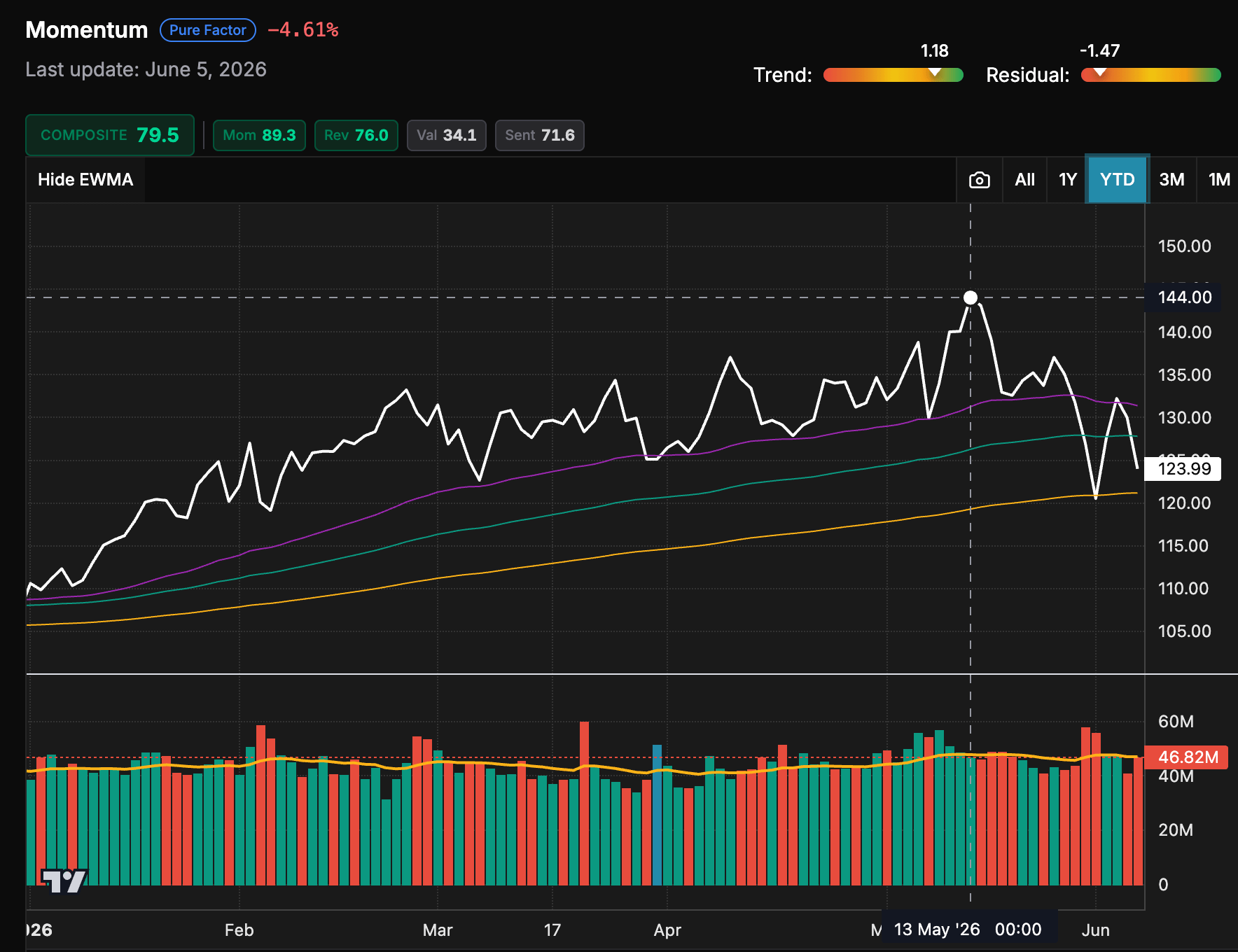

That was the setup. The US long/short Momentum portfolio effectively peaked two days later, on May 13:

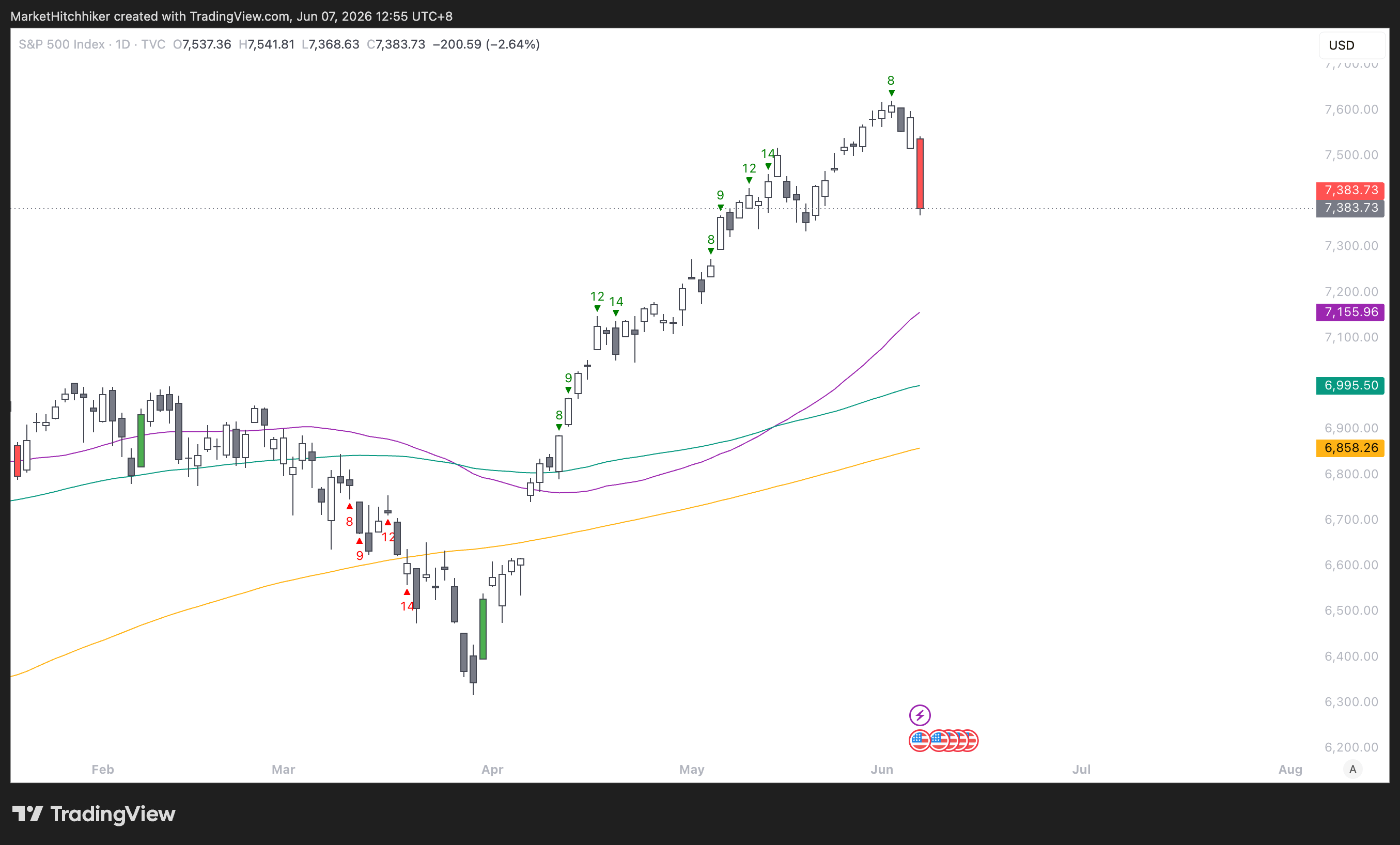

The important point is that the S&P 500 did not peak with it. The index still managed to grind higher all the way to 7,600 before finally correcting a couple of days ago, with that nasty red candle last Friday.

