Your Margin Is My Opportunity

Why I am staying away from the AI capex receivers, slowly turning constructive on hyperscalers, and parking my beta in Apple.

I have been thinking a lot about the AI capex cycle lately. Who is writing the checks, who is cashing them, who is creating the demand, and most importantly, who gets to keep their fat margins when the music slows down.

Because the music will slow down. Capex level itself will remain high, but the rate of change is about to roll over. Markets do not care about levels. They care about second derivatives. And the second derivative on hyperscaler capex is about to flip.

This post lays out how I am positioning around that.

The Four Actors of the AI Capex Cycle

Before getting into the trade, a quick refresher. The AI capex cycle has four distinct categories of players. They get lumped together into the same “AI trade” bucket, which is a mistake.

Demand creators, the AI labs. Anthropic, OpenAI, xAI and a few others. They sit in their own category. They build the frontier models that drive the insatiable need for compute, but most of them do not do the heavy direct capex themselves. Instead they partner with hyperscalers (OpenAI with Azure, Anthropic with AWS, Google, Microsoft) and commit to massive multi-year cloud spend. Anthropic alone has pledged more than $100 billion to AWS over ten years. A few outliers like Meta’s in-house AI effort or xAI’s Memphis supercluster blur the lines, but at smaller scale or in partnership.

Spenders, the Hyperscalers. These are the ones writing the giant checks: Microsoft, Amazon (AWS), Alphabet, Meta, and increasingly Oracle. They are collectively guiding toward $600 to $720 billion in total capex for 2026, the vast majority of it AI related (data centers, GPUs, networking, power infrastructure). They build and buy physical stuff because they own the cloud platforms where most training and inference actually happens.

Capacity multipliers, the Neoclouds. A new tier that sits between the hyperscalers and the labs. The Big 4 are CoreWeave (preferred NVIDIA access), Nebius (European data sovereignty), Crusoe (vertically integrated energy), and Lambda (developer ecosystem). Combined neocloud capex in 2026 lands somewhere around $50 to $80 billion, with combined revenue approaching $25 to $30 billion and growing at triple-digit rates. What makes this tier interesting is that it does not really sit on anyone’s balance sheet. NVIDIA owns 7% of CoreWeave and committed to buying back more than $6 billion of cloud services from it. Microsoft has pledged more than $60 billion of capacity commitments to neoclouds. The neoclouds then borrow against those contracts via delayed-draw term loans and use the proceeds to buy more NVIDIA GPUs. Hyperscalers and labs effectively use the neoclouds as a leveraged vehicle to spend more capex than their own books would allow. Neoclouds are the most leveraged expression of the AI capex thesis, and the most cyclical tier of it.

Receivers, the supply chain. This is where the hyperscaler money actually lands.

