Some thoughts about the market

Momentum is being pushed way too far.

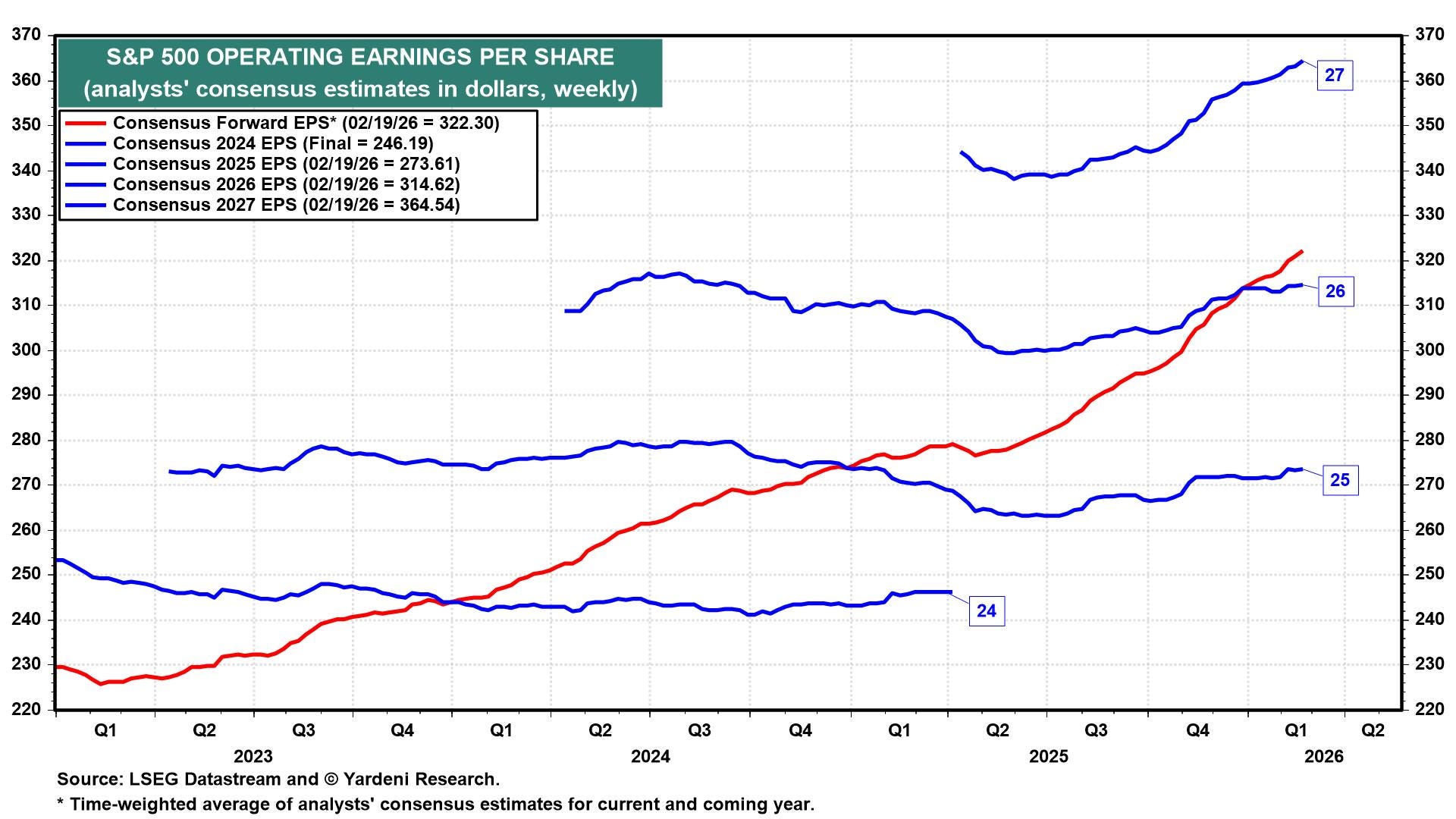

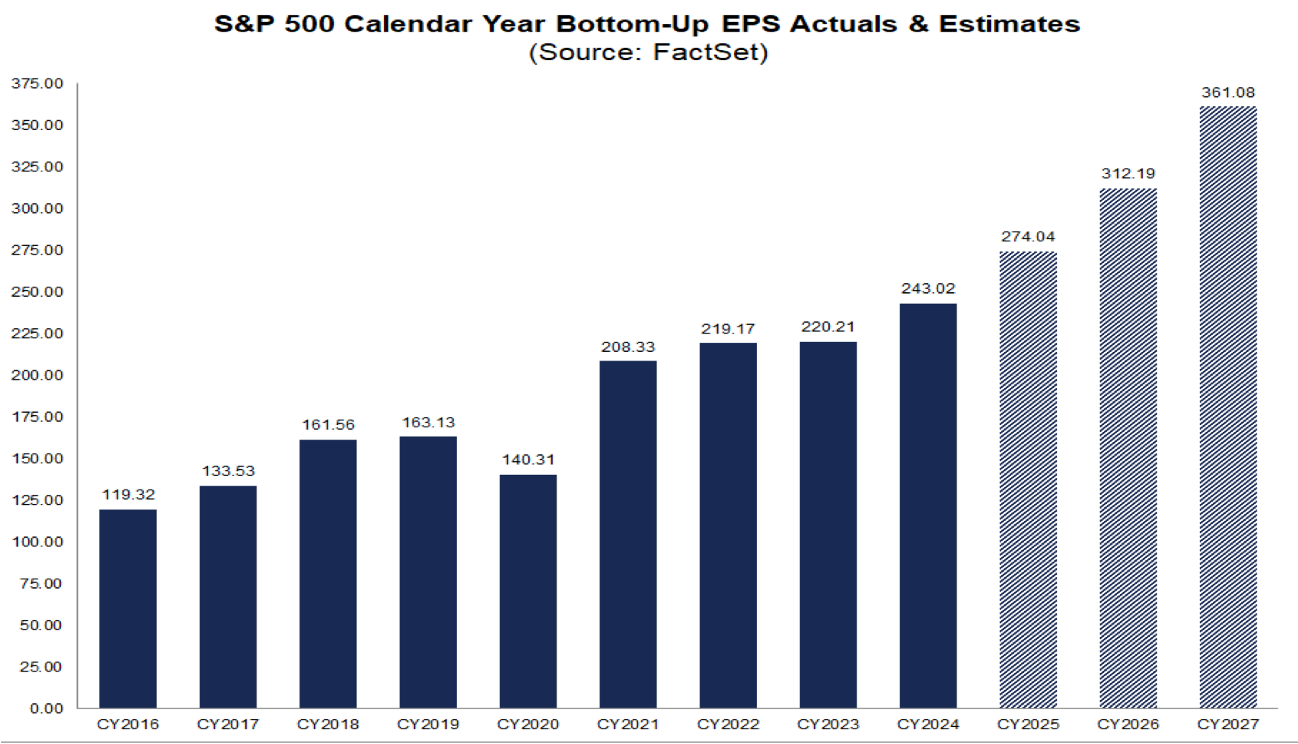

S&P 500 Forward Earnings? Growing at a record pace

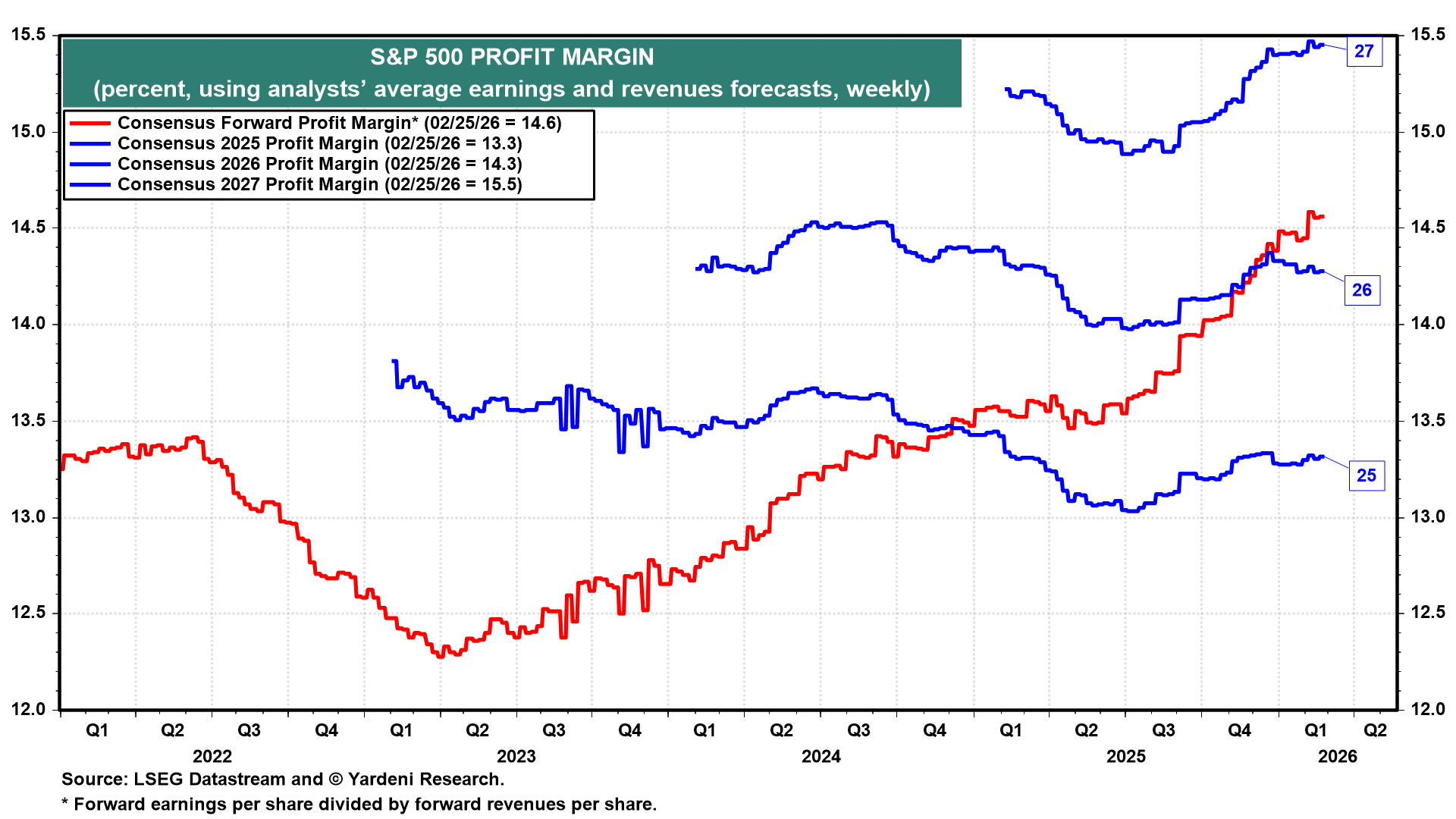

Forward Profit Margins? Growing as well

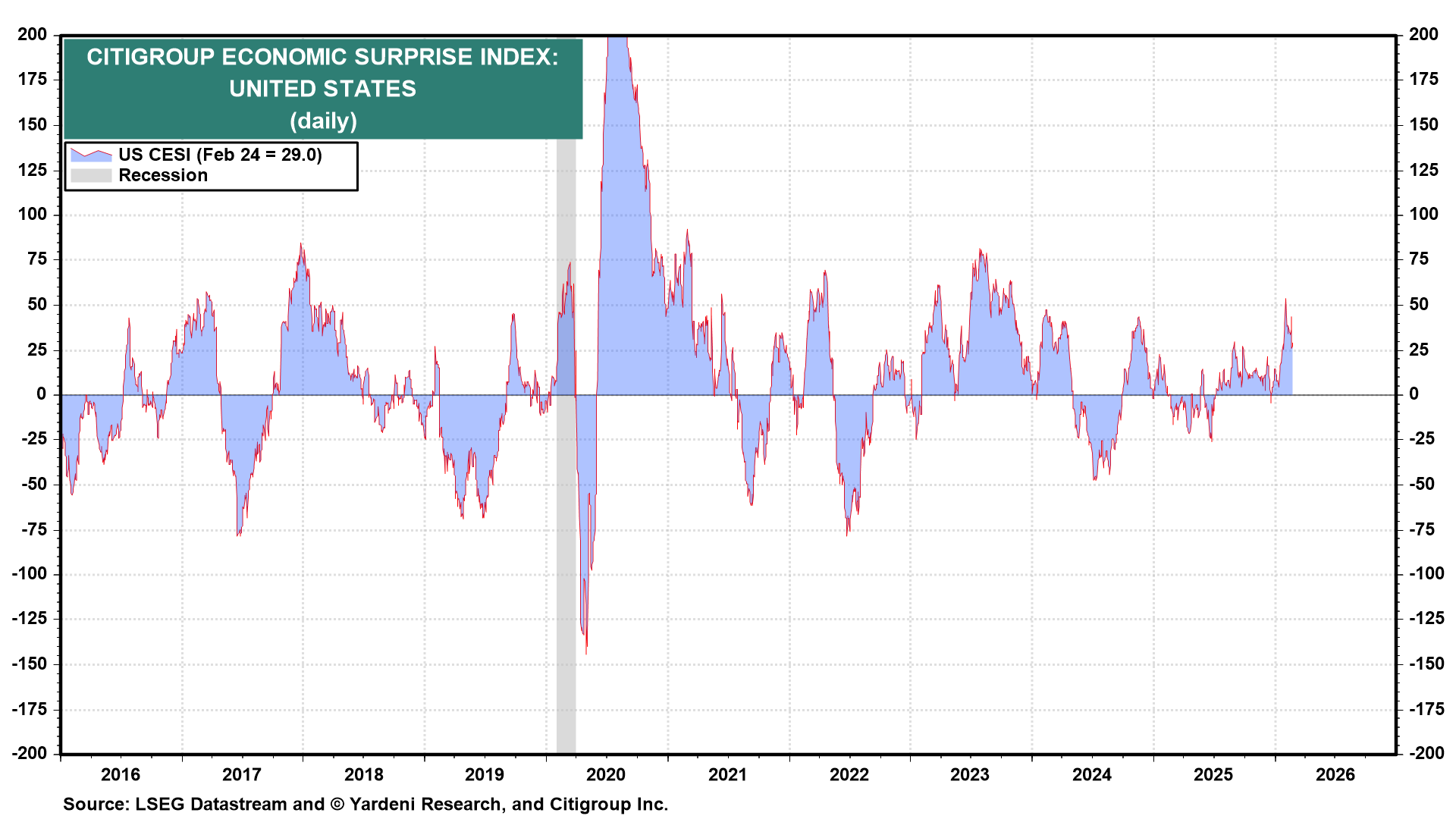

Citi Economic Surprise Index? In positive territory

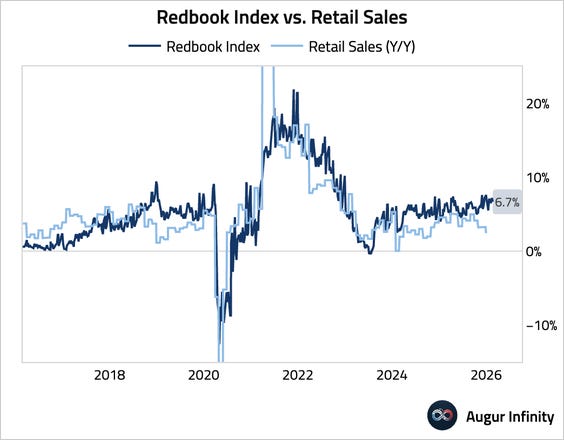

US Consumer? Doing fine

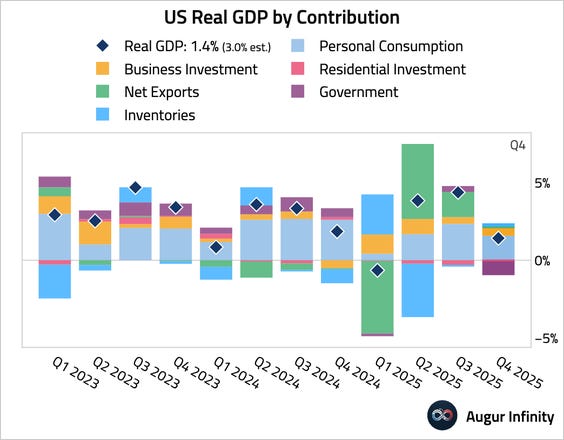