This is where the market became interesting. Momentum had already started to falter, yet the index kept levitating. That last leg higher was not driven by the same leadership (AI infra, semi, energy). It was driven by two late-cycle forces taking the baton after momentum cracked: high beta animal spirits and short-covering in the most hated parts of the market.

Momentum Cracked First

The momentum trade had become one giant AI trade.

Semis, memory, Korea, AI capex receivers, energy, and anything with strong earnings revisions were all sitting inside the same crowded factor expression. Different tickers, same underlying position. Long the winners of the AI capex boom. Short the laggards. Keep pressing as long as revisions stay positive and price confirms.

That trade worked beautifully for a long time. It also became extremely crowded.

Momentum is not automatically speculative. The long leg of the factor was full of real companies with real earnings upgrades. Semis were not meme stocks (initially!). Memory was not a joke. The AI capex receiver theme had fundamental support behind it.

The problem was positioning. When a fundamentally valid trade becomes too consensus. Everyone owns the same names, everyone hedges the same way, and everyone assumes there will be liquidity when they need it.

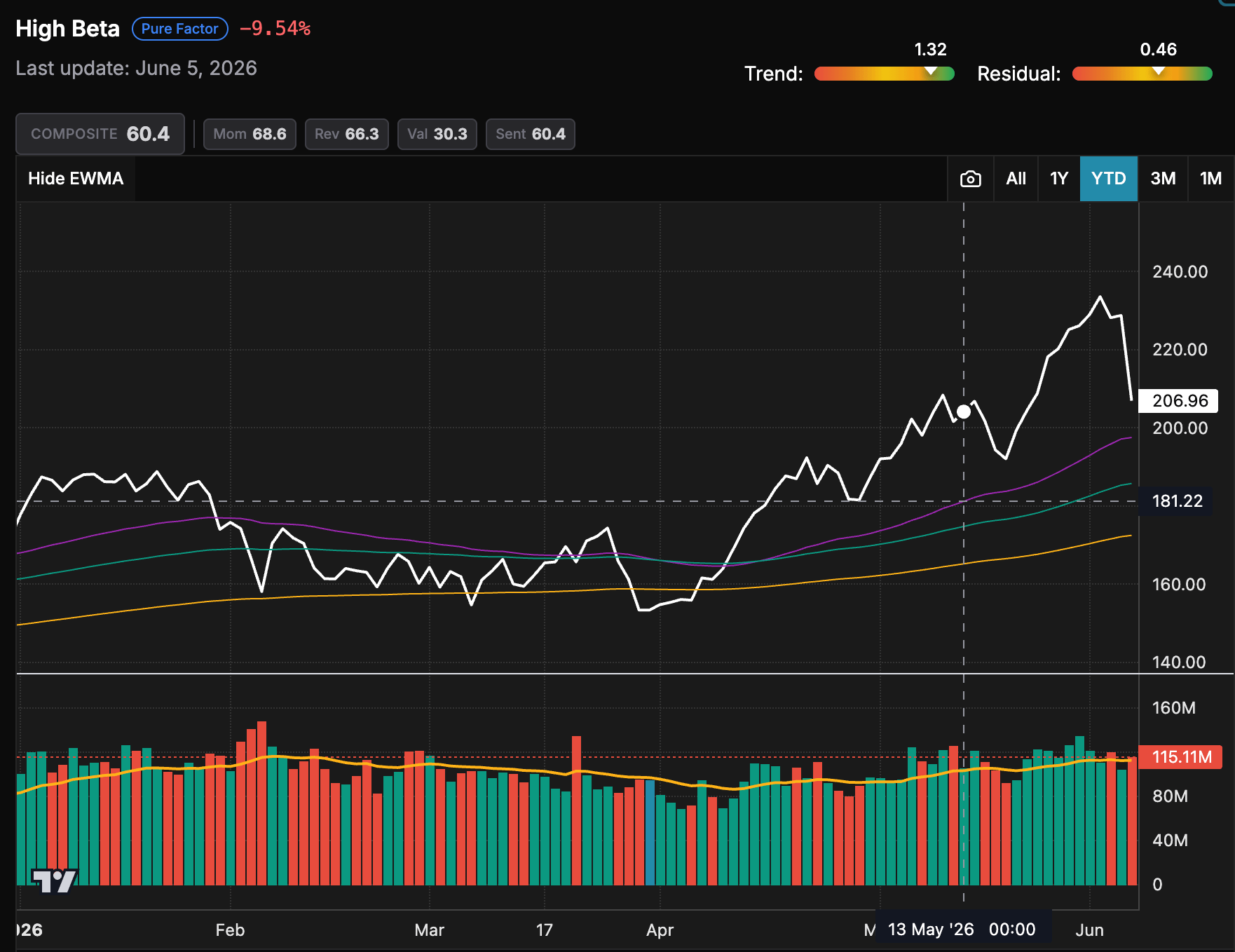

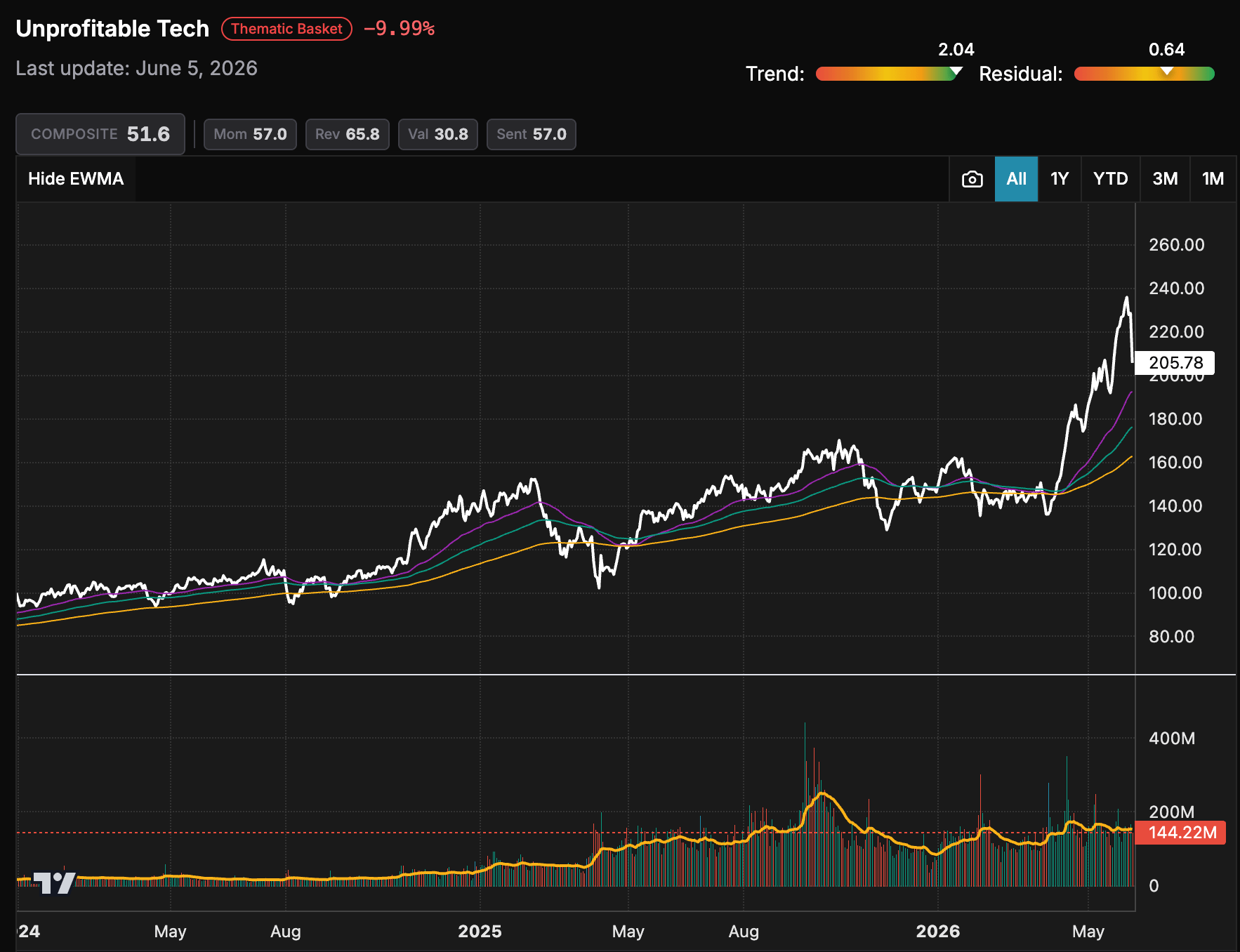

High Beta Took the Last Leg

After momentum peaked, the high beta factor managed to have one final aggressive leg higher.