Chip designers: NVIDIA dominant, with AMD and Broadcom for custom ASICs

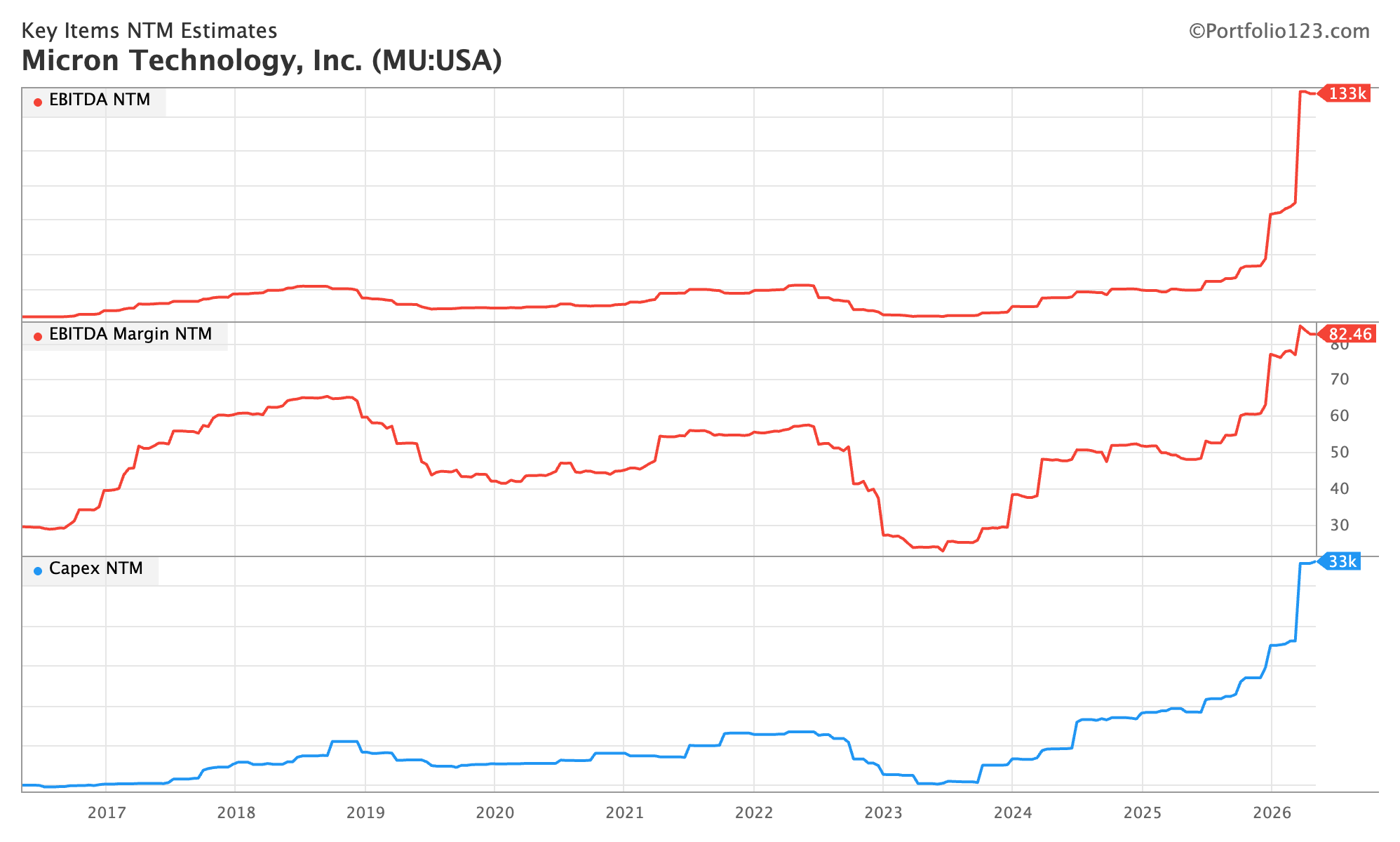

Memory makers: Micron, Samsung, SK Hynix, especially HBM for AI

Foundries: TSMC

Networking, servers, cooling, and power equipment

These are the direct monetizers of the capex wave. NVIDIA alone has visibility to more than $1 trillion of AI GPU revenue through 2027, almost entirely on the back of hyperscaler orders.

The flow is straightforward:

AI labs push model capability → hyperscalers race to build capacity to capture the revenue and keep cloud customers happy → money floods into the receiver supply chain → better hardware enables even bigger models → repeat.

This is the optimal chain of events, and right now the scaling laws are still working. The semis rally that kicked off the day Anthropic previewed its new frontier model Mythos in early April is the market repricing exactly this loop.

The Demand Side Is Genuinely Insane

Let me be clear: the demand side for compute is wildly bullish. Newer models require more power per training run, inference demand keeps climbing, and the per-token cost of inference keeps falling. This is the Jevons paradox in textbook form, and it is the bulls’ favorite (and best) argument. It is currently impossible to secure a B200 Blackwell GPU at any price the market considers reasonable.

The bottom line: demand for compute is rising exponentially while supply strains to keep up. That backdrop is structurally bullish for semiconductors and the broader AI complex.

The question is not whether the story is real (it is!), the actual question is how much of it is already in the price.

Markets Trade the Second Derivative

The receivers are extremely dependent on the hyperscaler capex line, and the absolute numbers are monstrous. Current consensus is roughly:

Numbers that big are easy to get drunk on. Until you look at the rate of change.

These are estimates and they will be revised. But the shape is unambiguous. The peak in capex growth is being reached by year end. From here, you are looking at decelerating growth even if the absolute capex line keeps drifting higher.

This matters enormously for the receivers. Their valuations are priced for an ever-accelerating earnings curve. Betting on a re-acceleration of AI capex from current levels is, at best, courageous. We are already running the largest capex cycle in modern history. Cracking $1 trillion is possible. Being closer to the end of the cycle than to the beginning is far more likely. Markets are forward looking; the deceleration gets priced before it shows up in earnings.