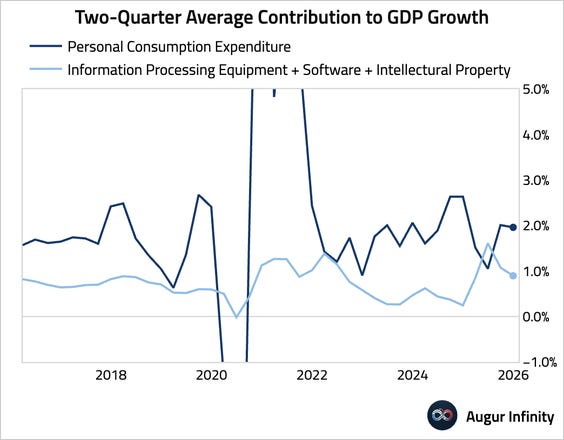

Q4-2025 GDP? Still mainly driven by Personal Consumption

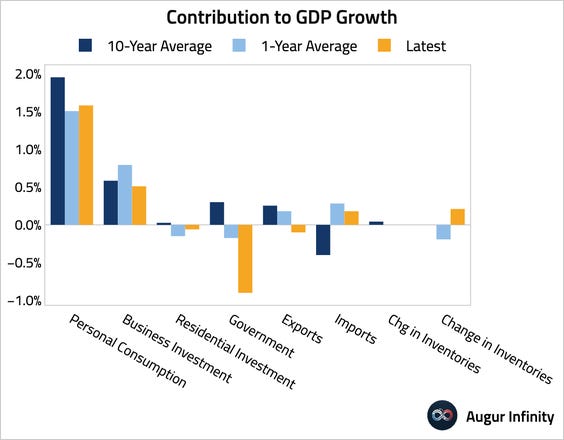

Personal Consumption and Business Investment are near the 10-year average

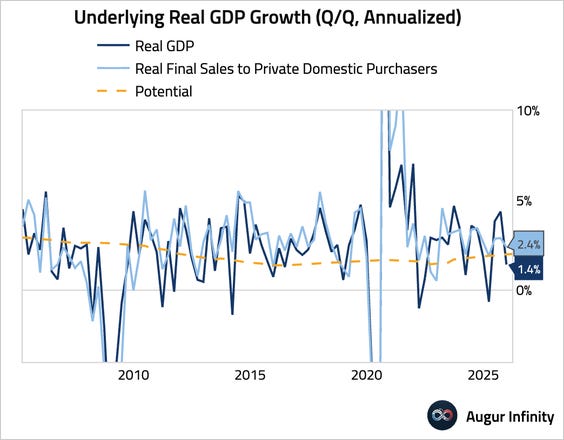

Removing all the noise from net exports, inventories, and government spending, real final sales to private domestic purchasers still saw robust expansion.

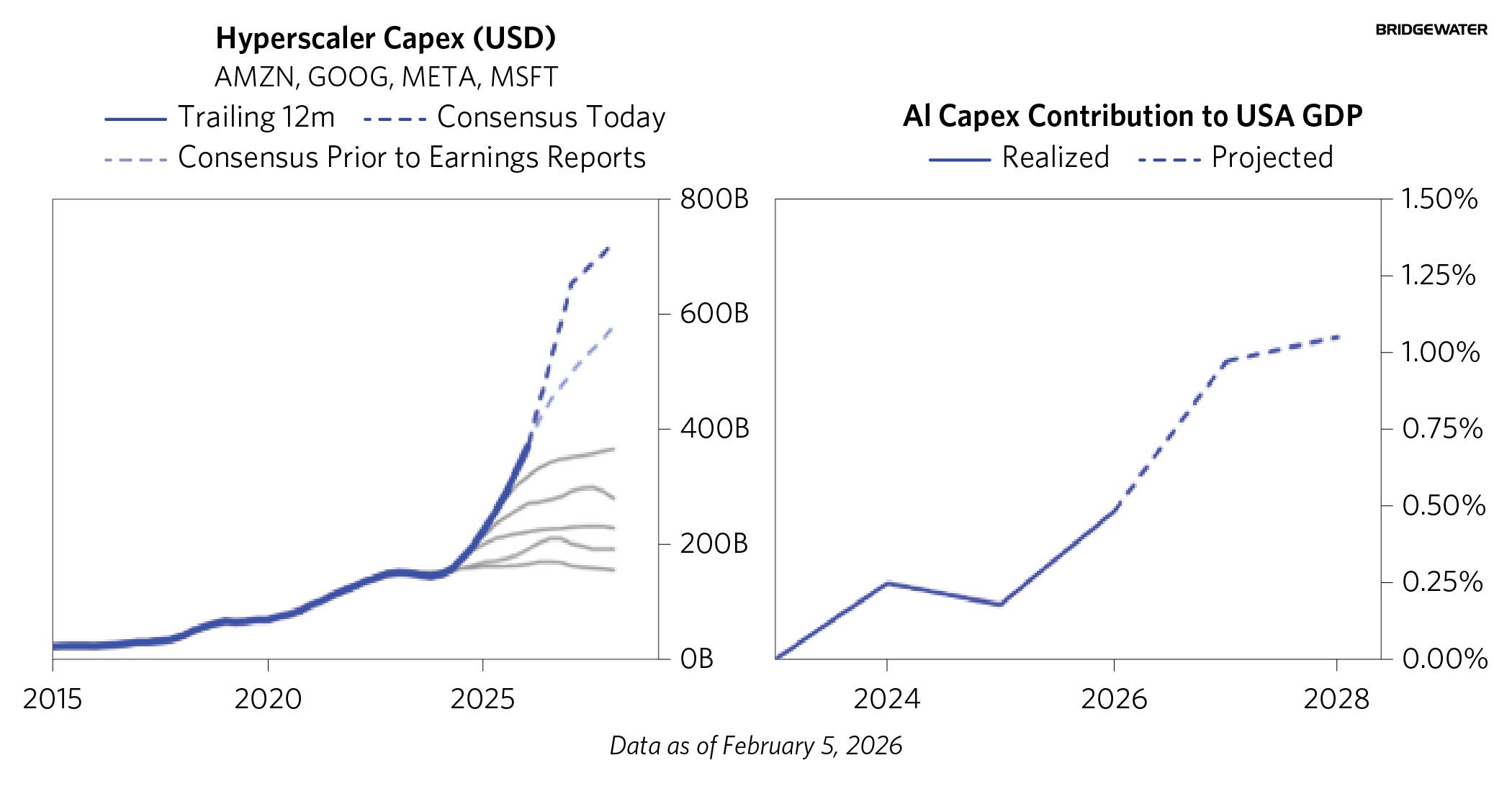

