Positioning Update

A Taco a day keeps the bears away

Today’s post is free! Like and re-stack this post if you enjoyed it! It will help me a lot.

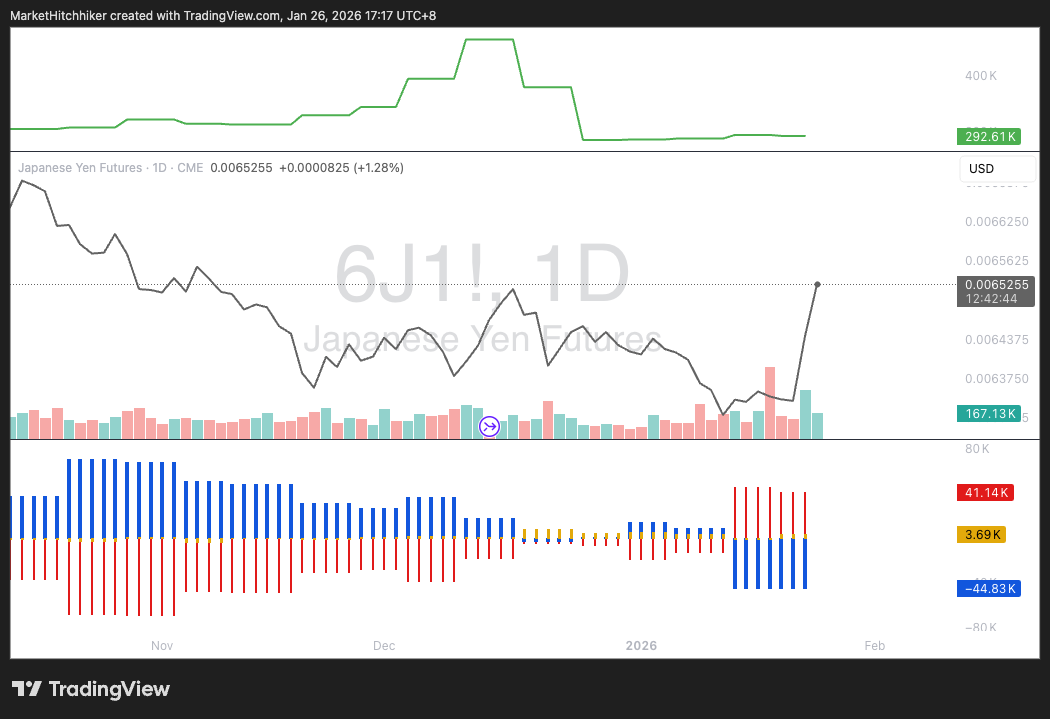

In last week’s update, I highlighted the short positioning in the yen and explained the rationale behind a long position (long 6J = short USD/JPY). A trade was triggered at 0.006366 on the 6J March contract. It is trading right now at 0.0065245, a +2.5% return in one week. My sizing tool was telling me to allocate 95% of my portfolio toward this trade. Not bad for a week’s worth of (hard) work. You can find last week’s issue below; the paywall has been removed for free subscribers.

Positioning Update

Another week, another positioning update! Here are the COT data that caught my attention:

Let’s review the most interesting charts for this week, starting, of course, with the yen.

Japanese Yen: The CoT data is as of last Tuesday’s close. This was before all the MOF/Fed shenanigans of last Friday, so keep that in mind, positioning has most likely shifted by now. As of last Tuesday, however, the short positioning remained unchanged for the large spec crowd. We will have to wait until Friday night for the new data.