My View on AI Capex Receivers

Now to the part of the cycle that gets dismissed too easily.

Yes, the move in semis and memory has been a repricing of fundamentals more than a pure speculative move. The earnings story is historic. I do not dispute that. I also still believe in free markets and capitalism, and Jeff Bezos famously summed it up:

“Your margin is my opportunity.”

When companies enjoy fat profit margins (charging far more than their costs), competitors and new entrants treat that as an open invitation. They enter the market, slash prices, accept razor-thin or even negative margins to start, and use scale, efficiency, and reinvestment to capture share and eventually dominate the incumbent.

We saw it play out with Amazon in US retail. We saw it again with Chinese EVs. We will see it in semiconductors and memory. Yes, the barriers to entry are high. So is the incentive for developed countries to fund national champions and reduce their dependency on a small cartel of suppliers. Every government with industrial policy ambitions is staring at the same map.

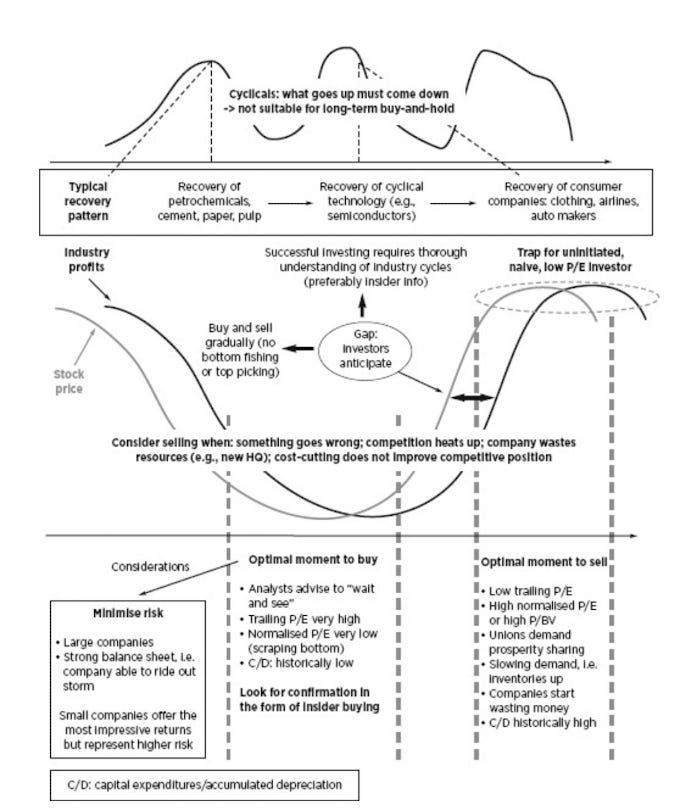

The pricing power the receivers enjoy today is a function of a temporary supply bottleneck inside an exceptional demand surge. This too shall pass.

Buying a cyclical after several years of record earnings and when the P/E ratio has hit a low point is a proven method for losing half your money in a short period of time.

Peter Lynch

The AI capex receivers are cyclical companies. Wonderful businesses, in many cases, with real moats. Cyclical nonetheless.

The rate of change of hyperscaler spending is going to decelerate, and the tailwind these cyclical names have been riding for two years is fading. The earnings growth they have delivered from current levels is not sustainable.

My base case for the cohort: a range-bound regime at best, a bear market at worst, once the second derivative flips and competition starts nibbling at margins.

This does not mean shorting them tomorrow. It means refusing to chase here, scaling out into strength, and concentrating exposure on the bottlenecks that are most defensible rather than on the speculative satellite names where forward earnings are already pricing perfection.

Hyperscalers: I Am Quietly Turning Bullish

My stance on hyperscalers used to be bearish. Free cash flows were falling, buybacks were being paused, and the ROIC on the capex was an open question with no good answer.

That stance is changing. I am neutral and on the verge of turning bullish.

You have all seen the chart that has been making the rounds on X: combined hyperscaler NTM FCF estimates basically pinned at zero. Given what I just laid out about the deceleration in capex growth, that FCF line should at minimum stop falling here. The open question is whether operating cash flow can outgrow what is now stabilizing capex, and whether the ROIC eventually shows up as overwhelmingly positive.