When you think about high beta, think about animal spirits. This is where unprofitable tech, meme stocks, speculative growth, and the crappiest parts of the risk spectrum live in the long leg. The funding leg is usually low volatility, defensive, boring quality.

Momentum and high beta are related, but they are not the same animal.

Momentum was pushed by stocks with strong earnings revisions, AI capex exposure, semis, memory, Korea, and energy. These were often real businesses with real earnings momentum.

High beta does not care. High beta happily buys the junk if the correlation is high enough to the benchmark. It buys even more if the stocks volatility is high, Beta scales up with covariance. It is the factor expression of traders pushing their luck trying to find leverage to the market.

That matters because an extended high beta factor at all-time highs is rarely a sign of healthy risk appetite. It is a sign that traders are over their skis. They are no longer buying improving fundamentals. They are buying optionality, leverage, and the hope that someone else will mark the same trash higher tomorrow.

This was the first warning that the rally was losing quality.

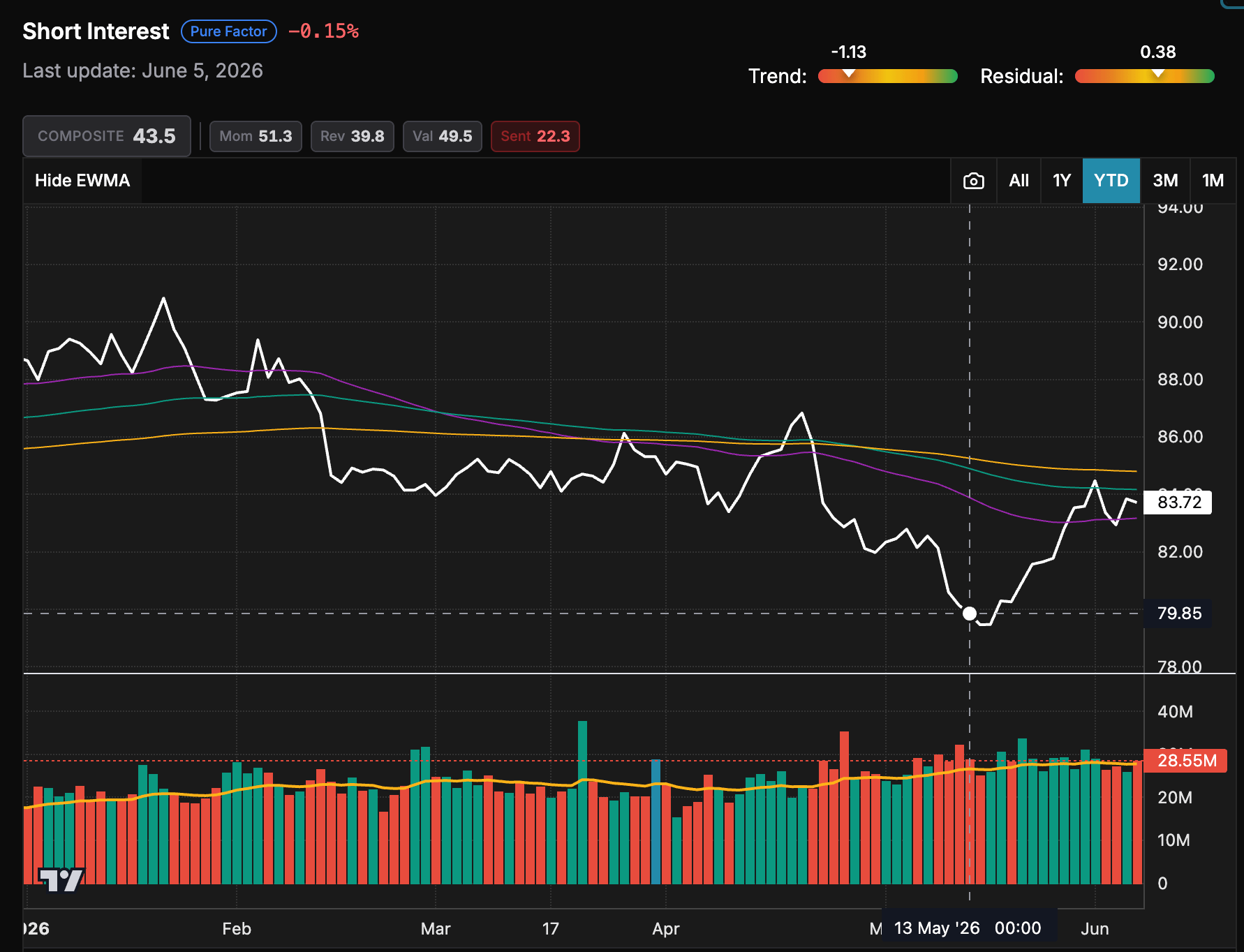

The Short-Covering Engine

The second force was even more important: the US long/short Short Interest factor.

This portfolio buys the most shorted stocks in the market and shorts the least shorted ones. Mechanically, it tends to capture the pain trade in crowded shorts.