The US economy is pushing higher with or without the AI spending.

According to Bridgewater, AI Capex is estimated to keep growing until 2028, adding up to 1% to GDP.

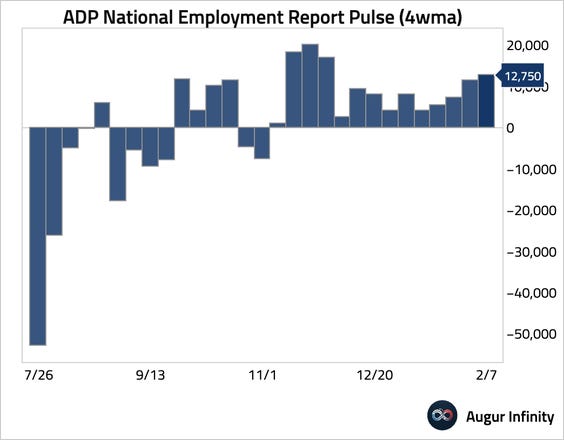

Job Market? Weekly ADP number is strong.

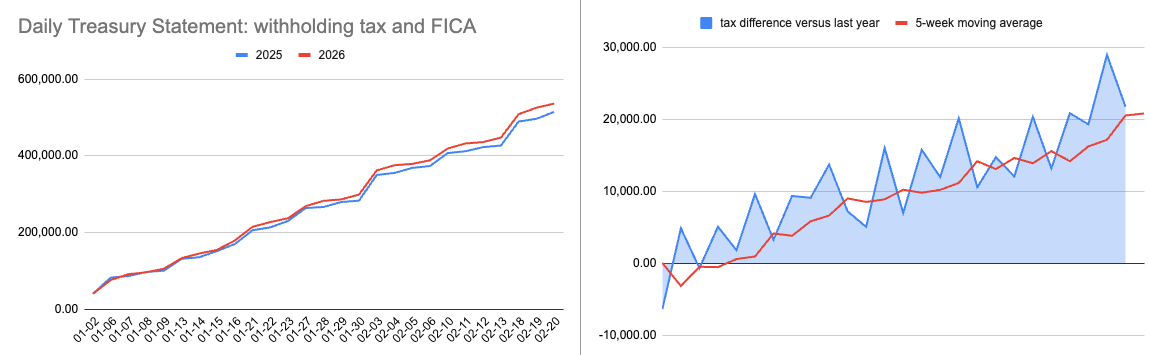

Withholding tax for 2026 is outpacing 2025. Reminder: this is the hardest data we have regarding the health of the job market. AI might be disrupting some industries, but on aggregate the US economy is still adding jobs.