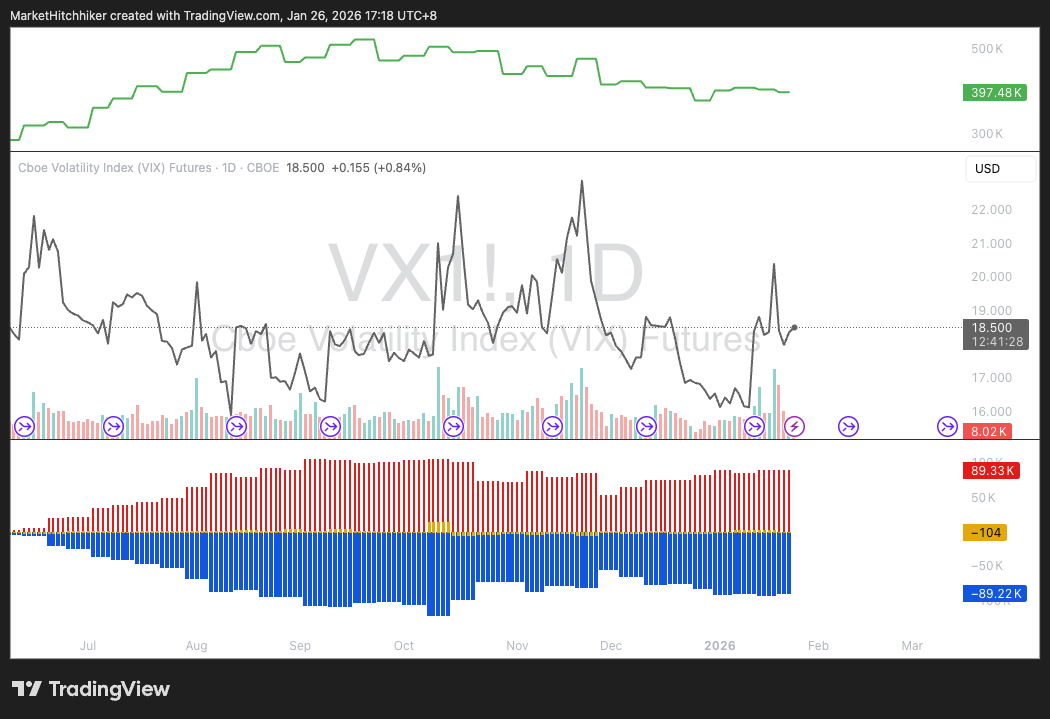

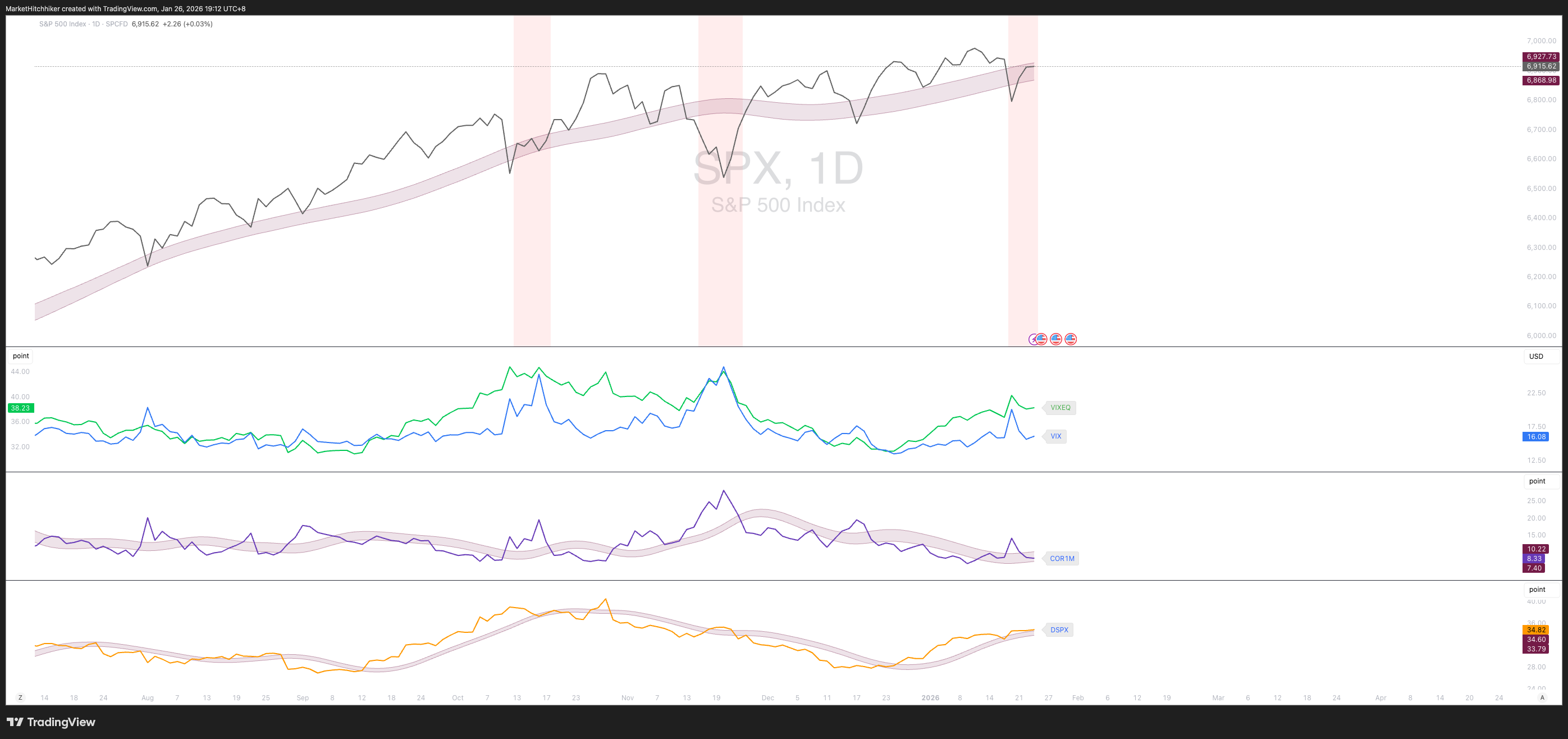

VIX: Large specs are still very short despite last Tuesday’s “risk-off” event. It’s interesting to see the VIX futures not resetting lower either. To me, it feels like we have some unfinished business here. TACO or no TACO, the positioning remains frothy.