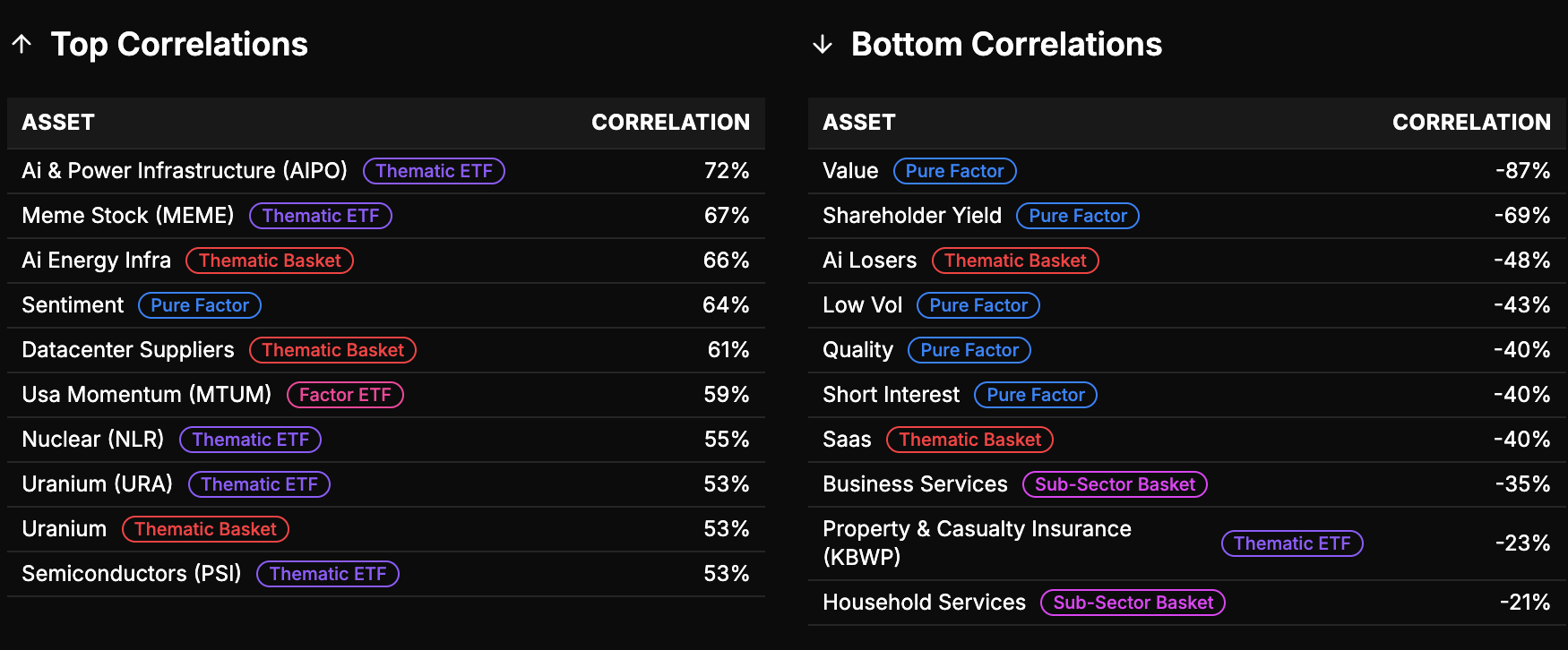

The composition was telling. The long side had been heavy in AI losers like software and consulting, while the short side was exposed to AI capex receivers such as semis, AI-linked utilities, and other winners of the capex cycle.

And lo and behold, the Short Interest factor bottomed around May 15, just a couple of days after Momentum peaked.

From there, it ripped.

Heavily shorted software names were aggressively covered for three weeks. What started as genuine positive earnings surprises in names like DDOG and SNOW turned into a broader rush into the most hated parts of the tape. Underweight traders and long/short funds had to chase. Shorts had to cover. The losers of the AI trade suddenly became the marginal source of index support.

This was the last key force that pushed the S&P 500 to new all-time highs.

It also pushed the dispersion trade to new extremes.