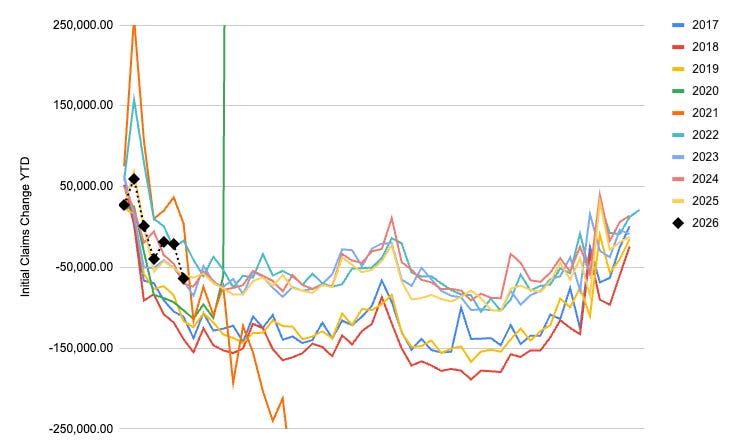

Same picture for Initial Claims; the NSA time series is tracking past years’ impulses.

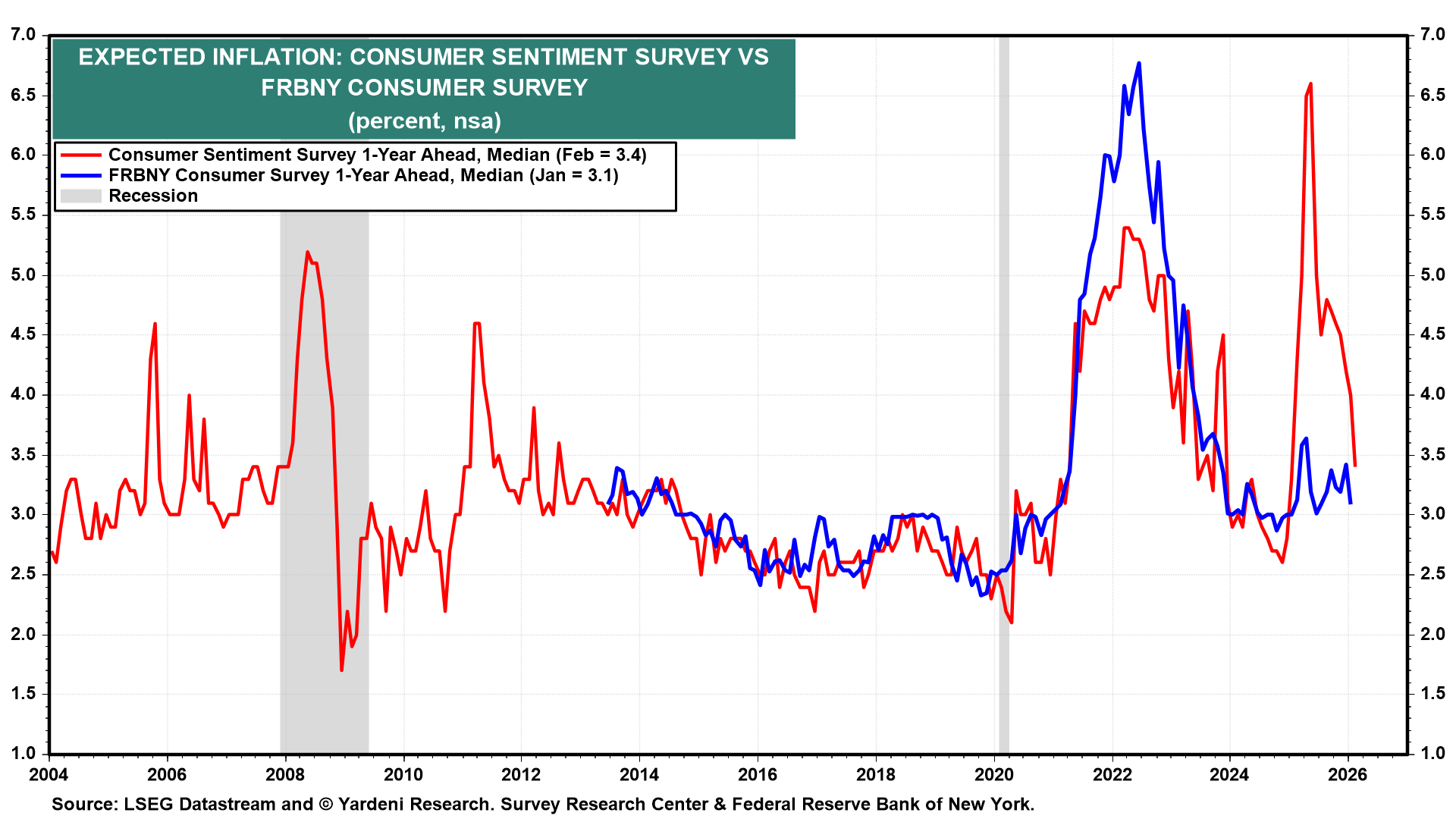

Inflation? Expectations have fully retraced the tariffs fear.

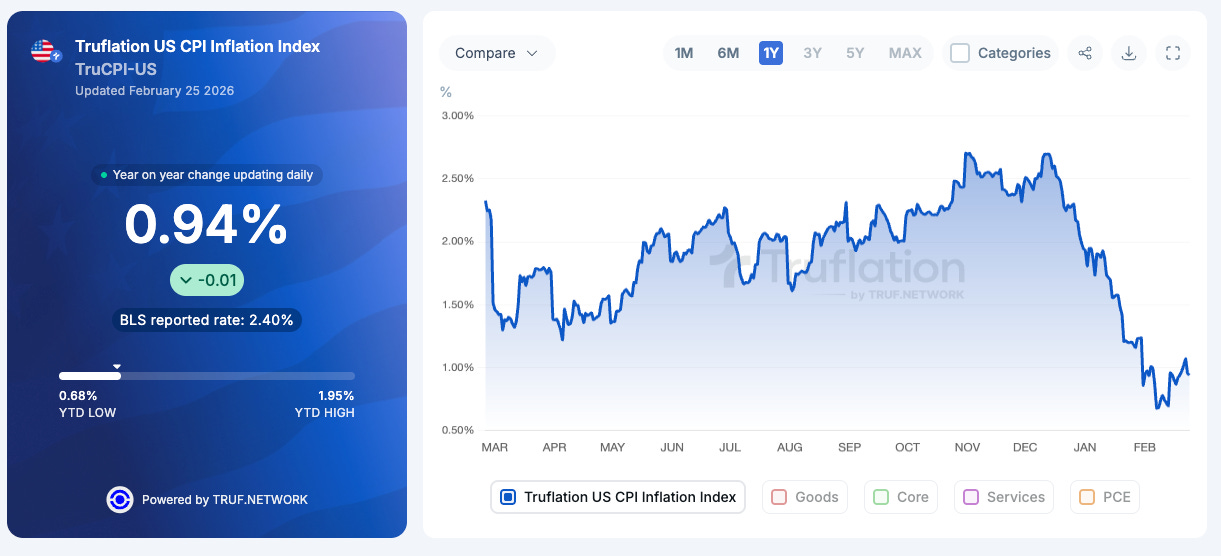

Truflation below 1%:

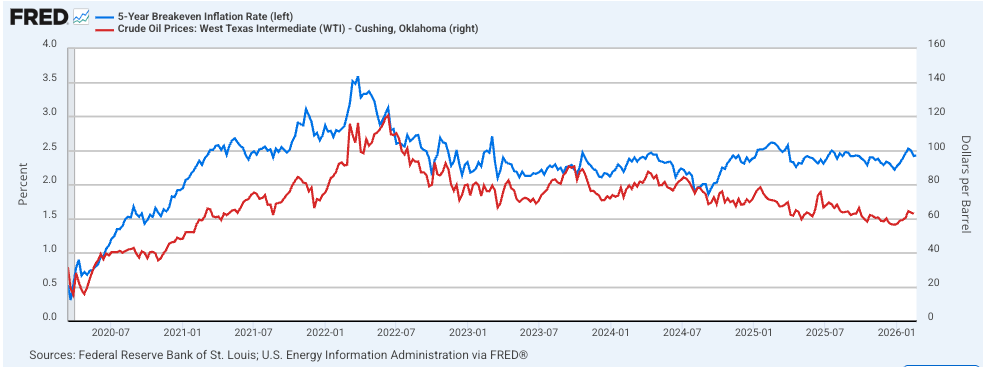

Inflation swaps and crude oil prices remain well behaved.