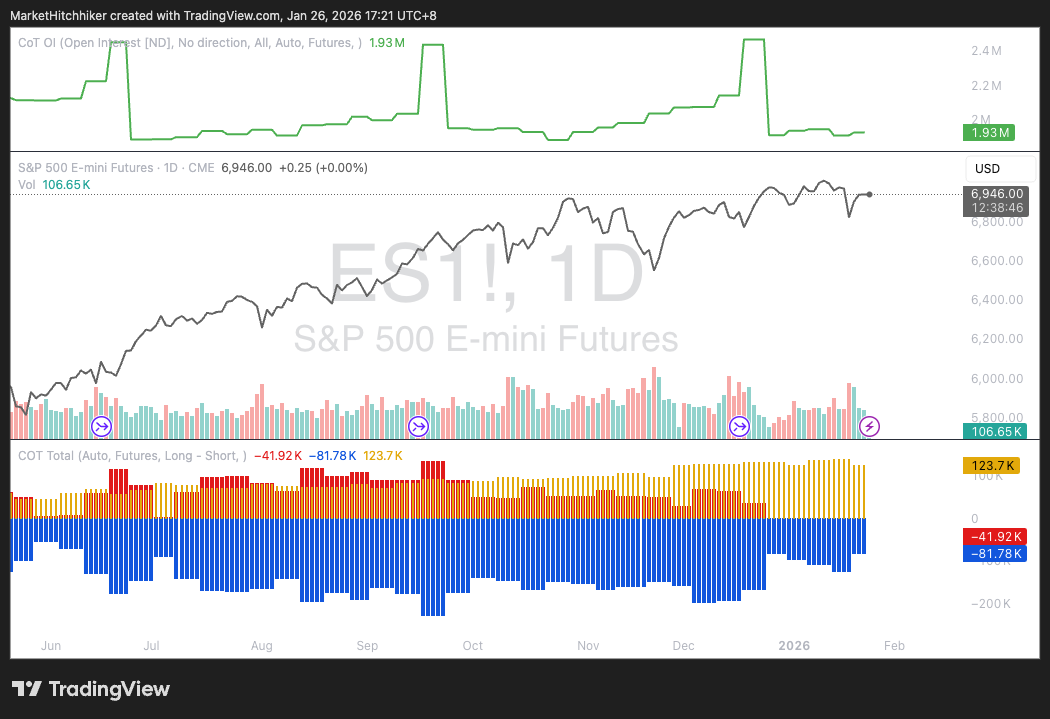

SP500: This is also the case in ES futures: we can see an uptick in positioning for large specs as of Tuesday’s close. With both the VIX and ES crowded long, I am very cautious with my risk-on positions.