The risk-reward has shifted. We are starting to see real green shoots, especially in the latest Google and Amazon prints. Revenue and margin payback is showing genuine early validation. The hyperscalers are supply constrained, backlogs are exploding, cloud growth is re-accelerating, and cloud operating margins are expanding sharply thanks to in-house silicon and efficiency gains.

The hard data from this earnings season:

Google Cloud: +63% YoY, first ever quarter above $20B

AWS: +28% YoY, the fastest growth in 15 quarters

Microsoft Azure: +40% YoY, with the AI-specific annualized run rate hitting $37B (+123% YoY)

Meta’s ad business (now AI-powered end to end): +33% with strong pricing and volume

Combined RPO and signed backlogs across the cohort sit in the hundreds of billions, already inked, converting over the next 1 to 2 years

ROIC is still in the “prove it” phase for 2026 and 2027. FCF will stay under pressure for a few more quarters, and Meta (which lacks a real cloud monetization engine) faced the most scrutiny this season. However, the early data of accelerating cloud growth, expanding margins, and signed demand points toward green shoots rather than a bubble top.

A Caveat on the Earnings Boom

A small reality check before getting too euphoric. SP500 Q1 2026 EPS growth came in at +25% YoY. That number is silly. It is heavily inflated by Amazon and Google marking up their equity stakes in Anthropic and a handful of other private AI companies.

Adjust that out and you are at roughly +16% YoY, which is still strong. The median SP500 stock is growing EPS at +11%, also a healthy double-digit print.

So yes, on paper there is an earnings boom. A meaningful chunk of it is one-time price appreciation on private investments, plus accounting asymmetry where the AI capex receivers print earnings today while the hyperscalers amortize the cost of those purchases over many years. A lot of value creation has been pulled forward and recognized on accelerated timelines. That can become a drag later when comps and depreciation schedules collide.