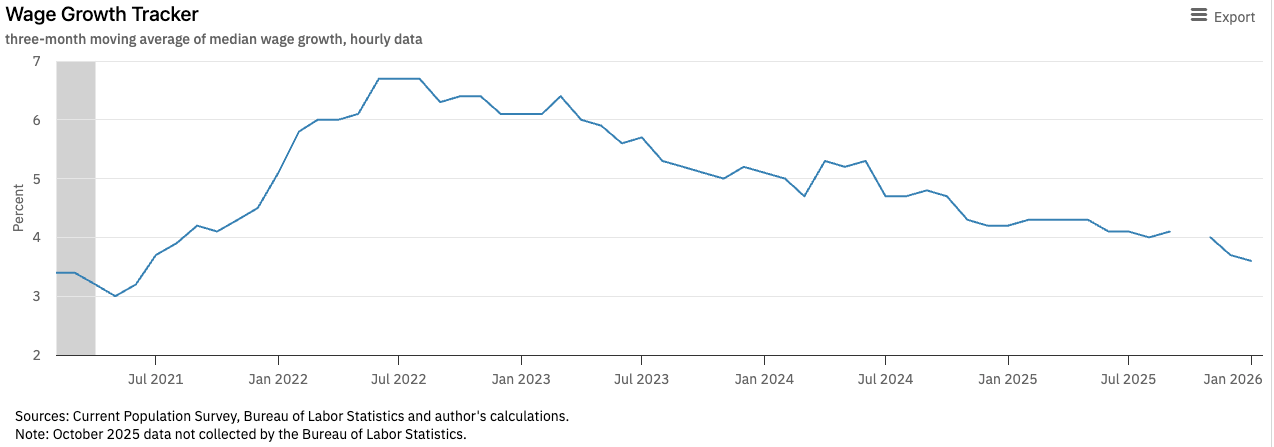

Wages? Still slowing down

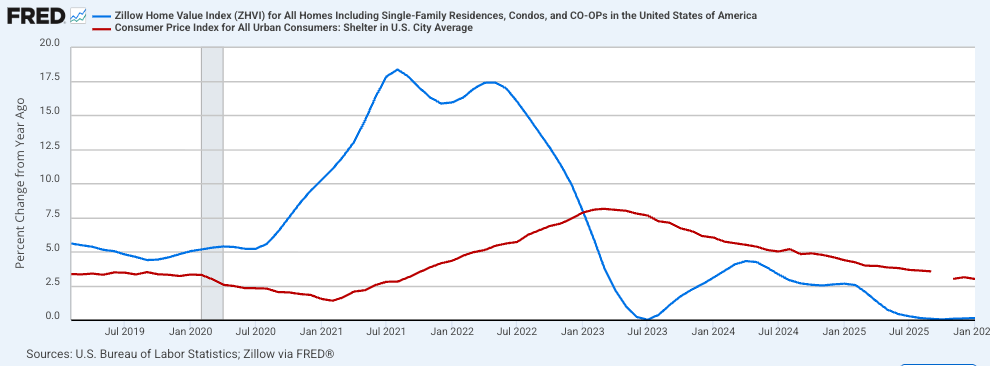

Rent and shelter? Same

Let me summarize the macro picture:

Growth is strong and potentially reaccelerating, sustained by both consumption and AI Capex spending.

Forward margins and earnings are growing at a record pace.

US job market is still at equilibrium with no sign of deterioration. AI could be impacting some industries; this is very well possible, but on aggregate we don’t see any worrisome slowdown.

Inflation is tame, with rent and wage increases still slowing down. Crude oil at $66 a barrel will not move the needle, especially when a lot of the recent price appreciation is 100% geopolitical risk premium.

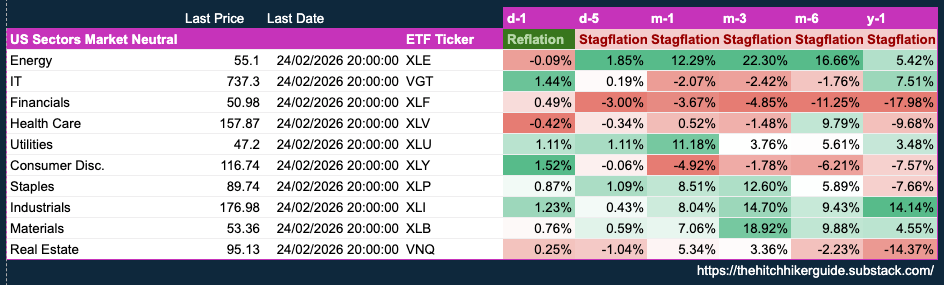

It all sounds very Goldilocks to me… yet the market has been throwing a fit for the past three months, with the S&P stubbornly flat while equity sectors are pricing a stagflation environment.

Energy: +22.30% over the past three months

Staples: +12.60%

Tech: -1.76%

Financials: -4.85%

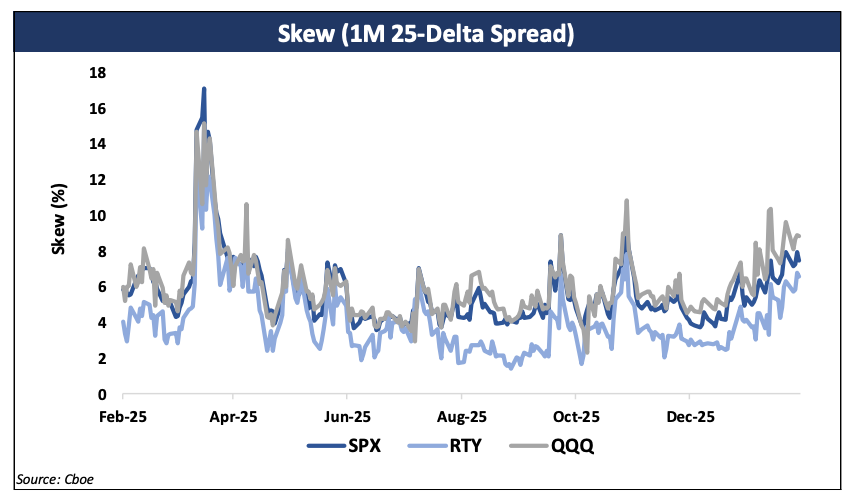

This is a very risk-off mix, and it transpires through the S&P 500 skew, trading at a very high level:

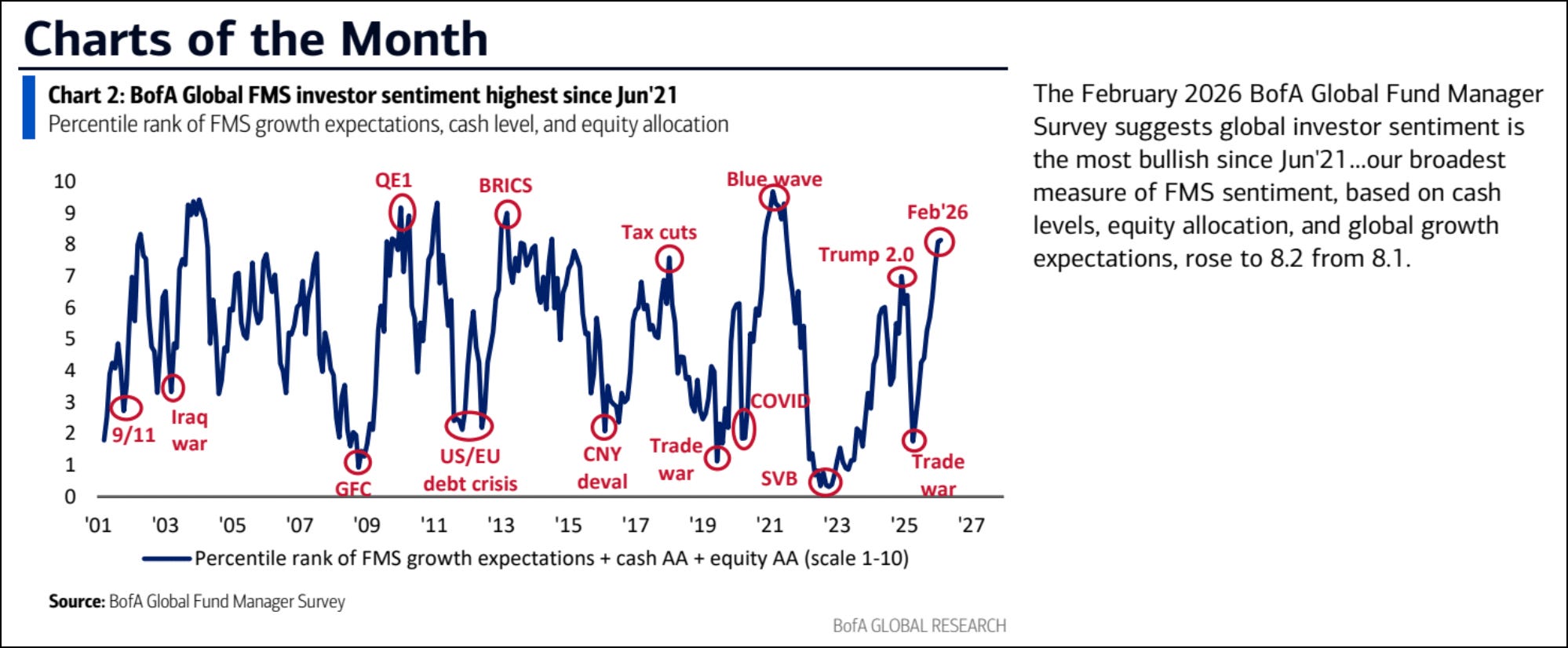

In plain English, traders have been hoarding OTM puts fearing a total collapse in the market. Interestingly, this is happening while investors are very bullish:

Very bullish but also very hedged.