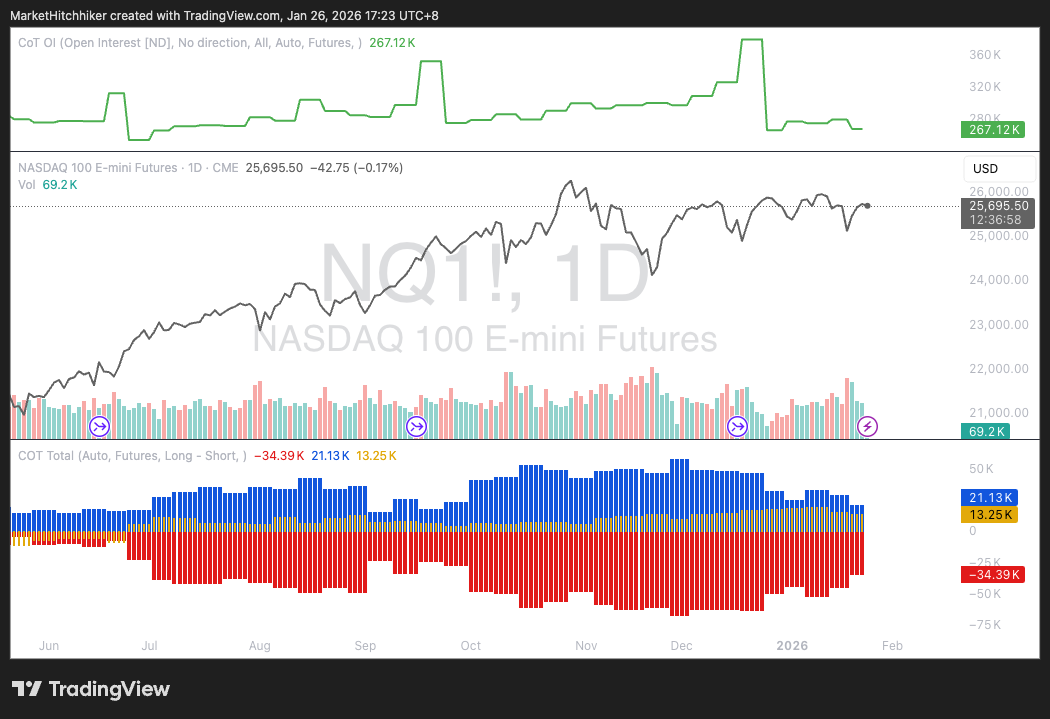

Nasdaq-100: At least NQ futures are showing light positioning, this is one point for the bulls here…

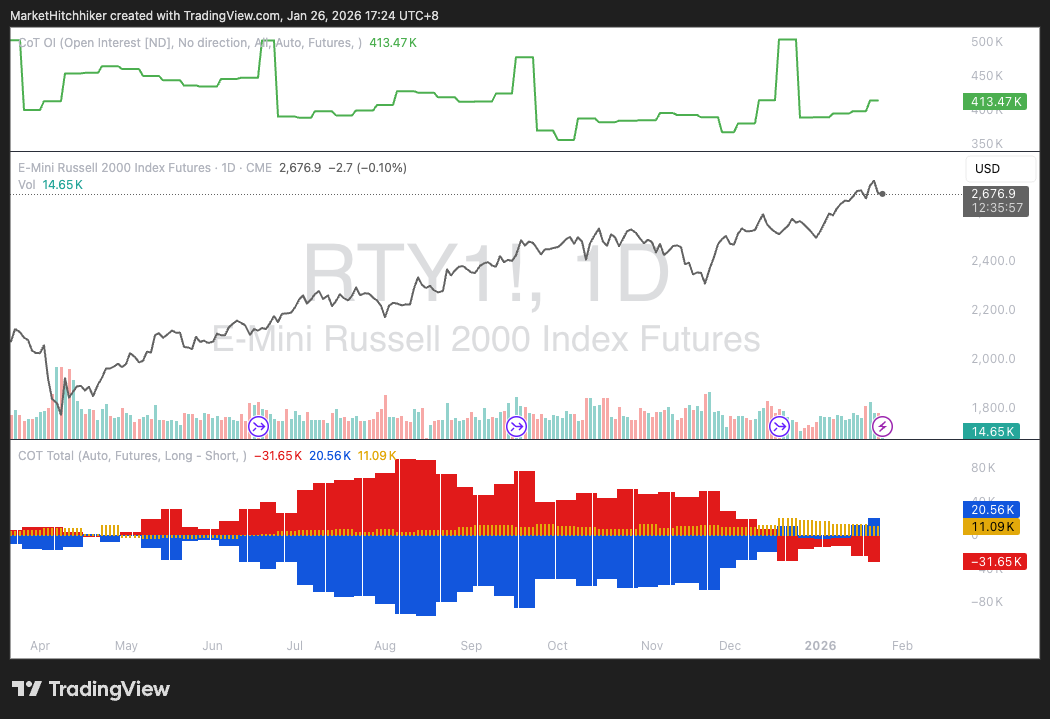

Russell 2000: …But small (unprofitable) caps are now crowded longs. The broadening-out narrative is still going strong. The big question is whether the market can march higher without Tech leadership. Historically, it cannot. So we better have strong earnings from the Mag-7; otherwise, we are cooked.

Let’s dive a bit deeper here and go beyond the CoT data.