Apple: One of These Stocks Is Not Like the Others

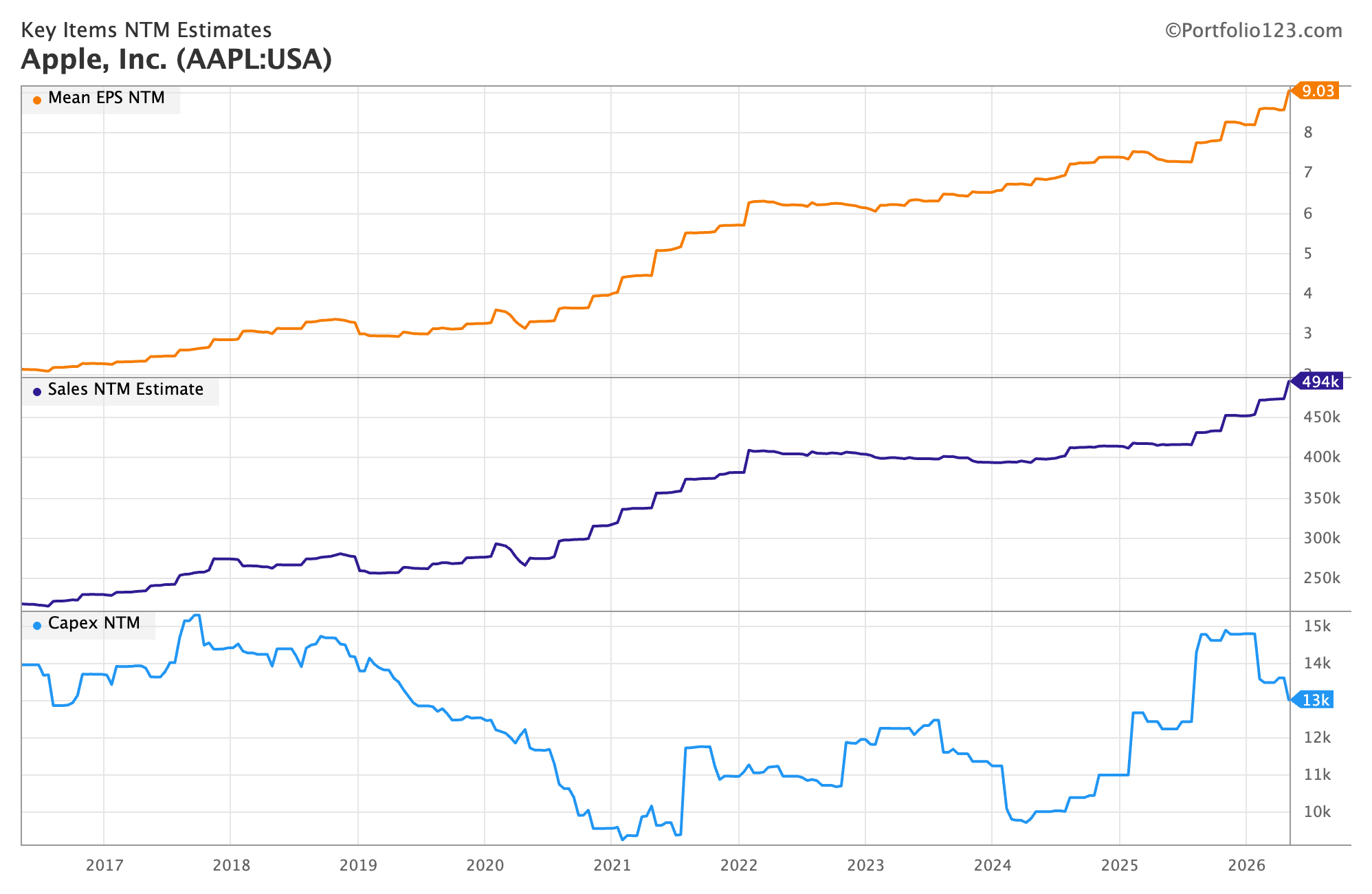

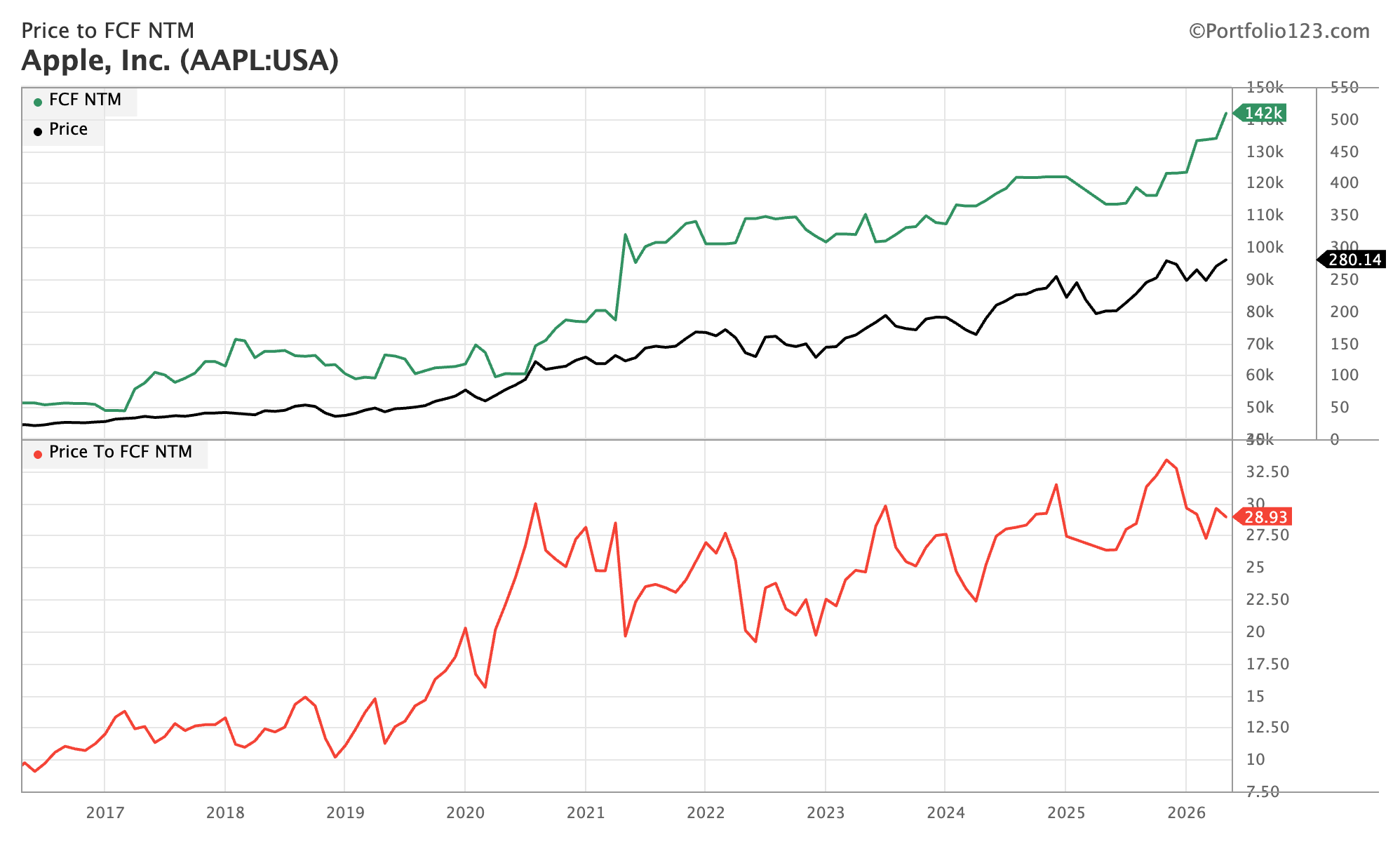

Apple has decided to sit out the AI capex cycle. They keep doing what they do best: growing free cash flow and buying back stock. I really like Apple here for a simple reason. It is fairly priced and I do not have to make up my mind on hyperscaler ROIC to own it.

Apple is indirectly exposed to AI through the receiving end. They benefit from every model improvement without funding it, and they are uniquely positioned at the device layer where on-device inference is about to take off. They also managed to defend their margins through the memory and GPU crunch, which is a testament to how well this company is run. Sales are reaccelerating, with analysts marking up their revenue estimates meaningfully over the next three years.

The Apple bull case in bullets:

Not burning cash on AI capex

Free to pick the winning model (currently Gemini) for a small partnership tag

2.5 billion devices already in users’ hands, ready for an AI Siri rollout

A war chest to spend on the application layer while everyone else was busy spending on models and infra

Best-in-class hardware for on-device inference

Produces the best chips for phones and laptops

Latest earnings: +17% revenue growth without raising hardware prices, accelerating, with record cash flow and EPS, and a strong +14% to +17% guide

Apple is still a growth company. Higher trending revenue, expanding margins, and the most recognizable brand on the planet. They are playing to their strengths: brand, hardware, and logistics.

The hardware story is genuinely impressive. The new M4 Max and Apple Mac Studio are tailor made for the “pick and shovel” side of the local AI wave, with software optimizations like Unified Memory, excellent CPU efficiency, MLX, and RDMA over Thunderbolt. These are decisions made years ahead of time finally paying off.

Most importantly, the sentiment around Apple has flipped. They used to be punished for “having no AI strategy.” Now they are increasingly recognized as the natural winner of the local inference rollout. It is a thematic bet that is orthogonal to data centers, which I find genuinely useful for portfolio construction.