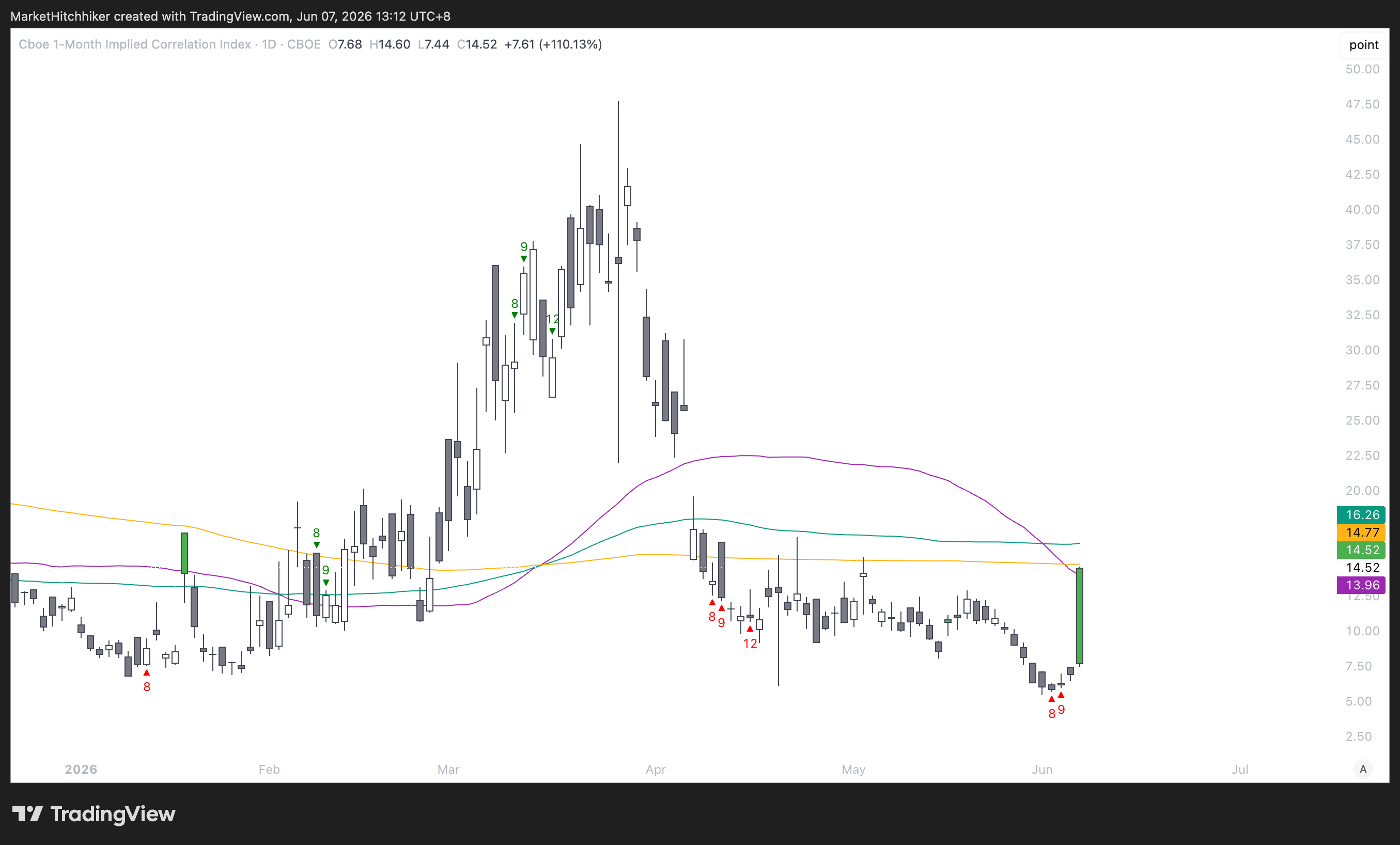

Peak Complacency in Correlation

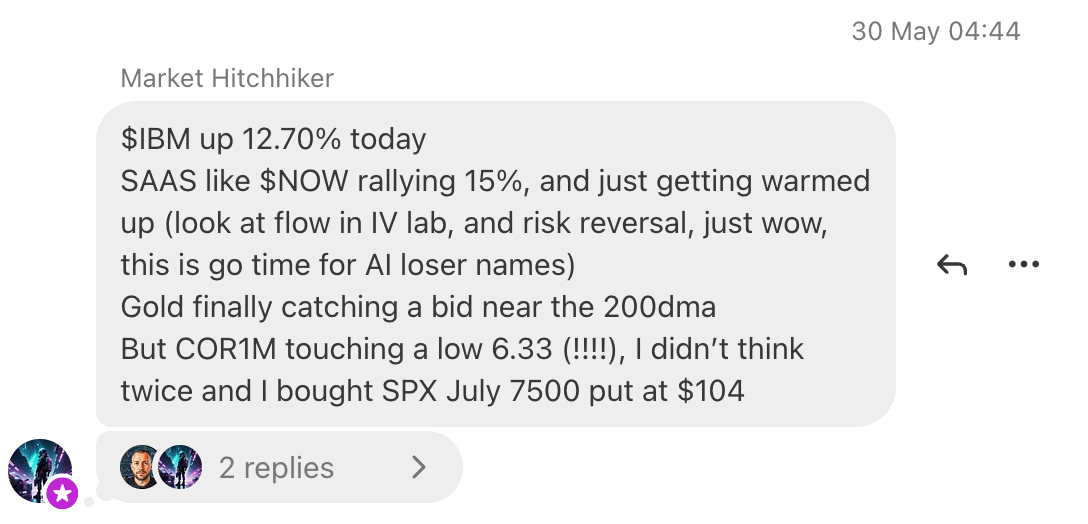

As the short-covering engine kicked in, implied correlation collapsed to absurd levels. COR1M, the CBOE 1-Month Implied Correlation Index, printed below 6 last Tuesday.

Sub-6 implied correlation is absurd. Mechanically, this meant the market was pricing a world where single-name volatility could remain high while the index stayed calm. Everyone wanted to own the dispersion trade. Everyone wanted to monetize index calm while trading fireworks underneath the surface.

When implied correlation gets this low, the index becomes fragile. A small catalyst can suddenly matter because the market is no longer positioned for stocks to move together. If enough crowded longs fall at the same time, index hedges have to be adjusted, dealers have to rebalance, and a supposedly diversified book starts behaving like one giant trade.

This was peak complacency and extreme bullish positioning.

The options market was saying the same thing.

Call volume exploded in the most crowded names: MU, SMH, SOXL, EWY, TQQQ, and all the usual suspects. And yes, because apparently buying calls on a 3x levered SOXX product is now considered a normal thing to do.

There were signs everywhere that the crowd was overweight the AI complex. Semis, memory, Korea, levered tech, call spreads, upside skew, low implied correlation. Different expressions, same trade.

The Candle That Broke the Spell

Last Friday, the S&P 500 fell 2.64%. The Nasdaq 100 dropped 4.77%.

We did not need much of a catalyst. A strong-ish jobs report was enough. That is usually what happens when a market is stretched this far. The catalyst is never the real story. The positioning is.

Charlie McElligott at Nomura described it perfectly as a market “collapsing under the weight of its own delta.”

That is exactly what it looked like.

When everyone is long the same upside, when everyone has monetized downside protection, when everyone assumes correlation stays dead, the first downside move forces the market to hedge after the fact. The move creates the need for more hedging, and the hedging creates more movement.

Then come the tweets, the memes, and the hilarious attempts to explain a multi-week positioning imbalance with one macro print.

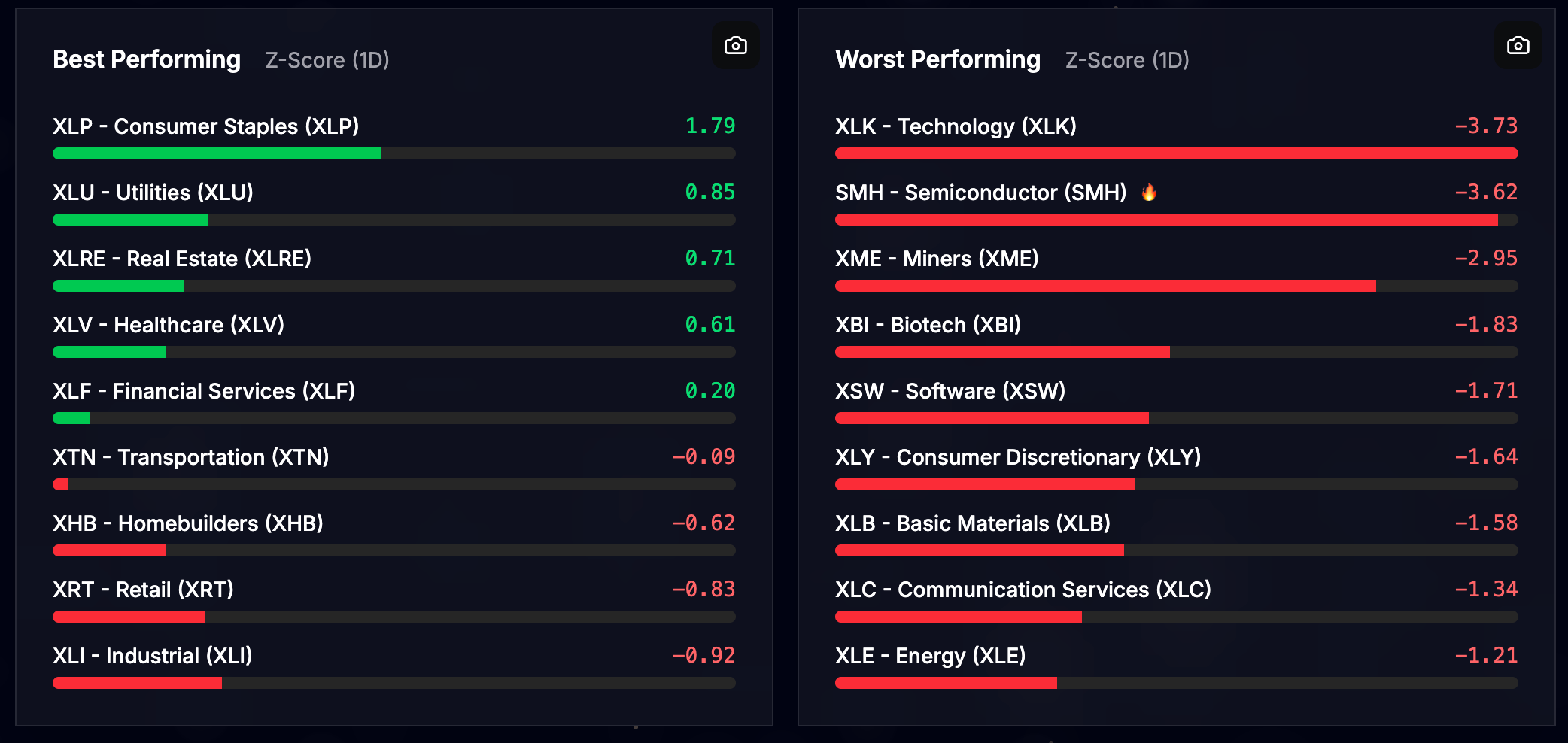

This was a textbook risk-off day.