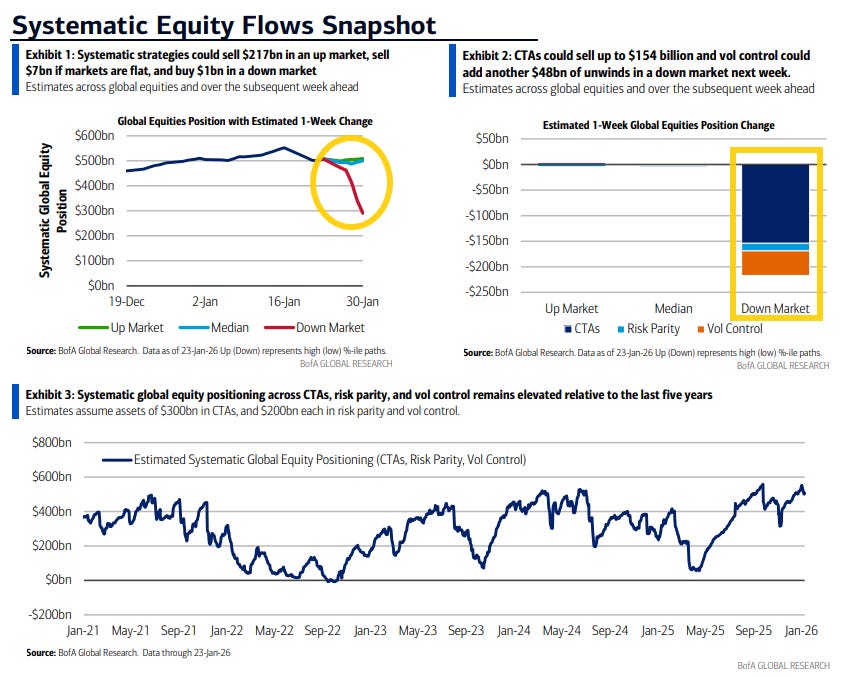

Systematic Investors:

Looking at BofA’s latest snapshot, the positioning is really not pretty here. Because realised volatility has been so low, CTAs are selling in both an up market and a down market:

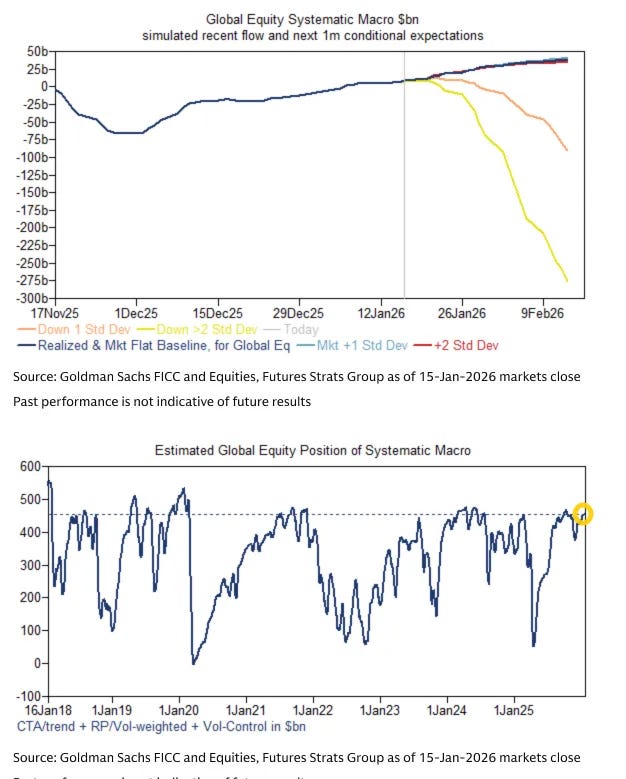

GS has a slightly different picture, but the conclusion is the same: Estimated global equity positioning of systematic macro is… very high.

Discretionary Investors:

Reminder: I wrote a guide about this crowd of degens. Read it if you haven’t yet:

The Hitchhiker's Guide to Positioning: Part I

Imagine spotting the early signs of a market cascade before it unfolds, volatility spikes triggering systematic sell-offs that amplify downturns across the board, from hedge funds to retail traders. In today’s $50 trillion US equities landscape, understanding positioning isn’t just insightful; it’s essential for anticipating those moves and staying ahead

The retail crowd did not disappoint last Tuesday, thanks to the TACO:

CNBC:

Tuesday was the third biggest single day for retail trader buying in a year, JPMorgan said. Flows of dollars into stocks from individual investors hit $12.9 billion this week — nearly double the weekly average over the past 12 months and close to the level of buying seen in the wake of Trump unveiling higher tariffs last April, the bank found.

Sustained buying momentum in the new year has pushed retail activity to new records on a rolling monthly basis, Jain added.

And this is not just Tuesday, retail traders pressed the buy button during the entire month of January for size!