Bottom line: Apple is the hardware king, and local inference is about to take off as smaller models become good enough for most everyday tasks.

Final Words

There will be winners and losers in this cycle, and today’s winners are not necessarily tomorrow’s. Right now everyone is raising capital, no one is short of cash, and we are about to see some of the largest IPOs in history. We are being told Anthropic is growing revenue at a pace never seen before. Fair enough. They also have a story to sell.

Do not be the bag holder when the capex cycle starts decelerating and the wave of stock issuance/unlocks arrives. Value will concentrate in a few specific places: where margins remain high, where competition cannot enter, and where bottlenecks persist long enough to keep pricing power intact.

Zooming out, the mega-secular force of passive investing forces all of us to have an opinion on the Mag 7, because that is where the money flows. The market lives or dies on the Mag 7. Despite earnings overstated for the moment, the bull case still has a real foundation: early signs of capex paying off, and a slower rate of change in capex itself, which is exactly what is needed to restore FCF growth and reactivate the buyback machine.

Until I can confidently assess the ROIC, I have parked part of my portfolio in Apple. It gives me beta to the market without paying the AI hype tax, and the local inference theme is a promising tailwind. The rest of the book stays with energy stocks, fertilizers, and agricultural futures. Owning some large tech is a useful diversifier along these boomer positions; it lowers realised portfolio volatility because oil currently trades with a negative correlation to US equities.

Finally, I remain acutely concerned that another wave of inflation is coming. Apple also happens to be the cleanest defensive in megacap land thanks to its FCF, war chest, and ability to trade like a defensive name once volatility picks up.