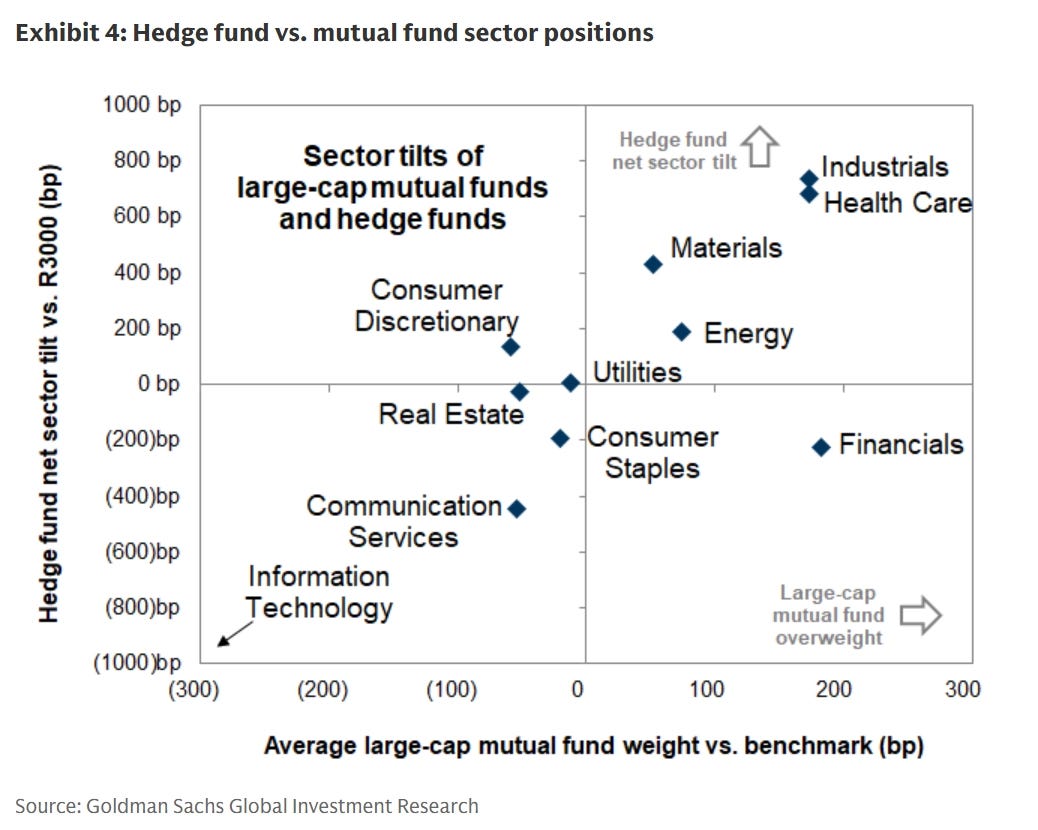

In terms of sector overweight, we are seeing both hedge funds and mutual funds overweight Industrials, Materials, Energy, and Health Care.

Industrials, Materials, and Energy make sense as they are expecting a “Boom.” They see the same macro data as us, and they extrapolate.

And by extrapolating, you end up trading momentum. US factor momentum is on an absolute tear; this is the best-performing factor YTD by a wide margin.

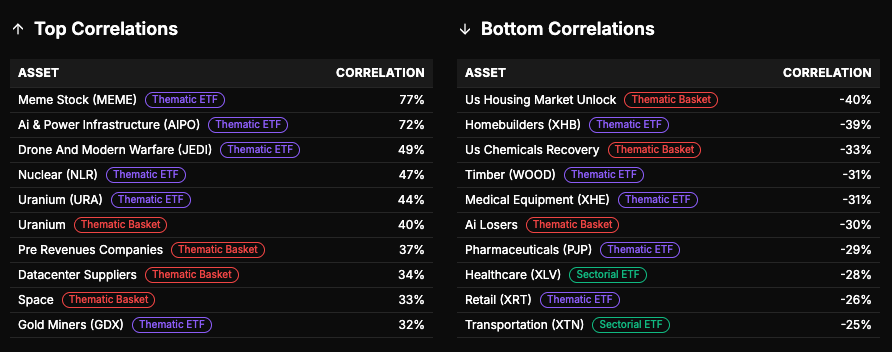

Momentum is currently correlated to four big themes:

US retail traders’ favorite stocks (aka meme stocks), high vol, high growth, preferably negative earnings. This theme has not been in favor this year; it is not driving the momentum factor performance.

AI and power infrastructure

Defense

Precious metals and miners

At the bottom correlation, we find AI losers.

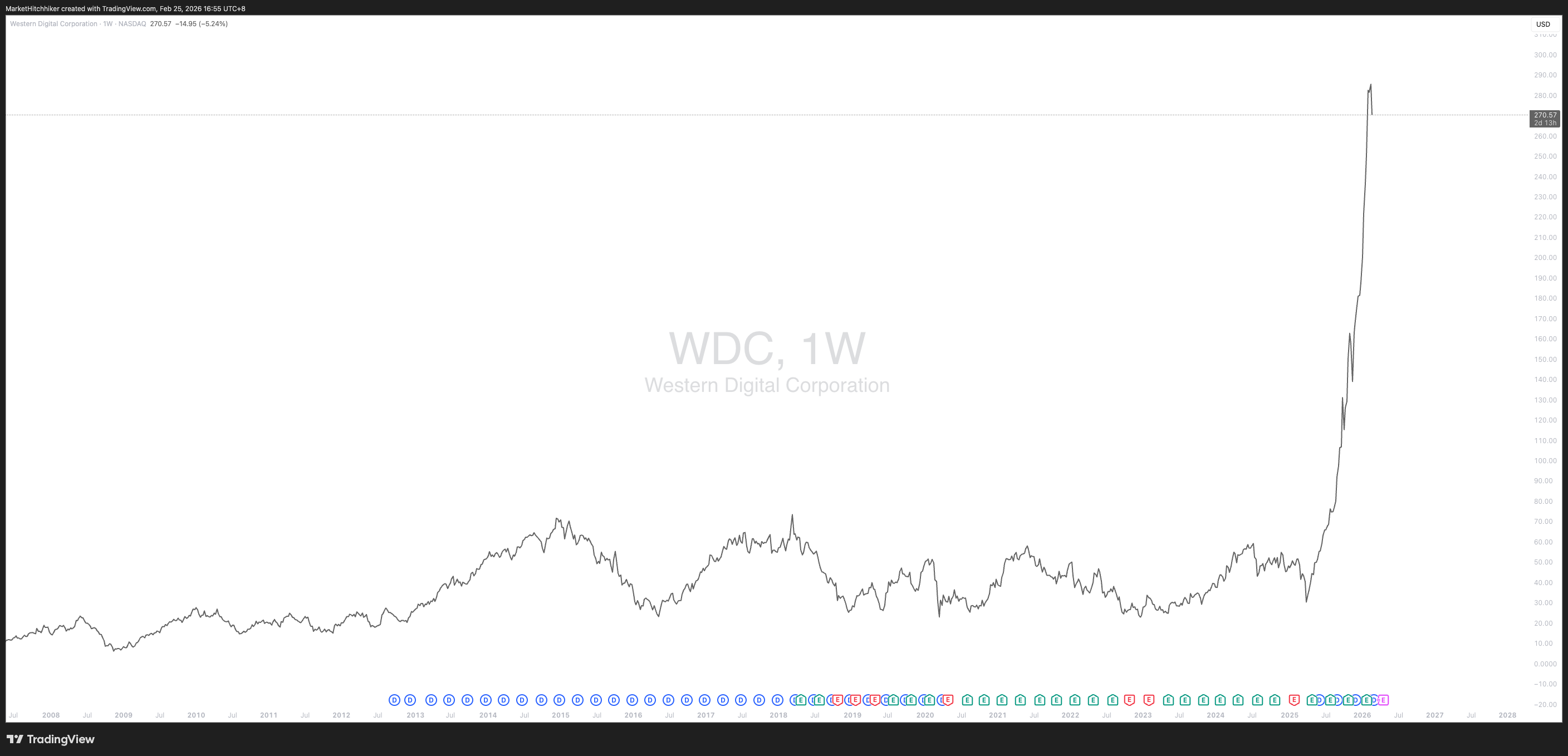

A few charts to illustrate how stretched these themes are:

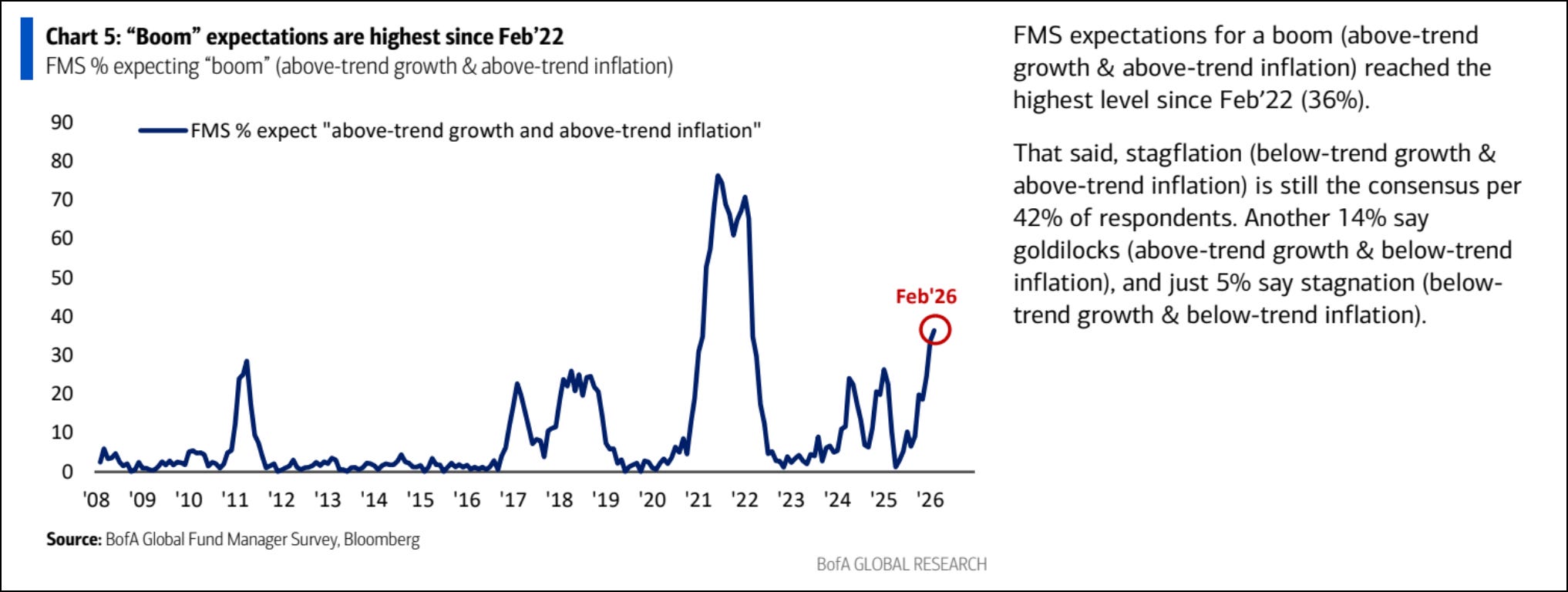

The “Boom” is here; it’s happening. And it also looks like we are near a blow-off top, typical of commodity boom/bust cycles. These moves are not sustainable.

Interestingly, this boom is happening at the same time as defensive names are ripping. Health Care, Staples, and Utilities are outperforming cyclical sectors like Consumer Discretionary and Financials

A “Boom” amid a risk-off move. Quite the unicorn we have there. It explains the very high dispersion we are seeing in the market.