Same analysis from Citadel:

And don’t get me started on Instit money…

And our beloved implied correlation is back to the lows:

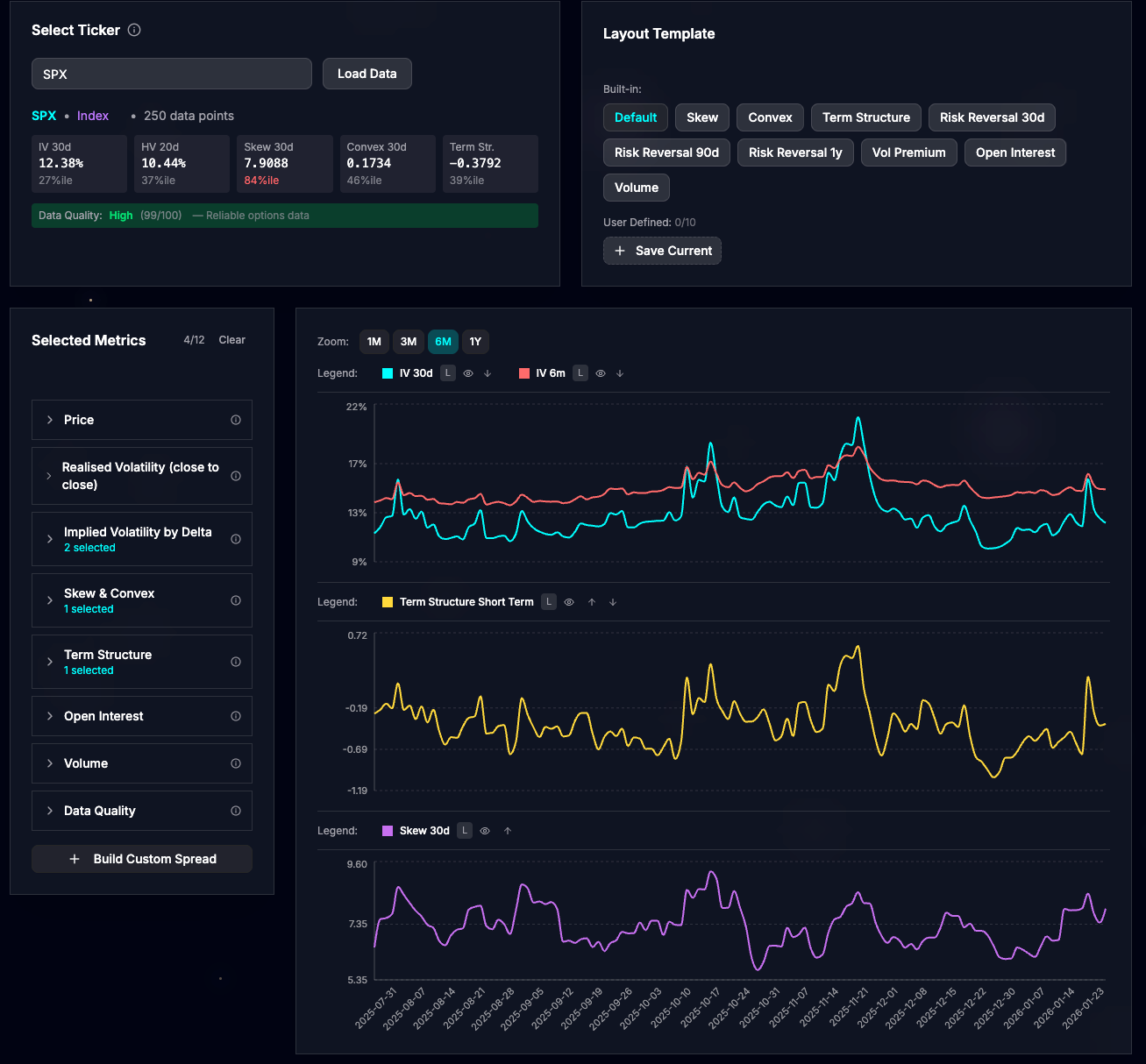

In terms of implied volatility, ATM implied vol reset a bit, but it doesn’t look like an all-clear signal yet: skew ticked up on Friday, and the term structure is not resetting lower. As I said earlier, we have some unfinished business on the downside for SPX.