Defensives were the only sectors that really weathered the storm. Most cross-assets traded lower. The one thing that did exactly what it always does during a classic risk-off impulse was the almighty US Dollar.

Factor land told the same story: RISK OFF.

Momentum, high beta, crowded longs, short interest, levered tech, AI complex. The unwind was broad enough to matter and concentrated enough to tell you exactly where the pain was.

The Froth Came Out Fast

The good news is that a lot of froth can disappear in a single day.

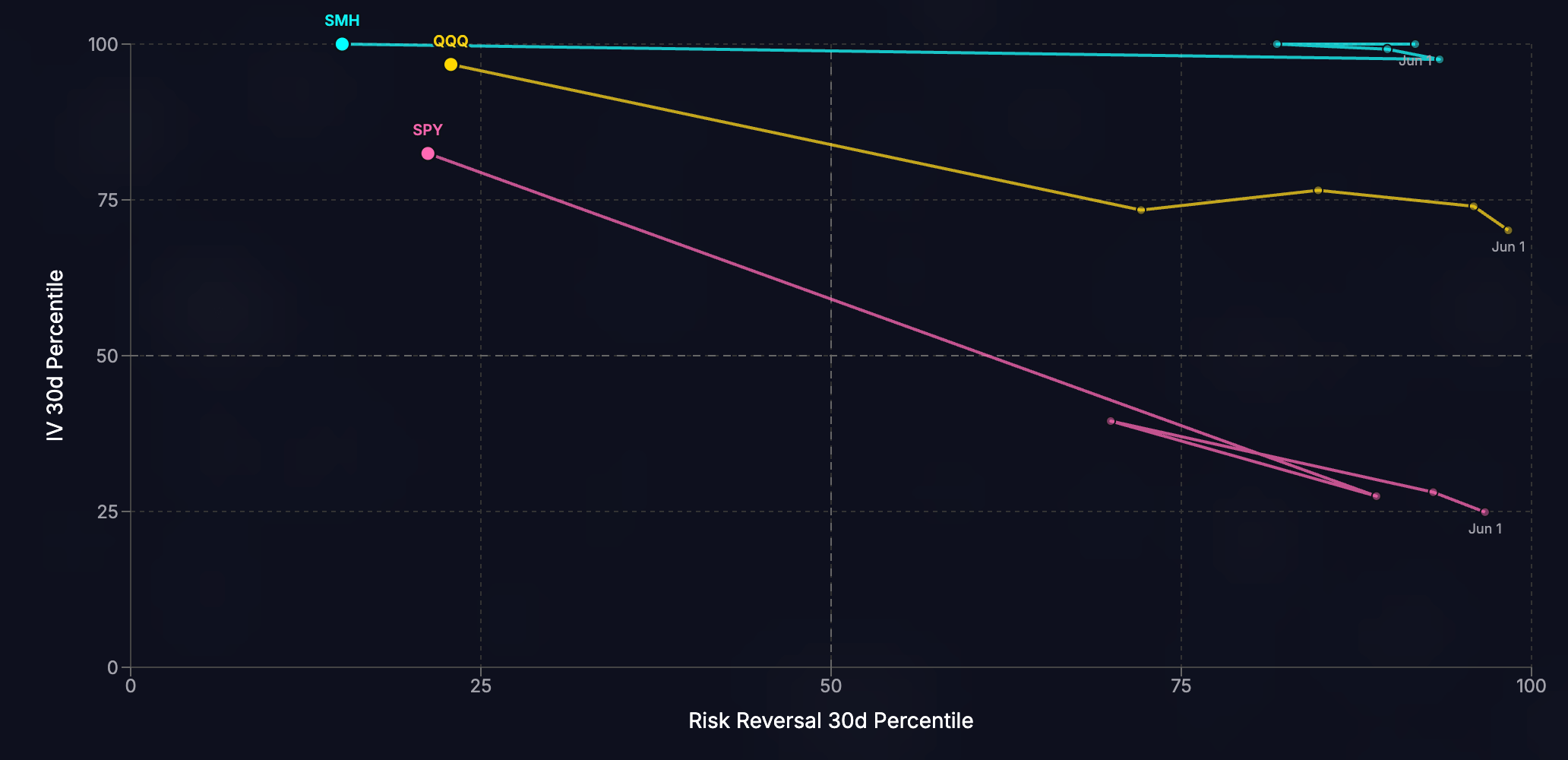

A few hours of trading and poof, the skew completely flipped for the major benchmarks.

How to read this chart:

X-axis: 30-day risk reversal, normalized with 1-year percentile rank. Risk reversal is the ratio of 25-delta calls over 25-delta puts.

Y-axis: 30-day at-the-money-forward implied volatility, normalized with 1-year percentile rank.

The move in implied parameters was violent. Traders went from paying for upside to scrambling for downside protection.

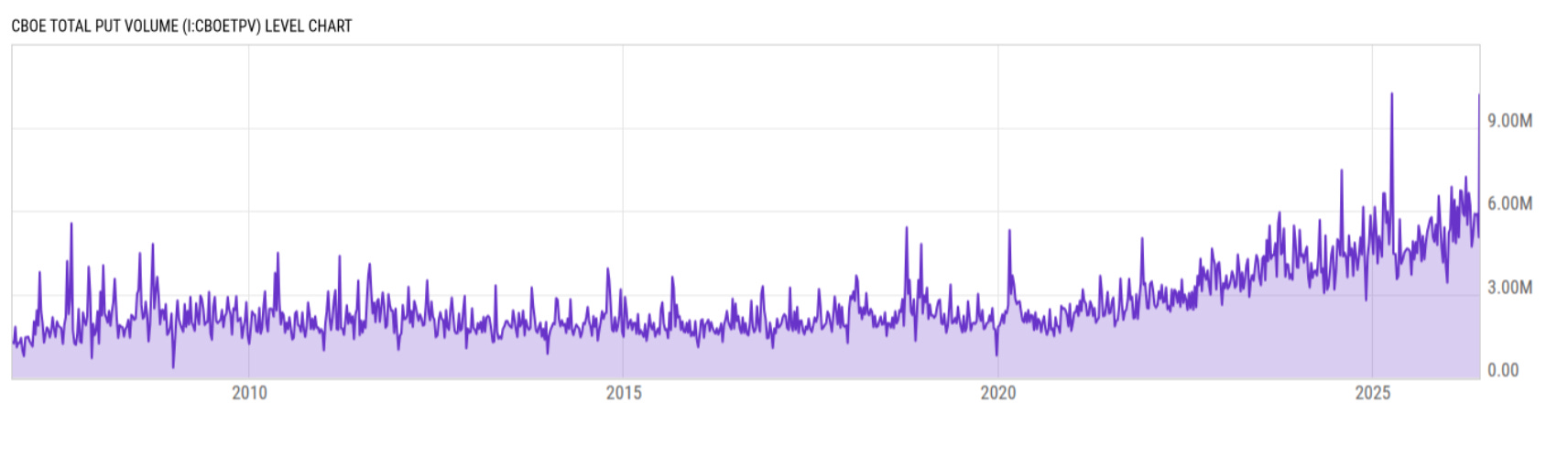

That flip did not happen on light volume. CBOE put volume exploded.