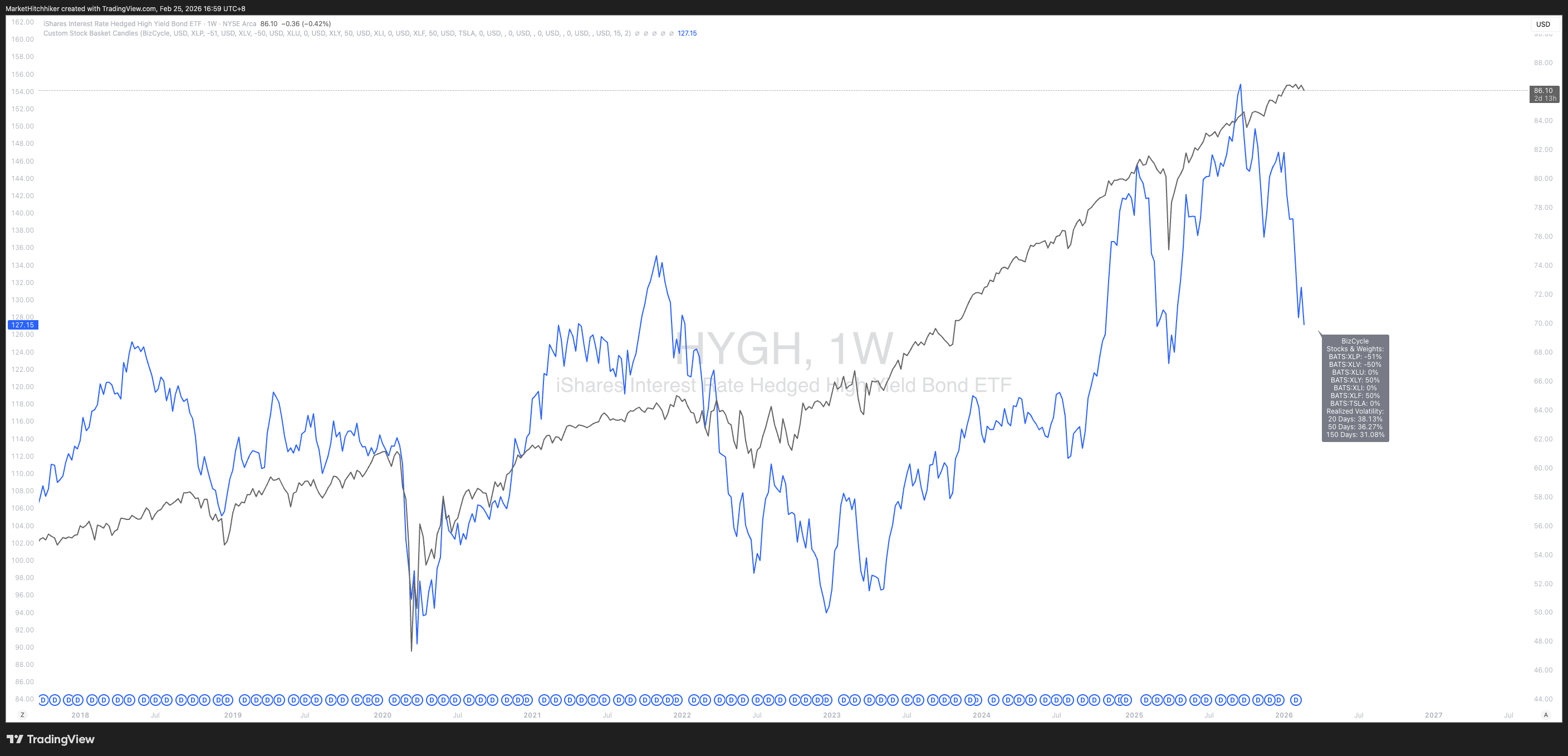

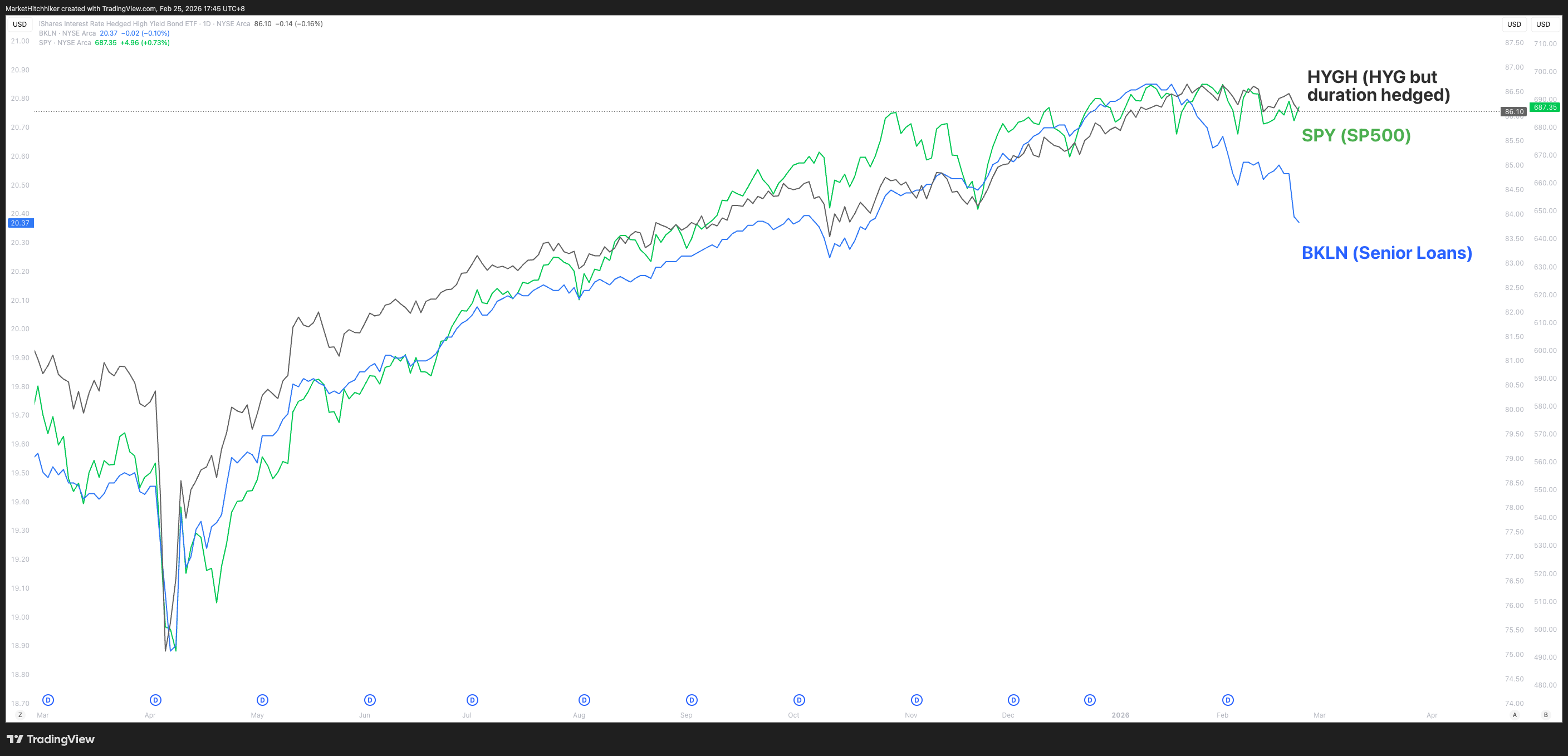

I have been saying time and time again that the S&P 500 is simply a high-yield bond. An overlay of HYGH and SPY shows a perfect correlation; they are tied at the hip.

BKLN is a senior loan ETF; these are short-duration loans made to large private companies like X. It usually follows HYGH with lower volatility. The recent AI scare has been bleeding into the senior loan market. This is extremely rare to see such divergence between BKLN and HYGH. While I am still constructive regarding US equities, this divergence is giving me pause. A very bearish scenario would be to see a contagion from this AI scare into the high-yield credit world, and inevitably it would spill into US equities, dragging the entire market lower.

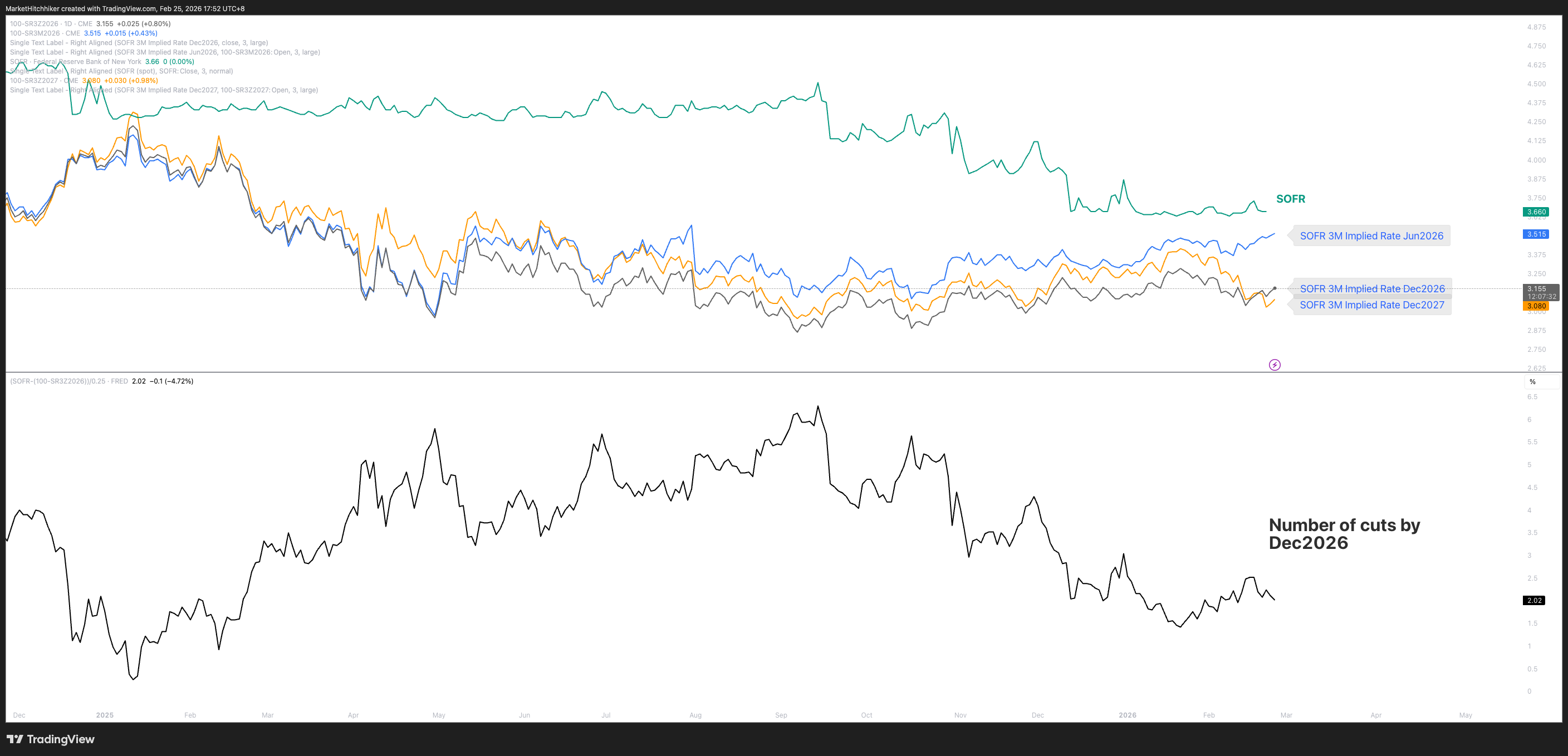

I am not yet worried; the Citrini doom post smelled like peak AI fear to me. And we are not seeing any more cuts being added in the SOFR market.

Summary:

Macro is still supportive of a Goldilocks environment.

Momentum is being pushed very far into big macro themes linked to AI Capex: energy, nuclear, memory, semis vs. SaaS, precious metals, miners, etc. This reminds me of a boom/bust cycle typical in commodities; we might be near the top of the cycle.

This extreme in momentum paired with peak AI fear is also pushing risk-off trades, with staples and utilities outperforming consumer discretionary and financials.

Senior loans are inflecting lower as the SaaSpocalypse is questioning the creditworthiness of some private companies…

…but public high-yield debt is holding up well.

Watch for any sign of spillover into high yield (HYGH ETF or IBOXX futures). Until then, the consolidation in the US stock market should resolve into a breakout (not a breakdown)…

…But we need tech stocks to lead again, as the broadening-out theme will not carry the market long enough, especially if the crowded trades linked to the AI Capex receivers enter into a blow-off top phase.

Finally, there are plenty of high-quality stocks currently trading at fair prices (Mastercard, American Express, IBM, MSFT, Uber, etc.). Consider buying them instead of buying SaaS stocks, which will probably stay in limbo for a long time. Do not confound multiple compression (or rerating) with indiscriminate selling. You want to buy what has been indiscriminately sold, but you stay away from an industry being rerated lower.