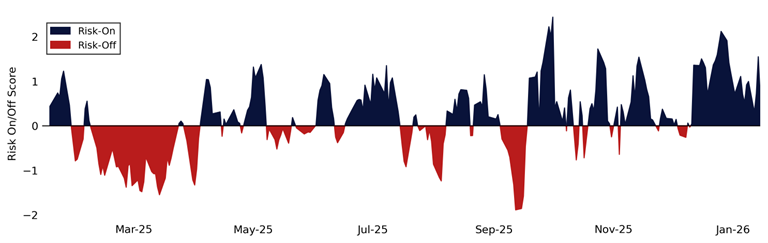

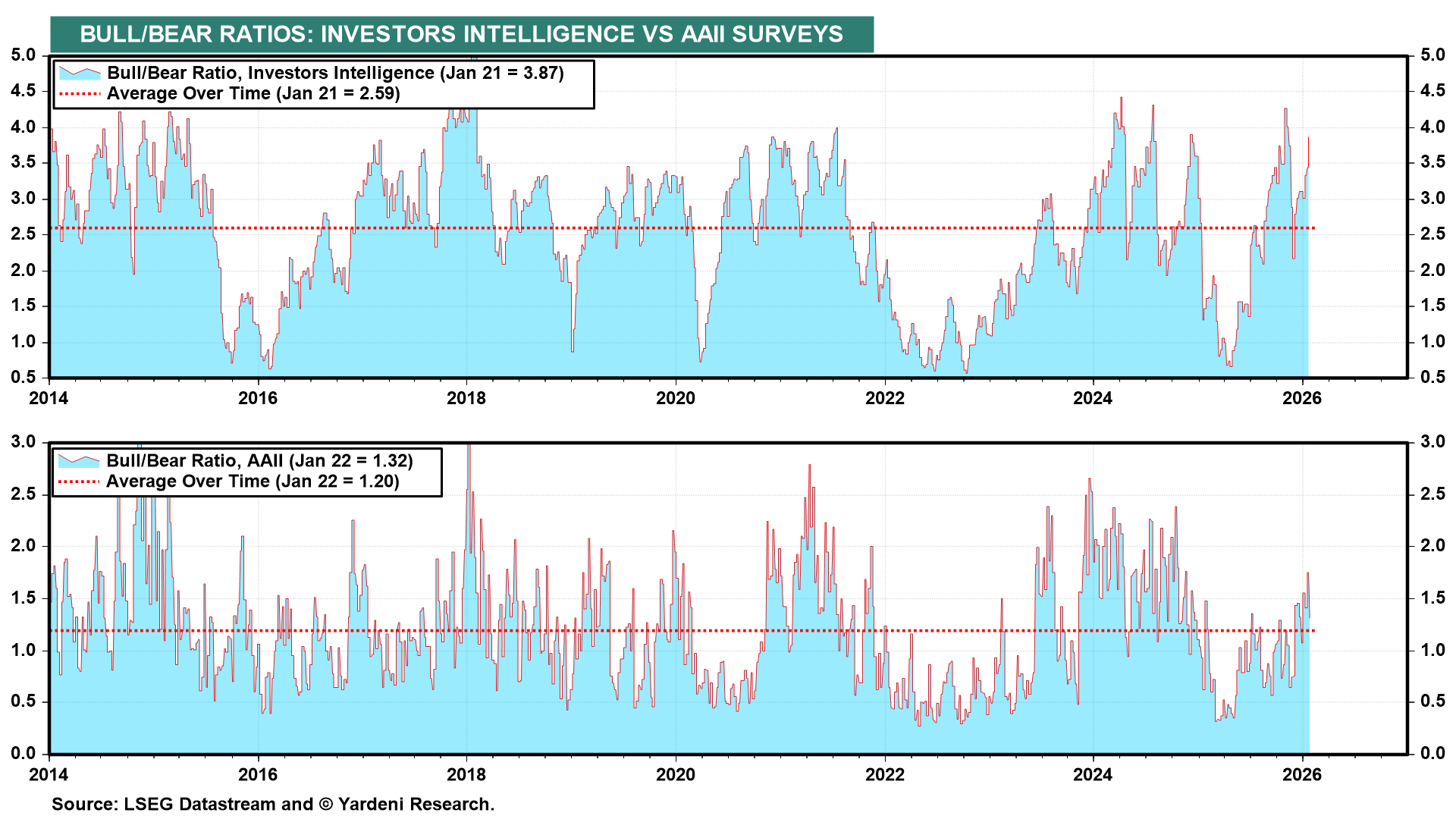

Regarding Sentiment, Yardeni always have the right wording:

Sentiment. So we have nothing to fear but nothing to fear (other than Greenland and other geopolitical risks). The Bull/Bear ratios suggest that too much good news is boosting bullishness, which may be bearish from a contrarian perspective (chart). Then again, we might have to raise our 20% subjective odds of a meltup/meltdown scenario. Stay tuned.