This is typical capitulation behavior: hedging too late into a large daily move. It is the oldest lesson in options trading and somehow everyone has to relearn it every cycle. Hedge when you can, not when you need to.

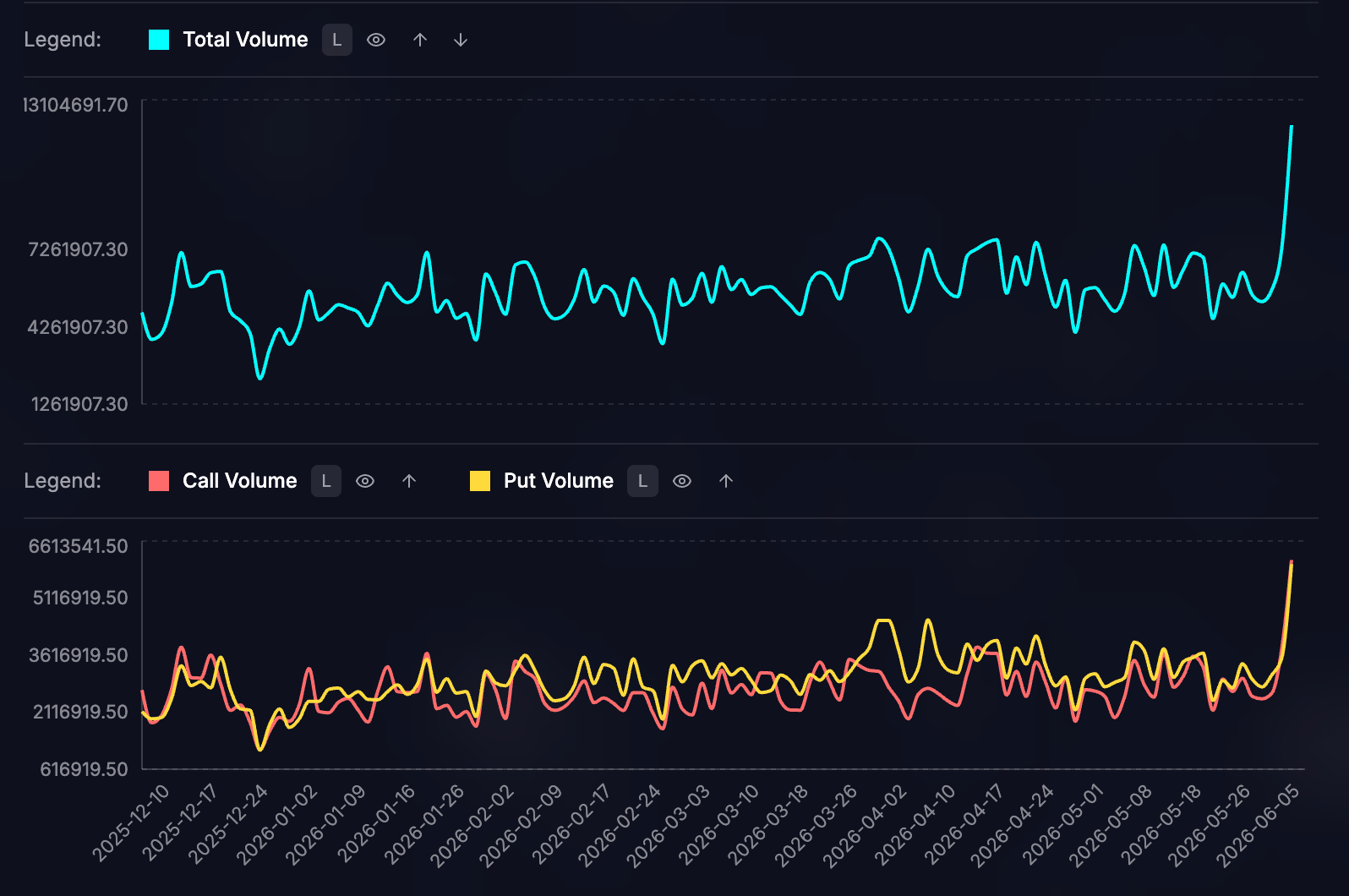

QQQ options told the same story.

Leveraged ETF volumes were spicy too. Inverse products such as SQQQ saw a massive spike in activity, another sign of short-term capitulation.

This is what a positioning reset looks like. The market spends weeks walking into a crowded room, then everyone discovers the exit door at the same time.