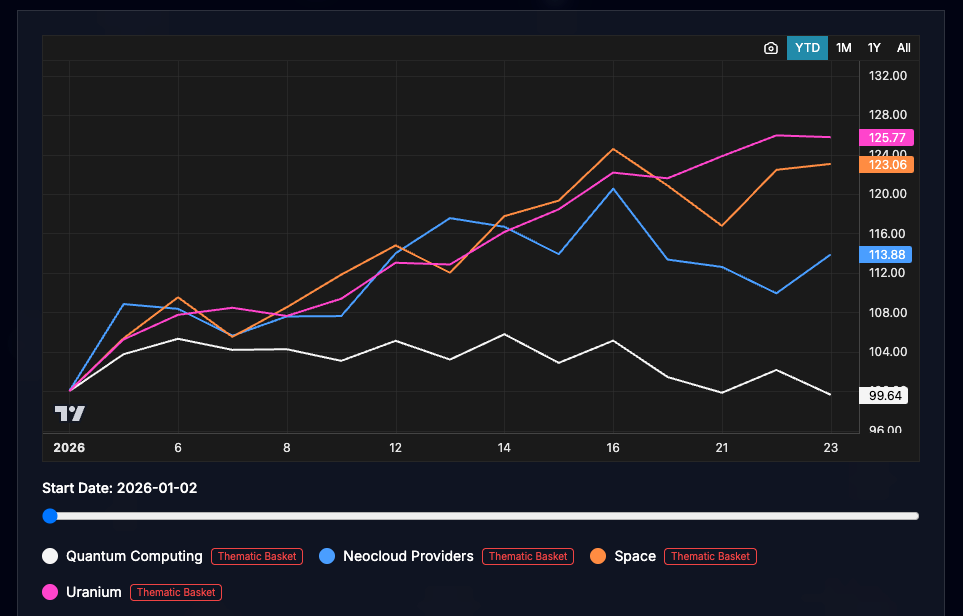

Given all this information, I am again quite bearish on US equities. After taking profit in the pre-market last Tuesday on the short NQ, I am very tempted to reopen a short position. But first things first: it is about time to close that awful trade on the quantum computing theme. I was hoping for a rebound in animal spirits, with momentum pushing these names higher in January. Alas… I picked the absolute worst thematic basket! The momentum factor decided to leave this theme but stick to uranium, space, neo-cloud providers, and other unprofitable tech baskets. This is comical, honestly…

Anyway, we are exiting the trade at a tiny loss and we move on. The process was good, I just got unlucky. Good process with bad outcome is something I can live with.

Momentum factor looks extended too, another bear argument…

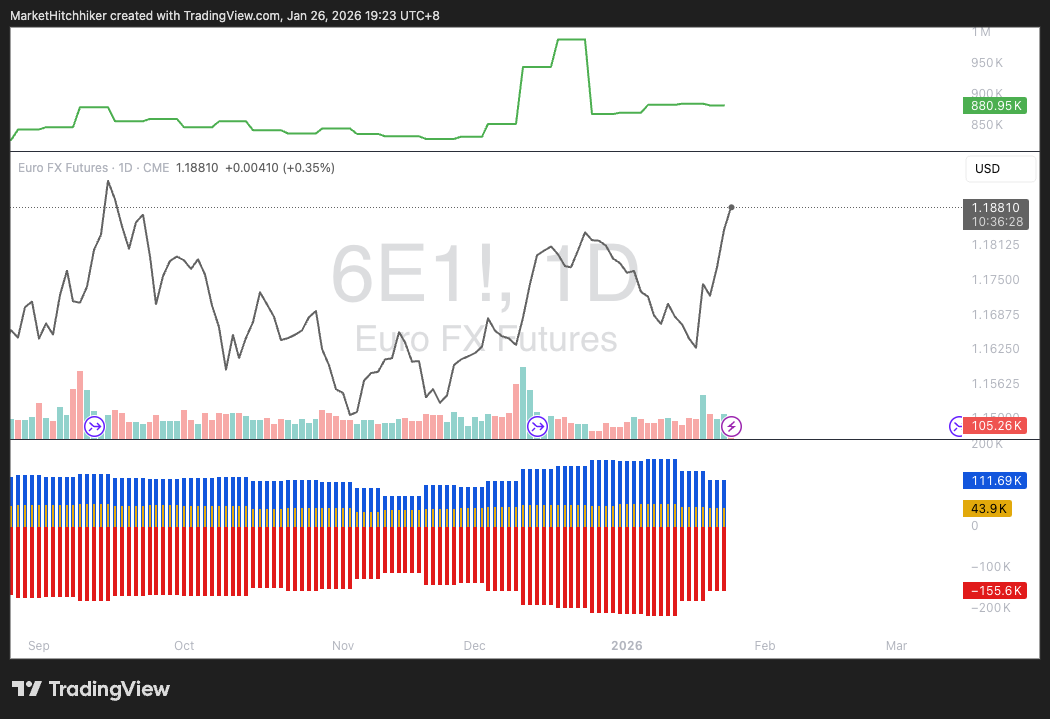

One last chart for this post, the CoT on Euro:

You gotta love this: large spec where degrossing at the bottom. Classic.

I write weekly on positioning, covering all asset classes, this is usually a paid post. Become a paid subscriber if you wish to access these posts weekly. You also get access to the web app, where you have access to a lot of great trading tools to better understand what moves the market.