Credit Did Not Confirm

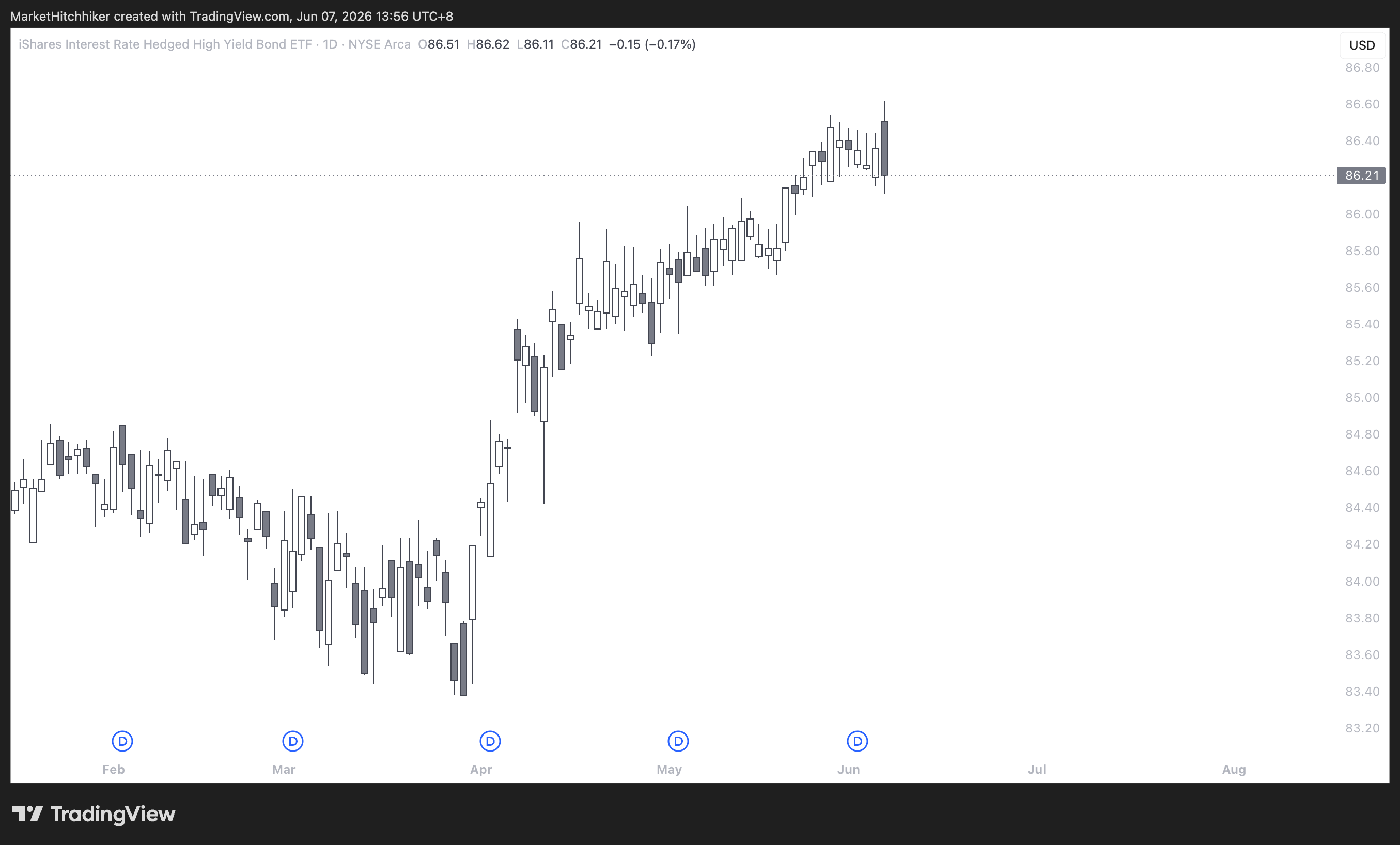

The most important cross-check came from credit. In high yield, HYGH, the high yield duration-hedged ETF, did not confirm the move in equities.

That matters. If credit had broken with equities, I would be much more worried. Credit is usually better at sniffing out genuine economic stress than equities during these flow-driven episodes. When equities puke and credit shrugs, the message is that the liquidation is probably self-contained inside equity positioning rather than the start of a broader funding problem.

That does not mean equities cannot go lower. They can. Positioning moves can overshoot violently. But it does mean this does not yet look like a systemic credit event.

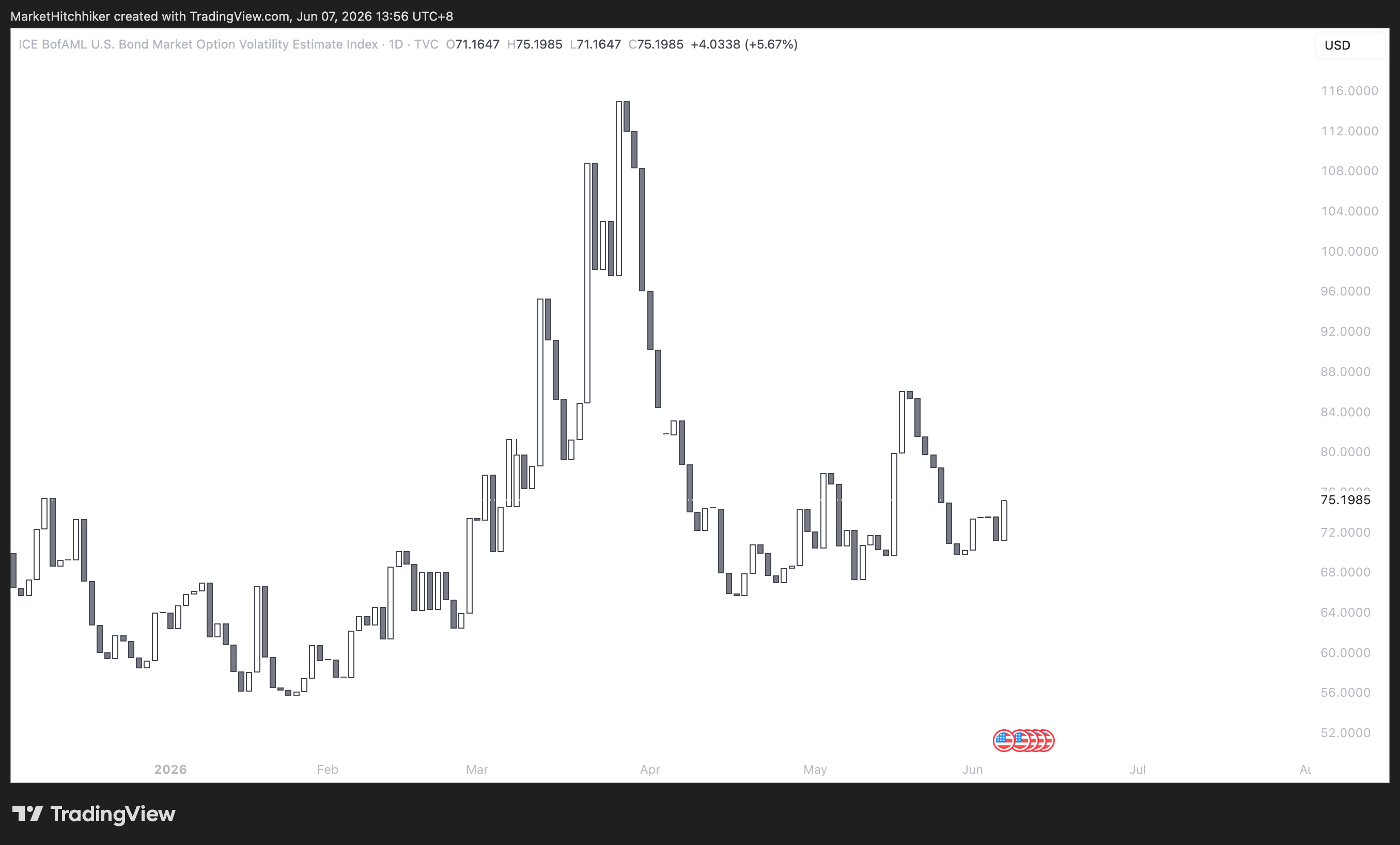

Bonds are giving a similar message. Despite the supposedly hot jobs report, bonds did not sell off as much as expected. The MOVE Index, the implied volatility index for bonds, remains extremely well behaved.

If this were a true macro regime break driven by rates, bonds and bond volatility would be screaming. They are not.

That is why I frame Friday as a positioning reset first, not a macro panic.

Dip or Something More Sinister?

The obvious question now is whether this is just a dip in the current bull market or the beginning of something more sinister.

My answer is that, for now, this looks like a classic positioning reset.

The evidence:

Credit did not confirm the equity puke. HYGH was resilient.

Bonds did not panic. MOVE remains well behaved.

Options showed capitulation. Put volume exploded after the move, not before it.

Skew flipped aggressively. Traders rushed from upside greed to downside fear in a single session.

Leveraged inverse ETF volume spiked. This is usually a short-term capitulation tell.

The pain was concentrated where positioning was most crowded. AI complex, momentum, high beta, short-covering winners.

That is the profile of a self-contained equity liquidation.

The near-term path is still messy. I would not be surprised to see Monday pre-market trade somewhat bearish. Asia traders may have to puke positions at the open, and there could be margin calls around the edges. That kind of follow-through would not shock me.

If that happens, it could create a good buying opportunity in the US pre-market.

The key is to distinguish between forced selling and a true deterioration in macro conditions. Forced selling creates bad prints and good entries. Macro deterioration creates bad prints and bad entries.

Right now, the evidence points more toward the first.

Great post! Really love learning how to use your tool to look under the hood of the market.